P/E Compression in Hong Kong: When Compressed Multiples Keep

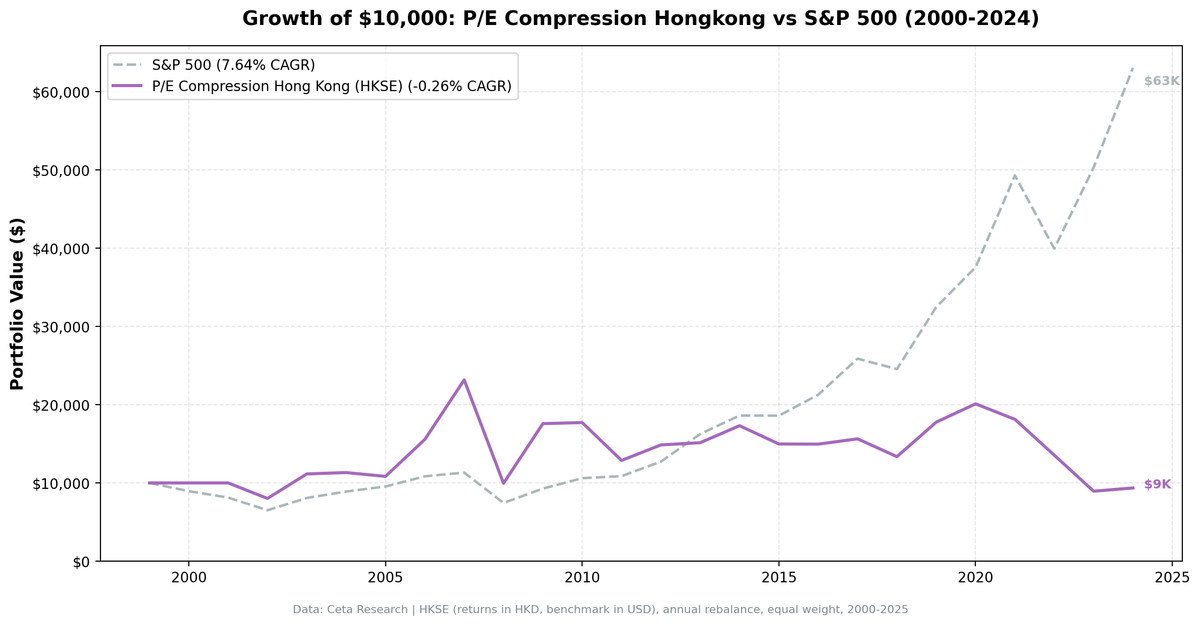

We ran the P/E compression screen on HKSE (Hong Kong Stock Exchange) from 2000 to 2025. The strategy averaged 20 qualifying stocks per year, held cash in only 2 of 25 years, and still returned -0.26% annually vs 7.64% for the S&P 500. A $10,000 investment became roughly $9,360. The down capture of 132.62% tells the story: when global markets fell, Hong Kong's P/E compression stocks didn't just fall with them. They fell harder.

Contents

- Method

- The Strategy

- Screen

- Results

- When It Worked (Briefly)

- Why It Fails

- Full Annual Returns

- Limitations

- Run It Yourself

- Part of a Series

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: HKSE (Hong Kong Stock Exchange), market cap > exchange-specific threshold

- Period: 2000-2025 (25 annual rebalance periods)

- Rebalancing: Annual (January), equal weight top 30 by compression score

- Benchmark: S&P 500 Total Return (SPY)

- Currency note: Returns in HKD. Benchmark is USD. The HKD/USD peg has been stable (7.75-7.85 range), so currency effects here are minimal compared to free-floating markets.

- Cash rule: Hold cash if fewer than 10 stocks qualify

Historical financial data with 45-day lag to prevent look-ahead bias. Full methodology: backtests/METHODOLOGY.md

The Strategy

P/E compression is the inverse of multiple expansion. A stock whose P/E has contracted 15%+ below its own historical average looks cheap relative to itself, not cheap in absolute terms, but cheap relative to what the market was willing to pay for this company's earnings across multiple business cycles.

The filters:

| Criterion | Metric | Threshold | Why |

|---|---|---|---|

| Valuation compression | Current P/E / 5yr avg P/E | < 0.85 | 15%+ below own history |

| Real earnings | P/E | > 5 | Positive earnings, not distressed |

| Not speculative | P/E | < 40 | Excludes story stocks |

| Profitability | Return on equity | > 10% | Business still earns decent returns |

| Leverage | Debt-to-equity | < 2.0 | Not over-leveraged |

| Liquidity | Market cap | > exchange threshold | Investable |

| History | Prior P/E data | 3+ years | Enough to compute meaningful average |

Ranking: Top 30 by most compressed (lowest current/average ratio), equal weight.

The ROE and D/E filters are the key differentiator from simple low-P/E screens. A stock with a compressed P/E but deteriorating fundamentals is a value trap. The quality filters select for companies where the compression looks like sentiment or cycle-driven repricing, not earnings deterioration. In Hong Kong's case, this distinction matters. But it didn't help.

Screen

WITH fy_pe AS (

SELECT r.symbol, r.priceToEarningsRatio AS pe, r.dateEpoch,

ROW_NUMBER() OVER (PARTITION BY r.symbol ORDER BY r.dateEpoch DESC) AS rn,

AVG(r.priceToEarningsRatio) OVER (

PARTITION BY r.symbol ORDER BY r.dateEpoch

ROWS BETWEEN 5 PRECEDING AND 1 PRECEDING

) AS avg_pe_5yr,

COUNT(r.priceToEarningsRatio) OVER (

PARTITION BY r.symbol ORDER BY r.dateEpoch

ROWS BETWEEN 5 PRECEDING AND 1 PRECEDING

) AS n_prior

FROM financial_ratios r

JOIN profile p ON r.symbol = p.symbol

WHERE r.period = 'FY' AND r.priceToEarningsRatio > 0 AND r.priceToEarningsRatio < 100

AND p.exchange IN ('HKSE')

)

SELECT f.symbol, p.companyName, p.sector,

ROUND(f.pe, 2) AS current_fy_pe,

ROUND(f.avg_pe_5yr, 2) AS pe_5yr_avg,

ROUND(f.pe / f.avg_pe_5yr, 3) AS pe_ratio_to_avg,

ROUND((1 - f.pe / f.avg_pe_5yr) * 100, 1) AS compression_pct,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(f2.debtToEquityRatioTTM, 2) AS debt_to_equity,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM fy_pe f

JOIN key_metrics_ttm k ON f.symbol = k.symbol

JOIN financial_ratios_ttm f2 ON f.symbol = f2.symbol

JOIN profile p ON f.symbol = p.symbol

WHERE f.rn = 1

AND f.avg_pe_5yr IS NOT NULL

AND f.n_prior >= 3

AND f.pe > 5

AND f.pe < 40

AND f.pe / f.avg_pe_5yr < 0.85

AND k.returnOnEquityTTM > 0.10

AND (f2.debtToEquityRatioTTM IS NULL OR (f2.debtToEquityRatioTTM >= 0 AND f2.debtToEquityRatioTTM < 2.0))

ORDER BY f.pe / f.avg_pe_5yr ASC

LIMIT 30

Results

| Metric | Portfolio | S&P 500 |

|---|---|---|

| CAGR | -0.26% | 7.64% |

| Total Return | -6.4% | 530.7% |

| Max Drawdown | -61.39% | -34.90% |

| Volatility (ann.) | 28.73% | 17.51% |

| Sharpe Ratio | -0.114 | 0.322 |

| Sortino Ratio | -0.182 | — |

| Beta | 0.879 | 1.00 |

| Alpha | -7.35% | — |

| Up Capture | 67.87% | — |

| Down Capture | 132.62% | — |

| Win Rate (vs SPY) | 32.0% | — |

| Cash Periods | 2/25 | — |

| Avg Stocks | 20.3 | — |

The headline: negative CAGR over 25 years. The strategy didn't just underperform. It lost money. A $10,000 investment in January 2000 was worth about $9,360 by end of 2025. While SPY turned the same $10,000 into $63,070.

The down capture of 132.62% is the worst figure across all 19 exchanges in this series. When global markets fell, Hong Kong's compressed-multiple stocks amplified those losses. The mean reversion mechanism that drives the US signal ran backwards here: compressed multiples got more compressed in downturns, not less.

When It Worked (Briefly)

The strategy had a strong early run, concentrated in the 2006-2009 window.

| Year | Portfolio | S&P 500 | Excess |

|---|---|---|---|

| 2003 | +39.1% | +24.1% | +15.0% |

| 2006 | +43.7% | +13.7% | +30.0% |

| 2007 | +48.9% | +4.4% | +44.5% |

| 2009 | +76.7% | +24.7% | +51.9% |

| 2019 | +33.0% | +32.3% | +0.7% |

These years coincided with Hong Kong's role as the dominant gateway for foreign capital entering China. The 2006-2007 period was fueled by the pre-crisis commodities and China growth boom. Hong Kong-listed companies with depressed multiples caught a re-rating as capital flooded into the region. 2009 was post-crisis recovery, consistent with global compressed-multiple rebounds.

These weren't structural wins. They were cyclical. The strategy spent most of the remaining 21 years giving them back.

Why It Fails

The 132.62% down capture is the number to understand. It means that when the S&P 500 fell 10% in a given year, this portfolio fell roughly 13.3% on average. Over 25 years with multiple significant down periods, that asymmetry compounds into disaster.

The structural discount problem. Hong Kong equities have traded at a persistent discount to global peers for over a decade. This isn't temporary sentiment, it's priced-in risk: legal system uncertainty after the 2020 National Security Law, capital control concerns, the Hang Seng Index's heavy concentration in financials and property, and direct exposure to mainland China policy decisions. When a HKSE stock shows P/E compression vs its own 5-year history, that history may include pre-NSL valuations. The market isn't wrong to reprice those. The fundamental risk profile of many listed companies changed.

Geopolitical risk as a permanent repricing factor. The 2021-2024 stretch was particularly painful: the strategy returned -9.8%, -25.3%, -34.0%, and +4.6% against SPY's +31.3%, -19.0%, +26.0%, and +25.3%. That's three consecutive years of severe negative excess return. The 2023 result (-34.0% while SPY gained 26.0%) represents a -60.0% excess gap in a single year. This wasn't a statistical anomaly. It reflects the ongoing structural repricing of Hong Kong as a financial center.

Down cycles amplify. HK-listed companies have significant leverage to Chinese economic cycles, global trade volumes, and regional property markets. In global risk-off environments, capital exits the region disproportionately. Compressed multiples become more compressed, not less. The quality filters (ROE, D/E) can't screen out this systemic exposure.

The 2008 blow-up. -57.0% against SPY's -34.3%, a -22.7% excess loss. This was the test of whether quality filters protect against deep drawdowns. They didn't. The max drawdown of -61.39% is the second worst in this global series.

The P/E compression signal assumes there's a "normal" multiple a business should revert to. In Hong Kong post-2020, that assumption breaks down. The structural discount is the new normal, not a temporary anomaly.

Full Annual Returns

| Year | Portfolio | S&P 500 | Excess |

|---|---|---|---|

| 2000 | 0.0% | -10.5% | +10.5% (cash) |

| 2001 | 0.0% | -9.2% | +9.2% (cash) |

| 2002 | -19.8% | -19.9% | +0.1% |

| 2003 | +39.1% | +24.1% | +15.0% |

| 2004 | +1.6% | +10.2% | -8.7% |

| 2005 | -4.3% | +7.2% | -11.5% |

| 2006 | +43.7% | +13.7% | +30.0% |

| 2007 | +48.9% | +4.4% | +44.5% |

| 2008 | -57.0% | -34.3% | -22.7% |

| 2009 | +76.7% | +24.7% | +51.9% |

| 2010 | +0.8% | +14.3% | -13.5% |

| 2011 | -27.3% | +2.5% | -29.8% |

| 2012 | +15.4% | +17.1% | -1.7% |

| 2013 | +1.9% | +27.8% | -25.9% |

| 2014 | +14.3% | +14.5% | -0.1% |

| 2015 | -13.5% | -0.1% | -13.4% |

| 2016 | -0.1% | +14.4% | -14.6% |

| 2017 | +4.5% | +21.6% | -17.1% |

| 2018 | -14.6% | -5.2% | -9.4% |

| 2019 | +33.0% | +32.3% | +0.7% |

| 2020 | +13.2% | +15.6% | -2.5% |

| 2021 | -9.8% | +31.3% | -41.1% |

| 2022 | -25.3% | -19.0% | -6.3% |

| 2023 | -34.0% | +26.0% | -60.0% |

| 2024 | +4.6% | +25.3% | -20.7% |

Win rate: 8 of 25 years with positive excess return.

Limitations

Currency effects. Returns are in HKD. The HKD/USD peg has held throughout the test period (range: 7.75-7.85), so FX translation isn't a major driver. This is one of few non-US markets where the currency comparison is relatively clean.

Pre-2020 vs post-2020 regime change. The strategy's failure isn't uniformly distributed across time. The 2000-2019 period shows a -3.34% average annual excess. The 2020-2024 period shows -14.1% average annual excess. The structural shift after the National Security Law represents a genuine regime change that historical P/E averages can't reflect.

Compressed multiples vs value traps. The quality filters (ROE > 10%, D/E < 2) are designed to separate temporary sentiment repricing from fundamental impairment. In HK post-2020, this distinction blurs. A company can have stable ROE and low debt but still face regulatory or geopolitical risks that permanently impair its multiple. The screen can't price that risk.

Annual rebalancing lag. January rebalancing using prior FY data means the portfolio can't respond to mid-year events (protests, regulatory announcements, geopolitical developments). This lag is particularly costly in a market as news-sensitive as HK.

Part of a Series: Japan | Global | US | UK | UK | Thailand | Thailand | Switzerland

Run It Yourself

git clone https://github.com/ceta-research/backtests.git

cd backtests

# Hong Kong backtest

python3 pe-compression/backtest.py --preset hongkong --output results.json --verbose

# Current screen

python3 pe-compression/screen.py --preset hongkong

Part of a Series

This is the Hong Kong analysis. We tested the same screen across 19 exchanges globally:

- Global comparison →. The East-West divide across 19 markets

- US analysis →, 9.97% CAGR, +2.32% excess, where it works best

- UK analysis →, 9.02% CAGR, +1.38% excess

- Canada analysis →, 8.75% CAGR, 23.7% down capture

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Returns in HKD. Benchmark: SPY (USD). Full methodology: METHODOLOGY.md. Past performance doesn't guarantee future results.