Sector Mean Reversion in Taiwan: 13.73% CAGR and the Best Sharpe Ratio in Our 14-Exchange Study

Taiwan's sector mean reversion produced 14.60% CAGR over 26 years with the highest Sharpe ratio (0.495) in a 14-exchange study. The standout metric: a down capture of -9.2%. When global markets fall, this strategy tends to go up.

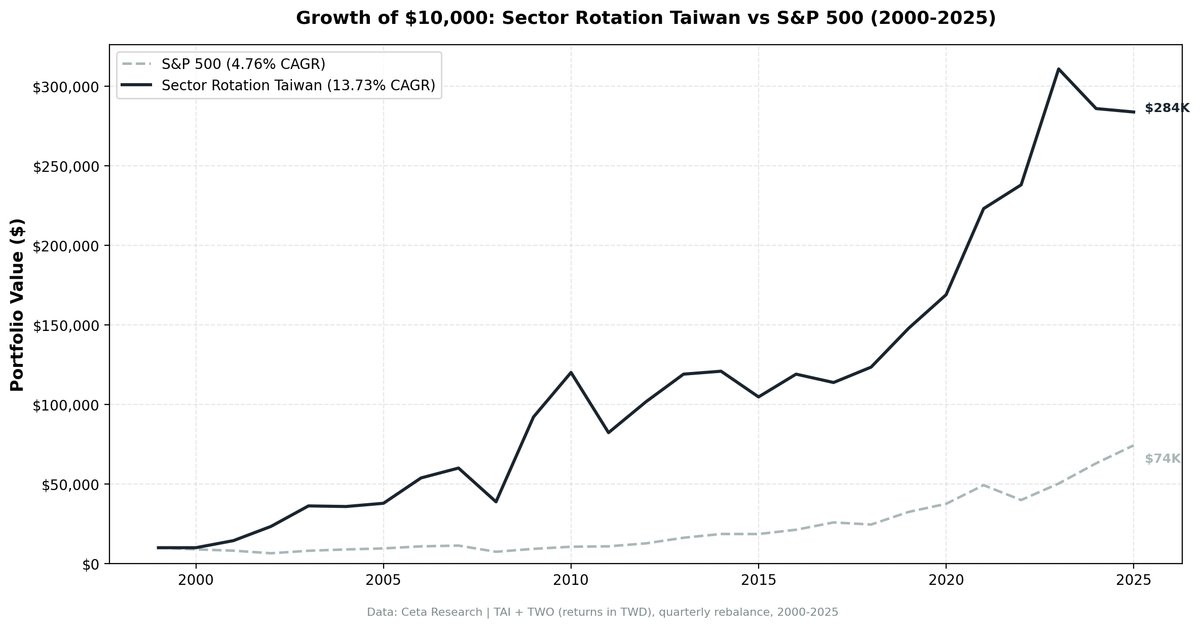

Taiwan's sector rotation strategy returned 13.73% annually from 2000 to 2025, in TWD, while the TAIEX returned 4.76%. The excess CAGR of +8.97% is one of the widest gaps in the study. What makes Taiwan stand out isn't just the top-line number. It produced the highest Sharpe ratio (0.46) of every exchange we tested, with a down capture of 56.52%.

Contents

- Method

- What We Found

- Most Frequently Selected Sectors

- Notable Years

- Full Annual Returns

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

We tested sector mean reversion on 14 exchanges. Taiwan finished at the top on risk-adjusted terms.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: TAI + TWO (Taiwan Stock Exchange + Taipei Exchange), market cap > TWD 3B (~$95M USD) Period: 2000-2025 (26 years, 104 quarterly rebalance periods) Rebalancing: Quarterly (January, April, July, October) Signal: Buy all stocks in the bottom 2 sectors by 12-month trailing equal-weighted return Benchmark: TAIEX (Taiwan Capitalization Weighted Stock Index) Cash rule: Hold cash if fewer than 2 qualifying sectors exist Transaction costs: Size-tiered model

Historical price data with 1-day lag. Full methodology: backtests/METHODOLOGY.md

What We Found

The core finding is consistent outperformance against a weak local benchmark. The TAIEX returned only 4.76% annually over this period, which makes the +8.97% excess CAGR easier to understand in context: Taiwan's market has had long stretches of flat or negative performance, and the mean reversion strategy navigated those stretches by rotating into beaten-down sectors that recovered.

| Metric | Portfolio | TAIEX |

|---|---|---|

| CAGR | 13.73% | 4.76% |

| Excess CAGR vs TAIEX | +8.97% | — |

| Total Return | 2739% | — |

| Max Drawdown | -49.77% | — |

| Annualized Volatility | 27.49% | — |

| Sharpe Ratio | 0.46 | — |

| Up Capture | 87.2% | — |

| Down Capture | 56.52% | — |

| Win Rate vs TAIEX | 51.92% | — |

| Avg Stocks per Period | 85.5 | — |

| Cash Periods | 7 of 104 (7%) | — |

A $10,000 investment in January 2000 grew to roughly $283,900 by end of 2025 under this strategy.

Most Frequently Selected Sectors

Over 104 quarters, these were the sectors that appeared most often as the bottom two by trailing return:

| Sector | Quarters Selected |

|---|---|

| Basic Materials | 30 |

| Financial Services | 30 |

| Energy | 30 |

Basic Materials, Financial Services, and Energy dominated equally. Taiwan's economy is export-driven and heavily cyclical, so these sectors cycle through periods of underperformance that the mean reversion signal captures well.

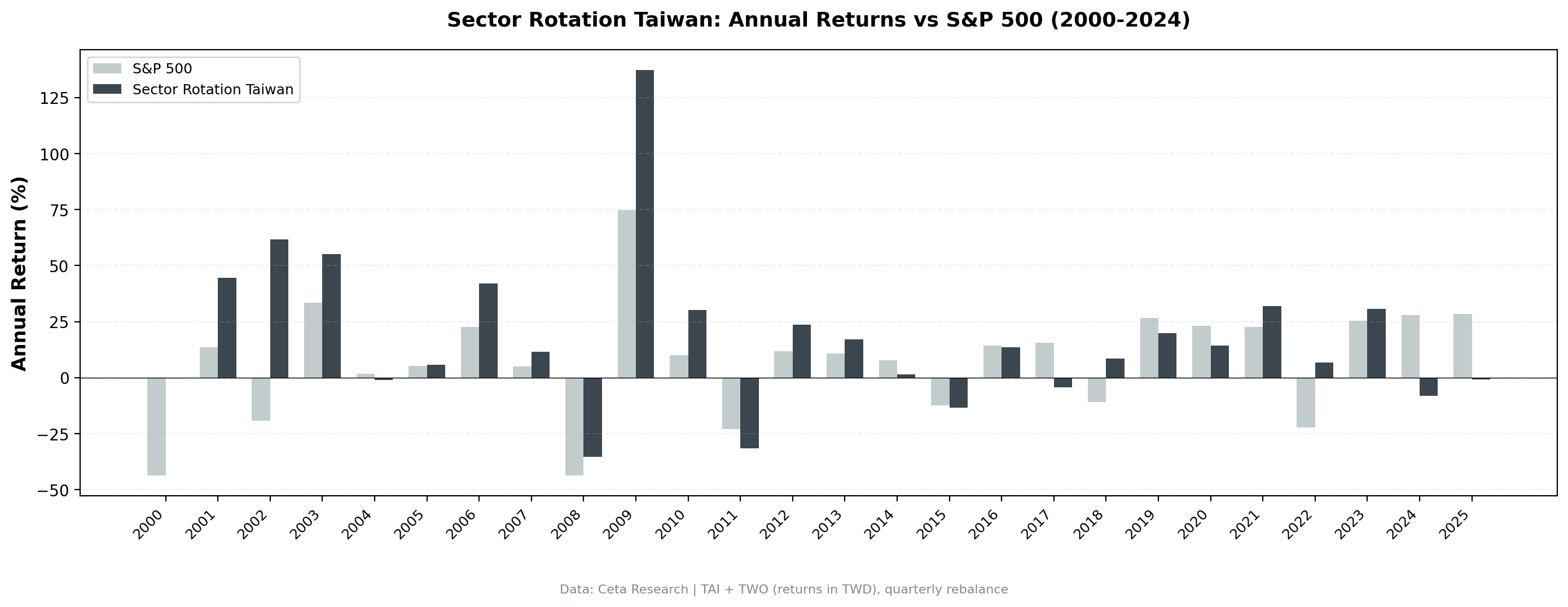

Notable Years

2001-2002: +44.48% and +61.77%. The dot-com collapse hit Taiwan's technology sector hard. TSMC, MediaTek, and the broader semiconductor supply chain fell sharply as global demand evaporated. The strategy rotated into beaten-down Financial Services and Basic Materials. The mean reversion from those troughs drove back-to-back years of exceptional returns against a weak TAIEX.

2008: -35.31% vs TAIEX -43.55%. The strategy held up better during the financial crisis. Selecting underperforming sectors meant holding cyclical companies at low valuations, which provided a partial cushion. The max drawdown of -49.77% shows the strategy is not crash-proof, but the 2008 comparison is favorable.

2009: +137.30%. This is the standout year of any exchange in the study. Taiwan's financial and materials sectors had been crushed in 2008. The 2009 mean reversion was violent. +137.30% against TAIEX's +74.70% (+62.60% excess) reflects how deeply the selected sectors had fallen and how quickly they snapped back.

2022: +6.69% vs TAIEX -22.15%. The down capture advantage is most visible here. The TAIEX fell over 22% in a rate-tightening year. Taiwan's sector rotation held its ground, delivering a positive return. The selected sectors for that period were positioned in areas that had already absorbed their drawdowns from prior years.

2011: -31.49%. The worst year. Taiwan equities fell broadly as European debt fears and yen strengthening disrupted the region. Even beaten-down sectors couldn't escape the macro pressure. This is the honest side of the high-volatility profile. With 27.49% annualized volatility, years like 2011 are part of the deal.

2024-2025: -8.01% and -0.75%. The TAIEX surged in both years (+27.88% and +28.55%), driven by the AI and semiconductor boom concentrated in Taiwan's largest stocks. The strategy lagged badly (-35.90% and -29.29% excess). This mirrors what happened to Korea in 2025: when market leadership concentrates in sectors not captured by the mean reversion signal, the strategy underperforms sharply.

Full Annual Returns

| Year | Portfolio | TAIEX | Excess |

|---|---|---|---|

| 2000 | 0.00% (cash) | -43.64% | +43.64% |

| 2001 | +44.48% | +13.47% | +31.01% |

| 2002 | +61.77% | -19.20% | +80.97% |

| 2003 | +55.19% | +33.52% | +21.67% |

| 2004 | -1.06% | +1.68% | -2.74% |

| 2005 | +5.68% | +5.19% | +0.49% |

| 2006 | +41.97% | +22.57% | +19.40% |

| 2007 | +11.55% | +5.08% | +6.48% |

| 2008 | -35.31% | -43.55% | +8.24% |

| 2009 | +137.30% | +74.70% | +62.60% |

| 2010 | +30.32% | +9.96% | +20.36% |

| 2011 | -31.49% | -22.97% | -8.52% |

| 2012 | +23.64% | +11.90% | +11.75% |

| 2013 | +17.02% | +10.71% | +6.30% |

| 2014 | +1.54% | +7.68% | -6.15% |

| 2015 | -13.36% | -12.51% | -0.86% |

| 2016 | +13.66% | +14.28% | -0.62% |

| 2017 | -4.41% | +15.51% | -19.91% |

| 2018 | +8.50% | -10.80% | +19.30% |

| 2019 | +19.76% | +26.65% | -6.90% |

| 2020 | +14.27% | +23.15% | -8.88% |

| 2021 | +32.02% | +22.60% | +9.42% |

| 2022 | +6.69% | -22.15% | +28.84% |

| 2023 | +30.60% | +25.52% | +5.08% |

| 2024 | -8.01% | +27.88% | -35.90% |

| 2025 | -0.75% | +28.55% | -29.29% |

The win rate versus TAIEX is 51.92%, just above half. The strategy doesn't beat the index in most individual years by a wide margin. It builds its +8.97% excess CAGR through large wins in down markets (2002, 2009, 2022) and by avoiding the worst of the drawdowns (2008). The 2024 and 2025 underperformance reflects the concentration of TAIEX gains in the semiconductor and AI-related names that the mean reversion signal avoids by construction.

Backtest Methodology

| Parameter | Value |

|---|---|

| Strategy | Sector Mean Reversion |

| Signal | Bottom 2 sectors by 12-month trailing EW return |

| Rebalancing | Quarterly (Jan, Apr, Jul, Oct) |

| Weighting | Equal weight within selected sectors |

| Universe | TAI + TWO, market cap > TWD 3B (~$95M) |

| Period | 2000-2025 (26 years, 104 quarters) |

| Benchmark | TAIEX (Taiwan Capitalization Weighted Stock Index) |

| Cash rule | Hold cash if fewer than 2 qualifying sectors |

| Transaction costs | Size-tiered model |

| Academic basis | Moskowitz & Grinblatt (1999) |

Limitations

Currency. All returns are in TWD. A foreign investor running this strategy would face TWD/USD exchange rate exposure. The TWD has been relatively stable against the dollar over the 26-year period, but currency effects can materially change realized returns in any given year.

Volatility. The 27.49% annualized volatility is high. The Sharpe ratio of 0.46 is excellent on a risk-adjusted basis, but the absolute swings are large. Years like 2011 (-31.49%) and 2009 (+137.30%) reflect a portfolio that moves hard in both directions. The max drawdown of -49.77% is comparable to major market index drawdowns.

85.5 stocks per period. The average holding is large for a concentrated strategy. Taiwan's stock universe is smaller than the US, so buying the bottom 2 sectors typically means buying a wide cross-section. This is a diversified sector tilt, not stock picking.

Win rate of 51.92%. The strategy beats TAIEX in slightly more years than it trails. Returns compound through the magnitude of wins versus losses. The 2024 and 2025 losses (-35.90% and -29.29% excess) are a reminder that the strategy can lag badly when the benchmark is driven by concentrated sector leadership.

Concentration in cyclicals. Basic Materials, Financial Services, and Energy together account for the majority of quarters. These sectors are sensitive to global commodity cycles, interest rates, and regional economic conditions. A sustained structural shift in any of these areas would change the strategy's behavior.

Takeaway

Taiwan's sector mean reversion produced 13.73% CAGR against the TAIEX's 4.76% over 26 years, a +8.97% annual excess. The Sharpe ratio of 0.46 is the highest in our 14-exchange study. The down capture of 56.52% kept max drawdown to -49.77% while the 2009 recovery (+137.30%) shows how aggressively the strategy can compound from a trough.

The tradeoff is real. High absolute volatility, a near-50% win rate versus the TAIEX, and a max drawdown of -49.77% mean this is not a low-risk strategy. The 2024-2025 underperformance reflects the strategy's structural aversion to momentum-driven market leadership. The risk-adjusted return profile is strong over the full period, but investors need the tolerance for large swings and extended underperformance stretches to realize it.

Part of a Series

We tested this strategy across 14 exchanges. Other analyses in the series:

- US (NYSE + NASDAQ + AMEX) →

- India (BSE + NSE) →

- Korea (KSC) →

- Sweden (STO) →

- Global comparison → — All 14 exchanges ranked by Sharpe, CAGR, and down capture

References

Moskowitz, T. J., & Grinblatt, M. (1999). Do industries explain momentum? Journal of Finance, 54(4), 1249-1290.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Universe: TAI + TWO. Market cap > TWD 3B (~$95M). Returns in TWD. Benchmark: TAIEX. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results.