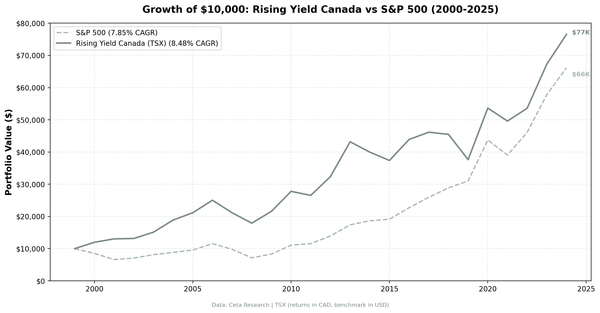

dividend investing

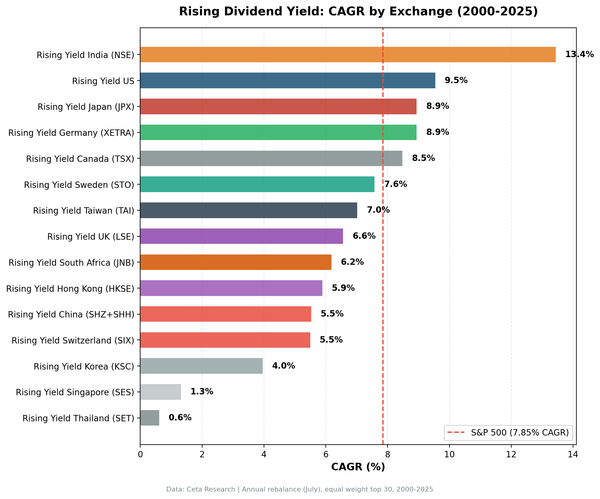

Rising Dividend Yield on Canadian Stocks: 8.48% CAGR With Zero Cash Periods

We applied the rising dividend yield screen to 25 years of TSX data. 8.48% CAGR, +4.53% annual alpha vs TSX Composite, zero cash periods, and lower volatility than the US version. Canada''s resource and financial sectors are natural dividend growers.