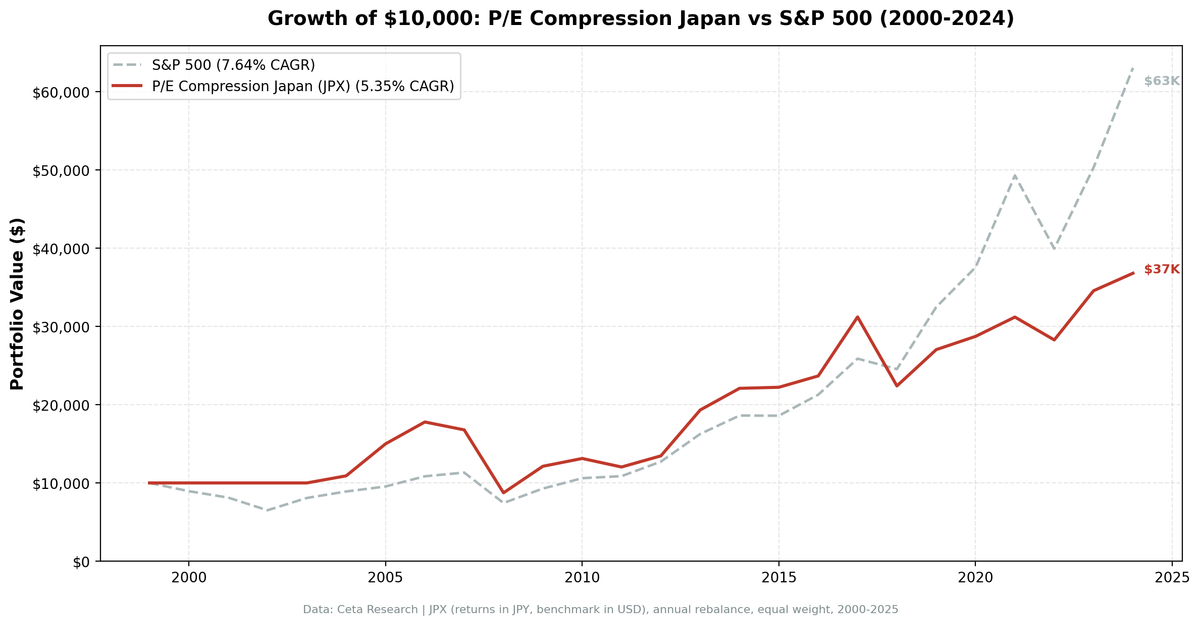

Japan P/E Compression: Underperforms by 2.29% Annually

We tested P/E compression mean reversion on 25 years of Japanese stock data. The strategy returned 5.35% annually (JPY-denominated) vs 7.64% for SPY, underperforming by 2.29% per year. This is an honest look at why P/E compression doesn't work in Japan: structural deflation, corporate governance issues, and low earnings growth make compressed P/E ratios often justified, not temporary.

Contents

- Method

- What We Found

- 25 years. -2.29% annual underperformance. Mean reversion doesn't work.

- Why P/E Compression Fails in Japan

- Backtest Methodology

- Conclusion

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: JPX, market cap > ¥100B

- Period: 2000-2025 (25 years, 25 annual periods)

- Rebalancing: Annual (January), equal weight, top 30 by compression ratio

- Benchmark: S&P 500 Total Return (SPY, USD)

Returns are in JPY. Benchmark (SPY) is in USD.

What We Found

25 years. -2.29% annual underperformance. Mean reversion doesn't work.

| Metric | P/E Compression (Japan) | S&P 500 (USD) |

|---|---|---|

| CAGR | 5.35% | 7.64% |

| Excess CAGR | -2.29% | - |

| Sharpe Ratio | 0.261 | 0.322 |

| Max Drawdown | -50.89% | -34.90% |

| Down Capture | 86.55% | 100% |

| Avg Stocks per Year | 28.0 | - |

| Cash Periods | 4 of 25 (16%) | - |

The strategy underperformed SPY despite having 28 stocks on average and only 16% cash periods. This isn't a data problem or an implementation issue. The signal simply doesn't work in Japan.

The -50.89% max drawdown is worse than SPY's -34.90%, and the down-capture of 87% shows the strategy didn't provide meaningful downside protection.

Why P/E Compression Fails in Japan

Structural deflation. Japan experienced decades of deflation and low inflation. When the economy doesn't grow, earnings don't grow, and P/E ratios don't expand. Compressed P/E ratios are often justified, not temporary.

Corporate governance. Japanese companies historically hoard cash, underinvest, and resist shareholder value initiatives. A compressed P/E ratio may reflect poor capital allocation, not temporary undervaluation.

Zombie companies. Many Japanese firms trade at low multiples because they're structurally unprofitable or low-growth. These aren't mean reversion opportunities; they're value traps.

Currency headwinds. JPY weakened vs USD over this period, adding complexity to the comparison. But even in local-currency terms, the strategy underperformed.

Low earnings growth. Without earnings growth, P/E mean reversion requires multiple expansion. In a deflationary, low-growth environment, multiples stay compressed.

Backtest Methodology

| Parameter | Choice |

|---|---|

| Universe | JPX, Market Cap > ¥100B |

| Signal | Current P/E < 85% of 5-year avg, P/E 5-40, ROE > 10%, D/E < 2.0 |

| Portfolio | Top 30 by lowest compression ratio, equal weight |

| Rebalancing | Annual (January) |

| Benchmark | S&P 500 Total Return (SPY, USD) |

| Period | 2000-2025 (25 years) |

| Returns | JPY-denominated (portfolio), USD (benchmark) |

Conclusion

P/E compression doesn't work in Japan, underperforming SPY by 2.29% annually. Structural deflation, low earnings growth, and corporate governance issues make compressed P/E ratios often justified, not temporary. Mean reversion strategies require environments where fundamentals support multiple expansion. Japan doesn't provide that.

Part of a Series: Japan | Global | US | UK | UK | Thailand | Thailand | Switzerland

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP). Returns in JPY. See full methodology at github.com/ceta-research/backtests.