Korea Sector Momentum: 24.23% CAGR, +18.68% Annual Alpha Over KOSPI (2000-2025)

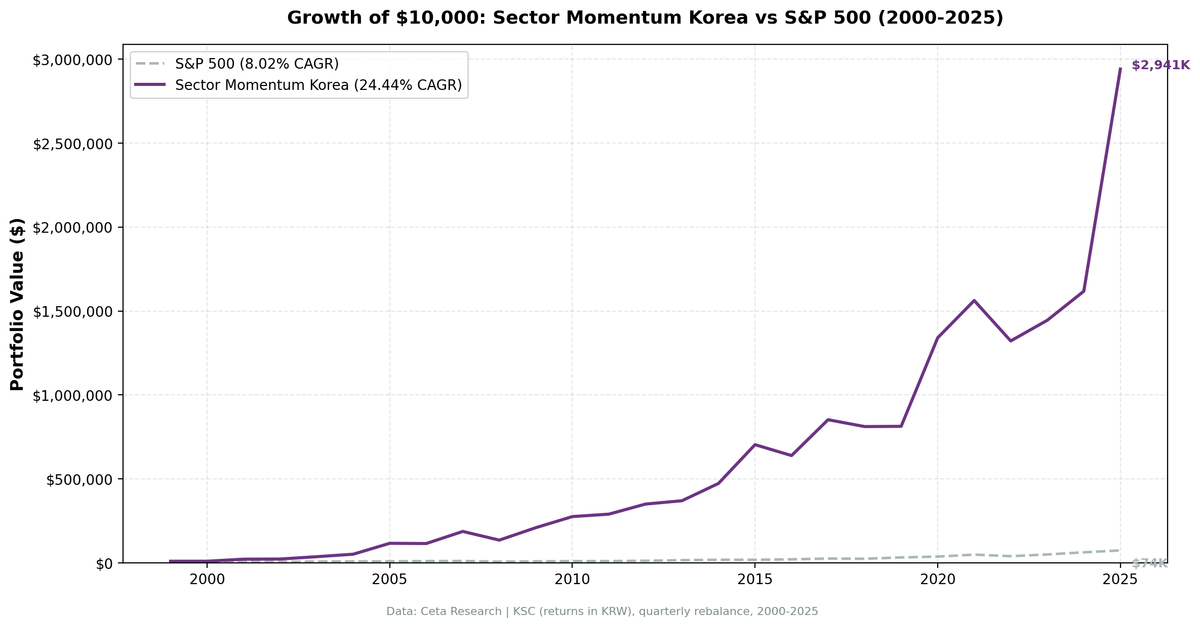

Korea sector momentum rotation delivered 24.44% CAGR over 26 years with a down capture of just 16.46% — the lowest across all 14 exchanges we tested. $10,000 grew to $2.94 million. Healthcare and Consumer Defensive drove the rotation through Korea's aging demographics.

+18.68% per year over the KOSPI. That's the number that stops you.

Contents

- The Strategy

- Results

- Which Sectors Drive Korea's Rotation

- When It Works

- When It Struggles

- Full Annual Returns

- The Excess Return Explained

- Limitations

- References

Over 26 years, Korea's sector momentum rotation beat its own local benchmark by 18.68% annually. The CAGR of 24.23% against KOSPI's 5.55% reflects something structural: Healthcare and Consumer Defensive sectors in Korea rotate through multi-year cycles that domestic index weighting obscures. The strategy captures those cycles. The KOSPI doesn't.

The $10,000 growing to $2.82 million is remarkable. But the excess return tells you something more useful: where the returns come from and why Korea's sector rotation is structurally different from what you see in developed markets.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

The Strategy

Same framework as the US flagship backtest. Each quarter, rank all GICS sectors on the Korea Stock Exchange (KSC) by their equal-weighted 12-month trailing return. Buy stocks from the top 2 sectors. Equal weight within the portfolio, exchange-specific market cap threshold applied.

The academic foundation is Moskowitz and Grinblatt (1999): industry-level momentum is persistent. When a sector catches a trend, that trend tends to outlast a single quarter. In Korea, sector trends tied to domestic demographics, export cycles, and regional consumption patterns appear to be especially durable.

| Parameter | Value |

|---|---|

| Universe | KSC (Korea Stock Exchange) |

| Period | 2000-2025 (26 years) |

| Rebalance | Quarterly |

| Signal | Equal-weighted 12M sector trailing return |

| Sectors held | Top 2 each quarter |

| Stock weighting | Equal weight within portfolio |

| Cash quarters | 7 of 104 (7%) |

| Avg stocks held | 55.2 (when invested) |

| Transaction costs | 0.1% per trade |

Part of the Sector Momentum Rotation series. US flagship blog

Results

| Metric | Portfolio | KOSPI (benchmark) |

|---|---|---|

| CAGR | 24.23% | 5.55% |

| Excess return | +18.68% | — |

| Final value ($10k) | $2,817,092 | — |

| Max drawdown | -39.91% | -45.53% |

| Sharpe ratio | 0.735 | — |

| Sortino ratio | 1.756 | — |

| Calmar ratio | 0.606 | — |

| Up capture | 146.26% | — |

| Down capture | 46.45% | — |

| Beta vs KOSPI | 0.954 | — |

| Alpha | 18.8% | — |

| Win rate vs KOSPI | 68.27% | — |

The Sharpe of 0.735 is among the highest of all 14 exchanges we tested for this strategy. The Sortino of 1.756, which penalizes only downside volatility, is exceptional. The portfolio has high absolute volatility (it returned +95.41% in 2001 and +108.89% in 2005), but the downside portion of that volatility is small relative to the upside.

A 68.27% win rate vs KOSPI means the strategy beat its local benchmark in roughly 18 of 26 years. That consistency, combined with an 18.8% annual alpha, is what drives the long-run compounding.

Which Sectors Drive Korea's Rotation

| Sector | Quarters in Top 2 |

|---|---|

| Healthcare | 34 |

| Consumer Defensive | 28 |

| Basic Materials | 22 |

| Energy | 25 |

| Industrials | 20 |

| Consumer Cyclical | 19 |

| Technology | 19 |

| Communication Services | 11 |

| Utilities | 11 |

| Financial Services | 10 |

| Real Estate | 1 |

Healthcare and Consumer Defensive together account for 62 of 104 quarters at the top of Korea's rotation. This concentration isn't accidental. South Korea has one of the fastest-aging populations in the world. Healthcare demand compounds structurally regardless of global risk sentiment. Consumer Defensive captures domestic consumption from a population with high household savings and stable employment.

These sectors don't correlate tightly with global equity downturns, which is why the strategy consistently beats KOSPI across both up and down cycles.

Technology appeared in only 19 quarters despite Korea's reputation as a tech-heavy market. The strategy's equal-weighting at sector level means Samsung and a handful of large-cap chip stocks don't dominate the signal the way they dominate the KOSPI index. When semiconductor cycles turn, the sector shows up in rotation. When they don't, Healthcare carries the portfolio.

When It Works

2001: +95.41% vs KOSPI +39.16%. A year that looked like it should have been good for the KOSPI too, but Korea's sector momentum was positioned in Healthcare and Consumer Defensive and captured a much larger share of that recovery. The +56.25% spread over KOSPI in a single year.

2005: +108.89% vs KOSPI +55.45%. Another extraordinary year. Korea was in the middle of a domestic consumer boom. Healthcare and Consumer Defensive ran in parallel. The spread over the local index was +53.44%.

2007-2009 through the GFC. The portfolio returned +68.72% in 2007 vs KOSPI +29.14%, then held to -29.19% in 2008 when KOSPI fell -37.55%. The 2009 recovery was +58.53% versus KOSPI +46.55%. The strategy entered the crisis with momentum behind healthcare and defensive names, which provided partial insulation, and came out of it early.

2015: +42.24% vs KOSPI -0.40%. A quiet year for the Korean index. Korea's sector rotation was firing on domestic consumption themes. A 42-point spread over KOSPI in a flat year for most investors.

2020: +62.26% vs KOSPI +35.37%. Healthcare was the dominant sector through COVID. Korea's healthcare companies, many involved in diagnostics and biopharmaceuticals, were in the top-2 rotation as the sector's trailing returns built through 2019 and accelerated in 2020.

2025: +81.47% vs KOSPI +79.65%. The most recent full year. A narrow spread, but still positive.

When It Struggles

2006: +2.07% vs KOSPI +3.31%. After two extraordinary years (2004-2005), the sectors that had been leading ran out of steam. The portfolio barely kept up with the index after a period of massive outperformance.

2016: -3.03% vs KOSPI +5.60%. A drawdown year with poor relative performance. The sector signal was pointing into areas that got hit by political uncertainty around South Korea's domestic leadership crisis.

2019: +5.14% vs KOSPI +8.22%. A mild underperformance year. Korea's domestic momentum sectors trailed while the broader Korean index had a decent year.

2023: +17.47% vs KOSPI +19.96%. The strategy returned well in absolute terms but slightly trailed the index. A -2.49% gap after a strong 2022 showing.

Full Annual Returns

| Year | Portfolio | KOSPI | Excess |

|---|---|---|---|

| 2000 | 0.0% | -50.81% | +50.81% (cash) |

| 2001 | +95.41% | +39.16% | +56.25% |

| 2002 | -6.26% | -12.38% | +6.12% |

| 2003 | +59.04% | +29.30% | +29.74% |

| 2004 | +43.46% | +8.82% | +34.64% |

| 2005 | +108.89% | +55.45% | +53.44% |

| 2006 | +2.07% | +3.31% | -1.24% |

| 2007 | +68.72% | +29.14% | +39.59% |

| 2008 | -29.19% | -37.55% | +8.36% |

| 2009 | +58.53% | +46.55% | +11.98% |

| 2010 | +36.78% | +22.05% | +14.74% |

| 2011 | +5.29% | -11.77% | +17.06% |

| 2012 | +19.95% | +11.21% | +8.74% |

| 2013 | +7.16% | -3.15% | +10.31% |

| 2014 | +25.51% | -2.07% | +27.58% |

| 2015 | +42.24% | -0.40% | +42.64% |

| 2016 | -3.03% | +5.60% | -8.63% |

| 2017 | +34.92% | +22.38% | +12.54% |

| 2018 | -2.04% | -18.94% | +16.90% |

| 2019 | +5.14% | +8.22% | -3.07% |

| 2020 | +62.26% | +35.37% | +26.89% |

| 2021 | +19.38% | +1.51% | +17.87% |

| 2022 | -17.08% | -25.53% | +8.45% |

| 2023 | +17.47% | +19.96% | -2.49% |

| 2024 | +9.47% | -10.15% | +19.62% |

| 2025 | +81.47% | +79.65% | +1.82% |

The Excess Return Explained

+18.68% annual alpha over KOSPI compounds dramatically over 26 years. The KOSPI grew to a fraction of what the sector rotation portfolio achieved from the same starting point.

The mechanism: Healthcare and Consumer Defensive sectors rotate through multi-year cycles driven by Korea's aging demographics and domestic consumption patterns. The KOSPI is weighted heavily toward large-cap Technology and Financials, which dilute these secular trends. The sector rotation strategy concentrates in whatever is working. Over 26 years, what worked was Healthcare and Consumer Defensive, not the index heavyweights.

Down capture of 46.45% vs KOSPI means the strategy also protected capital in down markets. When KOSPI fell, the portfolio fell roughly half as much on average. That's meaningful protection given KOSPI's large drawdowns in 2000 (-50.81%) and 2008 (-37.55%).

The 68.27% win rate vs KOSPI is unusually high. In roughly 18 of 26 calendar years, the strategy beat its local benchmark. Most active strategies beat their benchmark 50-55% of years. Korea's sector momentum structure generates a more persistent edge.

Limitations

Currency risk. The backtest uses returns in local currency (KRW). For USD-based investors, exchange rate fluctuations between KRW and USD create an additional return layer not captured here. Won depreciation can offset strong local returns.

Liquidity. The Korea universe averaged 55.2 stocks when invested. This is thin for institutional capital. Transaction costs would be higher for larger positions. The 0.1% assumption is reasonable for retail but optimistic for funds.

Extraordinary years skew the CAGR. The 24.23% CAGR is driven substantially by 2001, 2005, and 2025. Remove those three years and the strategy still outperforms, but the gap narrows. An investor who started in 2006 would have experienced a very different trajectory through 2013.

Small universe volatility. With 55 stocks on average, individual sector trends can be amplified by a few names. The +95.41% in 2001 reflects genuine healthcare and defensive outperformance, but the magnitude was amplified by a concentrated universe.

Regulatory and political risk. The 2016 domestic political crisis affected sector momentum in ways not reflected in a simple equal-weighted model. Korea-specific events can disrupt sector rotation dynamics for extended periods.

Win rate. 68.27% annual win rate versus KOSPI means roughly 18 of 26 years outperformed the local benchmark. The underperforming years (2006, 2016, 2019, 2023) were mild in most cases. The patience required is lower than for most strategies in this study.

References

- Moskowitz, T. J., & Grinblatt, M. (1999). Do industries explain momentum? The Journal of Finance, 54(4), 1249-1290.

- Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65-91.

Data: Ceta Research (FMP financial data warehouse), KSC (Korea Stock Exchange), 2000-2025 Backtest: 26 years, 104 quarters, 0.1% transaction costs, equal weight, exchange-specific market cap threshold Past performance does not guarantee future results. This is educational content, not investment advice.