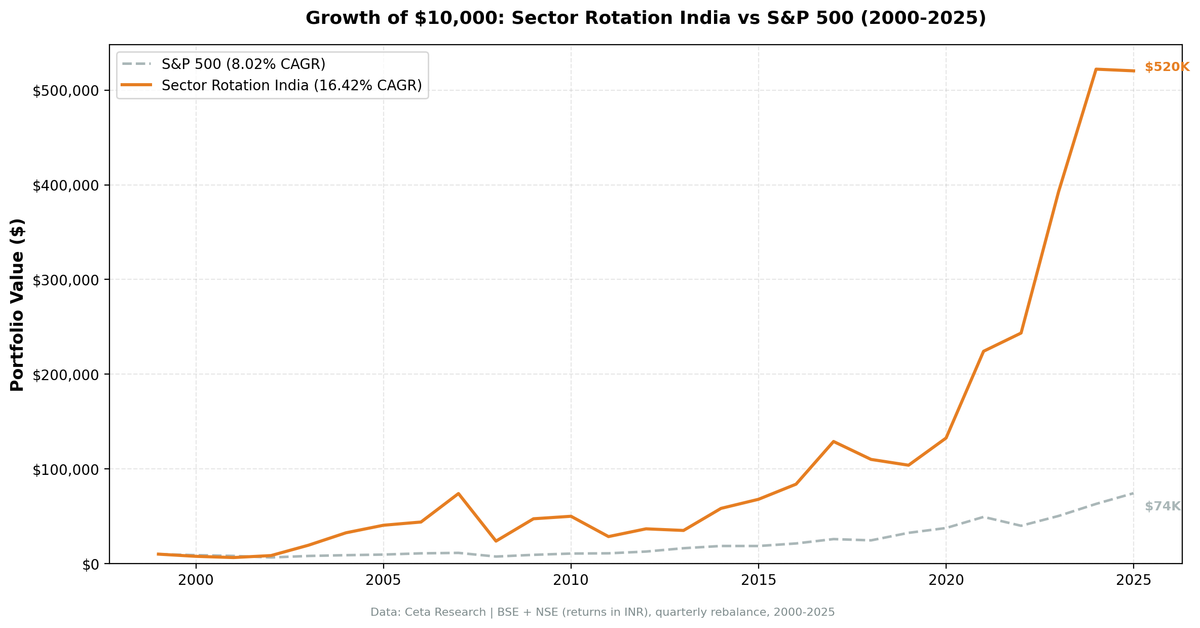

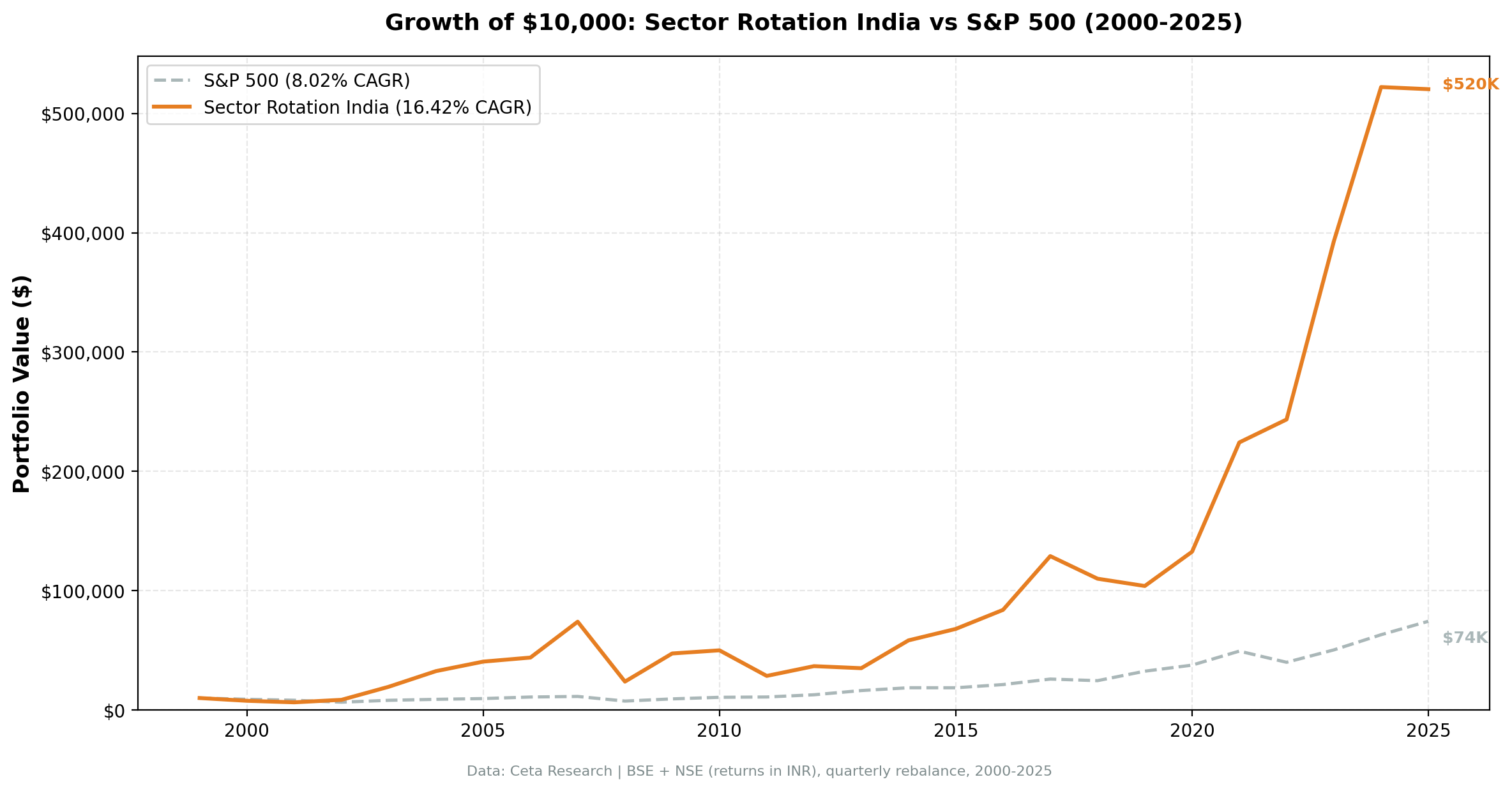

Sector Mean Reversion in India: 16.42% CAGR, 5105% Total Return, and

India's stock market rewards sector mean reversion handsomely. Over 26 years, buying the two most out-of-favor sectors on BSE and NSE each quarter produced 16.42% annually in INR, turning $10,000 into $520,500. That's +8.40% per year above SPY. The catch: you'll live through drawdowns that would end most systematic strategies.

Contents

- Method

- What We Found

- Most Selected Sectors (104 quarters)

- Notable Years

- Full Annual Returns

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: BSE + NSE (India), market cap > INR 10B (~$120M USD)

- Period: 2000-2025 (26 years, 104 quarterly periods)

- Rebalancing: Quarterly (January, April, July, October)

- Signal: Buy all stocks in the bottom 2 sectors by 12-month trailing equal-weighted return

- Portfolio construction: Equal weight all qualifying stocks in selected sectors

- Benchmark: S&P 500 Total Return (SPY)

- Cash rule: Hold cash if fewer than 5 stocks qualify

- Currency note: Returns are in INR (local currency). Benchmark is SPY in USD.

Historical financial data with 45-day lag to prevent look-ahead bias. Full methodology: backtests/METHODOLOGY.md

What We Found

India is the highest raw performer across all 14 exchanges we've tested. Not the best risk-adjusted, that's Korea, but in terms of raw CAGR and total return, nothing comes close. The strategy worked because India's market has large, cyclical sector swings. When Utilities, Telecom, or Real Estate fell out of favor, the mean reversion was violent and fast.

| Metric | Portfolio | S&P 500 |

|---|---|---|

| CAGR | 16.42% | 8.02% |

| Excess CAGR | +8.40% | — |

| Total Return | 5105% | — |

| Max Drawdown | -70.5% | -45.5% |

| Annualized Volatility | 37.47% | — |

| Sharpe Ratio | 0.265 | 0.357 |

| Win Rate (vs SPY) | 51.0% | — |

| Up Capture | 157.9% | — |

| Down Capture | 80.7% | — |

| Avg Stocks per Period | 132.8 | — |

| Cash Periods | 3 of 104 | — |

The 157.9% up capture is striking. When SPY goes up, this portfolio goes up 58% more. The down capture of 80.7% is decent, in falling markets, the portfolio falls about 80% as much as SPY. That asymmetry explains how the strategy compounds so aggressively over 26 years despite the brutal volatility.

The Sharpe of 0.265 is below SPY's 0.357. With 37.5% annualized volatility, the raw return isn't enough to overcome the risk-adjusted hurdle in the traditional sense. But 16.42% CAGR over 26 years isn't a number to dismiss, either.

Most Selected Sectors (104 quarters)

| Sector | Quarters Selected |

|---|---|

| Utilities | 38 |

| Communication Services | 36 |

| Real Estate | 28 |

| Healthcare | 24 |

| Technology | 19 |

| Consumer Defensive | 17 |

Utilities and Communication Services dominated. Both are sectors with long cyclical swings in India, periods of regulatory pressure, then recovery. Real Estate featured in 28 quarters, reflecting India's property cycles. Healthcare appeared surprisingly often, suggesting the sector underperformed for extended stretches before reverting.

Notable Years

2003: +129.01%. The standout year. Post-dot-com recovery coincided with India's infrastructure boom. The strategy caught Utilities and Telecom coming off multi-year lows. SPY returned +24.1%. The excess return of +104.9% in a single year is unusual even by India's volatile standards.

2008: -67.88%. The dark side of high-beta emerging market exposure. India's market fell harder than the US, and the strategy held cyclical sectors that amplified the drop. SPY lost -34.3%. This is when the -70.5% max drawdown accumulated, not entirely in 2008, but 2008 drove the peak-to-trough.

2009: +99.29%. The rebound was as violent as the collapse. Sectors that were destroyed in 2008 snapped back. The strategy returned 99.3% while SPY returned 24.7%. If you stayed in through 2008, the recovery was swift and complete.

2011: -42.90%. The strategy selected Communication Services and Real Estate coming into 2011. Both sectors continued to fall rather than revert. This is the core risk of mean reversion: you're buying sectors that have fallen, and sometimes they fall further. SPY returned +2.5% in 2011. The excess loss of -45.4% is the worst single-year gap in the backtest.

2019: -5.56%. SPY returned +32.3%. The -37.9% excess return is a significant strategy failure year, second only to 2011. The sectors selected didn't revert; India's market in 2019 was driven by a narrow set of quality growth names that the strategy was underweight.

2021: +69.10%. COVID recovery hit India's previously beaten-down sectors hard. Communication Services and Real Estate, which had been underperforming for years, reverted aggressively. SPY returned +31.3%.

Full Annual Returns

| Year | Portfolio | S&P 500 | Excess |

|---|---|---|---|

| 2000 | -23.20% | -10.50% | -12.69% |

| 2001 | -16.69% | -9.17% | -7.52% |

| 2002 | +32.55% | -19.92% | +52.47% |

| 2003 | +129.01% | +24.12% | +104.89% |

| 2004 | +67.52% | +10.24% | +57.28% |

| 2005 | +24.53% | +7.17% | +17.36% |

| 2006 | +8.39% | +13.65% | -5.25% |

| 2007 | +68.45% | +4.40% | +64.04% |

| 2008 | -67.88% | -34.31% | -33.57% |

| 2009 | +99.29% | +24.73% | +74.55% |

| 2010 | +5.55% | +14.31% | -8.75% |

| 2011 | -42.90% | +2.46% | -45.37% |

| 2012 | +28.67% | +17.09% | +11.58% |

| 2013 | -4.66% | +27.77% | -32.43% |

| 2014 | +66.59% | +14.50% | +52.10% |

| 2015 | +16.46% | -0.12% | +16.59% |

| 2016 | +23.49% | +14.45% | +9.04% |

| 2017 | +53.74% | +21.64% | +32.09% |

| 2018 | -14.68% | -5.15% | -9.53% |

| 2019 | -5.56% | +32.31% | -37.87% |

| 2020 | +27.62% | +15.64% | +11.99% |

| 2021 | +69.10% | +31.26% | +37.83% |

| 2022 | +8.58% | -18.99% | +27.57% |

| 2023 | +61.32% | +26.00% | +35.32% |

| 2024 | +32.93% | +25.28% | +7.65% |

| 2025 | -0.34% | +17.88% | -18.22% |

The pattern: large positive years are larger than the equivalent US numbers, and large negative years are also larger. India amplifies. The 51.0% win rate vs SPY is essentially a coin flip, but the wins are bigger than the losses, which is where the +8.40% excess CAGR comes from.

Backtest Methodology

| Parameter | Value |

|---|---|

| Signal | 12-month trailing equal-weighted sector return |

| Selection | Bottom 2 sectors each quarter |

| Universe | BSE + NSE, market cap > INR 10B |

| Portfolio | Equal weight all qualifying stocks in selected sectors |

| Rebalancing | Quarterly (Jan, Apr, Jul, Oct) |

| Cash rule | Hold cash if < 5 qualifying stocks |

| Transaction costs | Size-tiered model |

| Data lag | 45 days (prevents look-ahead bias) |

| Period | 2000-2025 (104 quarterly periods) |

| Benchmark | S&P 500 Total Return (SPY) |

Limitations

Currency risk. All returns are in INR. The S&P 500 benchmark is in USD. INR has depreciated against USD over the 26-year period, which means the real excess return for a USD-based investor is meaningfully lower than +8.40%. This comparison mixes currencies in a way that overstates USD-equivalent outperformance.

Maximum drawdown of -70.5%. This isn't a strategy for the faint-hearted. A 70.5% drawdown requires a 239% return just to break even. The recovery from 2008-2009 happened, but living through a 68% loss in a single year while holding isn't realistic for most investors.

High average stock count. The portfolio held an average of 132.8 stocks. For individual investors, replicating this exactly would require holding ~130 positions per quarter and rebalancing four times a year. Transaction costs in practice would likely exceed the model assumptions.

Emerging market data quality. BSE and NSE data before 2005 is thinner than post-2010 data. Early-period returns should be read with more caution than the more data-rich recent period.

Sector concentration. Utilities and Communication Services were selected in 74 of 104 quarters combined. This creates persistent sector bets, not true diversification across the market. In periods where both sectors decline simultaneously (2011, 2013), the portfolio has nowhere to hide.

Takeaway

India is a market that rewards mean reversion betting. The sectors are cyclical, the swings are large, and when the reversal comes, it comes fast. The 16.42% CAGR over 26 years is real. So is the -70.5% drawdown.

The strategy works in India because the market has the characteristics that make mean reversion strategies work anywhere: large sector-level mispricing driven by sentiment, sufficient time for those mispricings to correct, and a liquid enough market to implement the positions. What India adds is scale, the wins are bigger, the losses are bigger, and the compounding over time is larger.

USD-based investors should discount the returns for currency. INR has weakened against USD over the 26-year period, so the USD-equivalent CAGR is lower than 16.42%.

Part of a Series

- US analysis →. The benchmark: consistent returns across 104 quarters

- Korea analysis →. Best risk-adjusted globally: 0.466 Sharpe, 36.7% down capture

- Global comparison →, 14 exchanges, the full picture

References

Moskowitz, T. J., & Grinblatt, M. (1999). Do industries explain momentum? Journal of Finance, 54(4), 1249-1290.

Part of a Series: US | Global | Global | US | UK | Thailand | Taiwan | Taiwan

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse. Universe: BSE + NSE. Quarterly rebalance, equal weight, 2000-2025. Returns in INR. Past performance doesn't guarantee future results.