Sector Momentum Rotation: Chasing Industry Trends in US Markets

Sector Momentum Rotation: Chasing Industry Trends Across 26 Years of US Markets

Sector momentum is one of the few quantitative signals that has survived decades of academic scrutiny and real-world testing. The idea: industries that outperformed recently tend to keep outperforming. Buy the winners. Let the losers sit.

Contents

- The Strategy

- Results

- Which Sectors Drive the Rotation

- When It Works

- When It Struggles

- Full Annual Returns

- Run It Yourself

- Limitations

- References

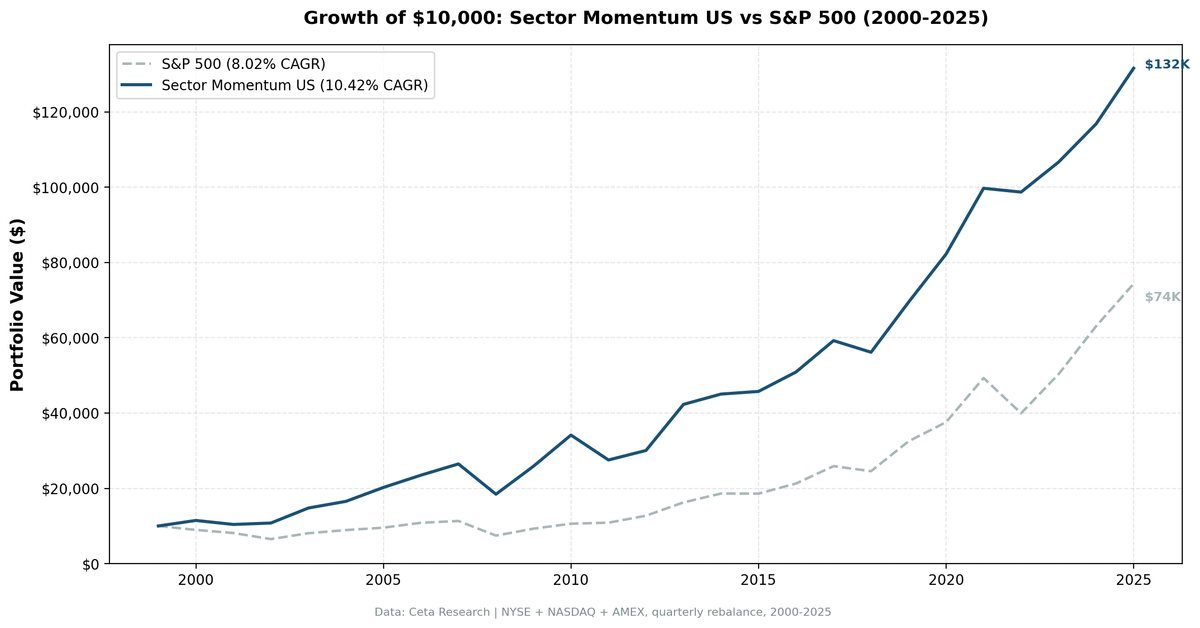

We ran this strategy on US markets (NYSE, NASDAQ, AMEX) from 2000 to 2025. The result: 10.42% CAGR versus 8.02% for SPY, with meaningfully lower drawdown in most losing years. Over 26 years, $10,000 grew to $131,577 in the portfolio versus $74,347 in SPY.

The real story isn't the average outperformance. It's when the strategy wins and when it doesn't.

The Strategy

Each quarter, we rank all 11 GICS sectors by their equal-weighted 12-month trailing return. We buy stocks from the top 2 sectors. Holdings are equal-weighted within the portfolio, rebalanced quarterly. Stocks must meet an exchange-specific market cap threshold to be included.

The academic foundation comes from Moskowitz and Grinblatt's 1999 paper, "Do Industries Explain Momentum?" Their answer was yes. Industry-level momentum is persistent and partially explains the broader momentum anomaly documented by Jegadeesh and Titman (1993). When an industry catches a tailwind, commodity supercycles, regulatory shifts, demographic demand, that tailwind tends to last more than one quarter.

| Parameter | Value |

|---|---|

| Universe | NYSE, NASDAQ, AMEX |

| Period | 2000-2025 (26 years) |

| Rebalance | Quarterly |

| Signal | Equal-weighted 12M sector trailing return |

| Sectors held | Top 2 each quarter |

| Stock weighting | Equal weight within portfolio |

| Market cap min | Exchange-specific threshold |

| Transaction costs | Size-tiered: 0.1% (>$10B), 0.3% ($2–10B), 0.5% (<$2B), one-way |

| Cash quarters | 3 of 104 (3%) |

| Avg stocks held | 315.8 |

Results

| Metric | Portfolio | SPY |

|---|---|---|

| CAGR | 10.42% | 8.02% |

| Final value ($10k) | $131,577 | $74,347 |

| Max drawdown | -42.02% | -45.53% |

| Sharpe ratio | 0.405 | — |

| Sortino ratio | 0.613 | — |

| Calmar ratio | 0.248 | — |

| Up capture | 106.61% | — |

| Down capture | 81.21% | — |

| Beta | 0.983 | — |

| Alpha | 2.5% | — |

| Win rate vs SPY | 50.0% | — |

Down capture of 81.21% is the key number here. When SPY fell, this portfolio fell less on average. Not dramatically, but consistently. Over 26 years, that consistency compounds.

The win rate of 50.0% tells you this isn't a strategy that beats SPY every year. Half the annual periods went to the portfolio, half to SPY. The edge comes from the magnitude of wins versus losses, not frequency.

Which Sectors Drive the Rotation

Some sectors dominated the top-2 rotation over the full 26-year period.

| Sector | Quarters in Top 2 |

|---|---|

| Healthcare | 31 |

| Energy | 30 |

| Basic Materials | 30 |

| Technology | 25 |

| Utilities | 19 |

| Consumer Cyclical | 18 |

| Consumer Defensive | 16 |

| Real Estate | 14 |

| Communication Services | 13 |

| Industrials | 12 |

Healthcare, Energy, and Basic Materials each appeared in 29-30% of all quarters. These aren't random. Healthcare benefits from persistent demographic demand and multi-year drug approval cycles. Energy and Basic Materials track commodity supercycles that play out over 5-10 years. When oil runs, it tends to run for a while.

Technology appeared in 25 quarters but delivered most of its rotation signal in the post-GFC era and again in 2020-2021. The 2019-2024 period saw tech dominate index returns through market-cap concentration rather than sector-level momentum, which created drag for this strategy.

When It Works

Early in commodity cycles. The 2000-2002 period is the clearest example. While the dot-com bust crushed SPY (-10.5%, -9.2%, -19.9%), the portfolio returned +14.7%, -9.3%, +3.7%. Energy and Basic Materials carried the rotation as commodity demand from emerging markets began building.

Post-crisis recoveries. 2009 through 2010 showed the strategy at its best: +40.3% and +32.0% versus +24.7% and +14.3% for SPY. Momentum carried beaten-down sectors that had lagged through the GFC back into leadership.

Rate hike environments. 2022 is the standout year. SPY fell 19.0%. The portfolio fell just 1.0%. Energy was rotating into the top-2 signal as oil prices climbed, and the sector delivered while everything else sold off. That single year contributed roughly 18 percentage points of relative outperformance.

Early 2000s overall. The strategy returned +25.2%, +23.6% excess in 2000 and 2002 respectively. These years defined the long-term relative return. Without them, the CAGR gap narrows considerably.

When It Struggles

The AI era (2019-2024). Six consecutive years of underperformance or near-parity with SPY. The market rewarded a handful of large-cap technology companies through passive index flows rather than broad sector rotation. Healthcare and Energy kept appearing in the top-2 signal, but their returns didn't keep up with the index being pushed higher by mega-cap tech.

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2019 | +23.68% | +32.31% | -8.6% |

| 2020 | +18.39% | +15.64% | +2.8% |

| 2021 | +21.27% | +31.26% | -10.0% |

| 2022 | -1.01% | -18.99% | +18.0% |

| 2023 | +8.07% | +26.0% | -17.9% |

| 2024 | +9.50% | +25.28% | -15.8% |

The 2022 recovery partially offset the six-year drag, but the net result was a significant undershoot during the AI-era bull market.

2011. The portfolio returned -19.4% while SPY gained +2.5%. A -21.8% gap in a single year. European debt crisis contagion hit Energy and Materials hard. When global macro events create sharp, correlation-driven selloffs, sector momentum signals can carry you directly into the fire.

2012 and 2016. Both years saw the portfolio trail by 7-8%. Post-crisis mean reversion years where SPY caught up quickly while the momentum basket was still positioned in the prior cycle's leaders.

Full Annual Returns

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2000 | +14.68% | -10.5% | +25.2% |

| 2001 | -9.29% | -9.17% | -0.1% |

| 2002 | +3.65% | -19.92% | +23.6% |

| 2003 | +37.0% | +24.12% | +12.9% |

| 2004 | — | +10.24% | — |

| 2005 | +22.36% | +7.17% | +15.2% |

| 2006 | +16.13% | +13.65% | +2.5% |

| 2007 | +12.73% | +4.4% | +8.3% |

| 2008 | -30.39% | -34.31% | +3.9% |

| 2009 | +40.33% | +24.73% | +15.6% |

| 2010 | +31.98% | +14.31% | +17.7% |

| 2011 | -19.37% | +2.46% | -21.8% |

| 2012 | +9.18% | +17.09% | -7.9% |

| 2013 | +40.73% | +27.77% | +13.0% |

| 2014 | +6.48% | +14.5% | -8.0% |

| 2015 | +1.56% | -0.12% | +1.7% |

| 2016 | +11.28% | +14.45% | -3.2% |

| 2017 | +16.38% | +21.64% | -5.3% |

| 2018 | -5.21% | -5.15% | -0.1% |

| 2019 | +23.68% | +32.31% | -8.6% |

| 2020 | +18.39% | +15.64% | +2.8% |

| 2021 | +21.27% | +31.26% | -10.0% |

| 2022 | -1.01% | -18.99% | +18.0% |

| 2023 | +8.07% | +26.0% | -17.9% |

| 2024 | +9.5% | +25.28% | -15.8% |

| 2025 | +12.66% | +17.88% | -5.2% |

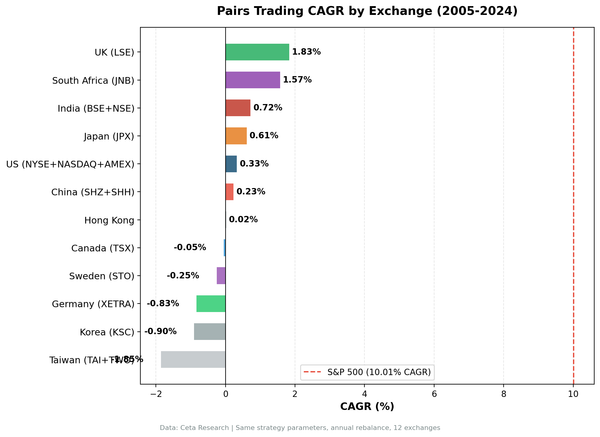

Part of a Series: Global | Korea | Japan | India | Germany | Canada

Run It Yourself

This query ranks current US sectors by 12-month equal-weighted trailing return. The top 2 are where the momentum signal points today.

WITH prices AS (

SELECT e.symbol, e.adjClose, CAST(e.date AS DATE) AS trade_date

FROM stock_eod e

JOIN profile p ON e.symbol = p.symbol

WHERE p.sector IS NOT NULL AND p.sector != ''

AND p.marketCap > 1000000000

AND p.exchange IN ('NYSE', 'NASDAQ', 'AMEX')

AND CAST(e.date AS DATE) >= CURRENT_DATE - INTERVAL '400' DAY

AND e.adjClose IS NOT NULL AND e.adjClose > 0

),

recent AS (

SELECT symbol, adjClose AS recent_price

FROM prices

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY trade_date DESC) = 1

),

year_ago AS (

SELECT symbol, adjClose AS old_price

FROM prices

WHERE trade_date <= CURRENT_DATE - INTERVAL '252' DAY

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY trade_date DESC) = 1

),

stock_returns AS (

SELECT r.symbol, pr.sector,

(r.recent_price / ya.old_price - 1) * 100 AS return_12m

FROM recent r

JOIN year_ago ya ON r.symbol = ya.symbol

JOIN profile pr ON r.symbol = pr.symbol

WHERE ya.old_price > 0 AND r.recent_price > 0

AND (r.recent_price / ya.old_price - 1) BETWEEN -0.99 AND 5.0

)

SELECT

sector,

ROUND(AVG(return_12m), 2) AS avg_return_12m_pct,

COUNT(DISTINCT symbol) AS n_stocks,

ROW_NUMBER() OVER (ORDER BY AVG(return_12m) DESC) AS rank

FROM stock_returns

GROUP BY sector

HAVING COUNT(DISTINCT symbol) >= 5

ORDER BY avg_return_12m_pct DESC

Run this query on Ceta Research: cetaresearch.com/data-explorer?q=-oJZC4EYnB

For the stock screen (top stocks in momentum sectors): cetaresearch.com/data-explorer?q=TprJe-lIS9

Limitations

Concentration risk. Equal weighting across 300+ stocks provides diversification, but holding only the top 2 sectors means concentrated sector exposure. In 2011, that concentration cost 21.8% relative to SPY in a single year.

Momentum crashes. Academic literature documents momentum crashes during sharp reversals (especially post-crisis). When sectors that led into a downturn become the laggards out of it, the signal points in the wrong direction at the worst time. The 2008-2009 transition is a partial example.

AI-era underperformance. The 2019-2024 drag reflects a genuine structural challenge: passive index flows into mega-cap tech drove returns independent of sector rotation dynamics. If this pattern persists, the strategy's edge versus SPY may be smaller going forward.

Win rate. 50.0% annual win rate means you'll regularly experience multi-year underperformance streaks. The 2019-2024 run required conviction to stay with. Most investors won't.

Market cap filter. The $1B USD minimum excludes small and mid-cap stocks. The strategy captures sector trends at large-cap scale, not the full sector universe.

Transaction costs. The model uses size-tiered costs (0.1% for large-cap >$10B, 0.3% for mid-cap, 0.5% for small-cap), one-way. Actual costs depend on execution quality and position sizes.

References

- Moskowitz, T. J., & Grinblatt, M. (1999). Do industries explain momentum? The Journal of Finance, 54(4), 1249-1290.

- Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65-91.

Data: Ceta Research (FMP financial data warehouse), NYSE/NASDAQ/AMEX, 2000-2025 Backtest: 26 years, 104 quarters, 0.1% transaction costs, equal weight Past performance doesn't guarantee future results. This is educational content, not investment advice.