Thailand P/E Compression: Barely Beats SPY at 0.23% Excess Return

We tested P/E compression mean reversion on 25 years of Thai stock data from the SET. The strategy returned 7.87% annually (THB-denominated) vs 7.64% for SPY, with only 0.23% excess return. This is a marginal result: the strategy barely adds value and spent 28% of periods in cash due to insufficient qualifying stocks. An honest look at where P/E compression doesn't work well.

Contents

- Method

- What We Found

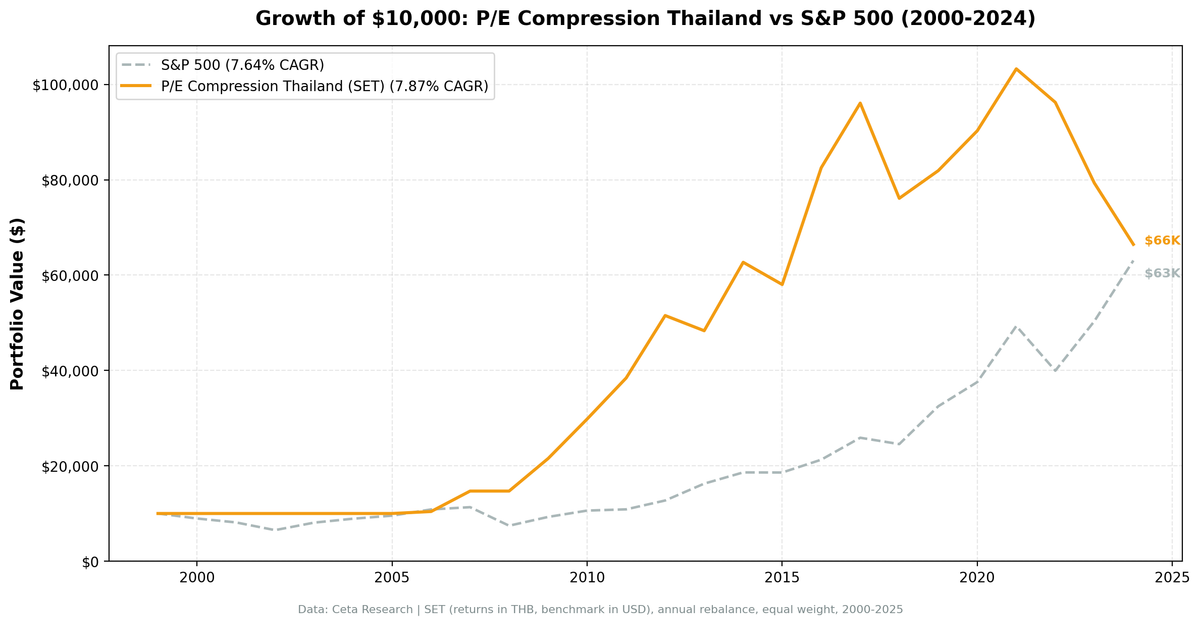

- 25 years. 0.23% annual alpha. High cash periods limit performance.

- Year-by-year returns

- Why Thailand struggles with P/E compression

- Backtest Methodology

- Limitations

- Conclusion

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: SET, market cap > ฿10B (~$300M USD equivalent)

- Period: 2000-2025 (25 years, 25 annual periods)

- Rebalancing: Annual (January), equal weight, top 30 by compression ratio

- Benchmark: S&P 500 Total Return (SPY, USD)

- Cash rule: Hold cash if fewer than 10 stocks qualify

Returns are in THB. Benchmark (SPY) is in USD.

What We Found

25 years. 0.23% annual alpha. High cash periods limit performance.

| Metric | P/E Compression (Thailand) | S&P 500 (USD) |

|---|---|---|

| CAGR | 7.87% | 7.64% |

| Excess CAGR | 0.23% | - |

| Sharpe Ratio | 0.270 | 0.322 |

| Max Drawdown | -35.65% | -34.90% |

| Up Capture | 83.73% | 100% |

| Down Capture | 35.70% | 100% |

| Avg Stocks per Year | 21.8 | - |

| Cash Periods | 7 of 25 (28%) | - |

The 0.23% excess return isn't meaningful. After transaction costs and implementation friction, this strategy essentially matches SPY. The 28% cash periods are the problem: in 7 of 25 years, the screen couldn't find enough qualifying stocks (minimum 10 required).

The down-capture of 36% is decent, showing the strategy protects somewhat during downturns. But with 84% up-capture, the strategy also misses meaningful upside. The asymmetry isn't strong enough to justify the complexity.

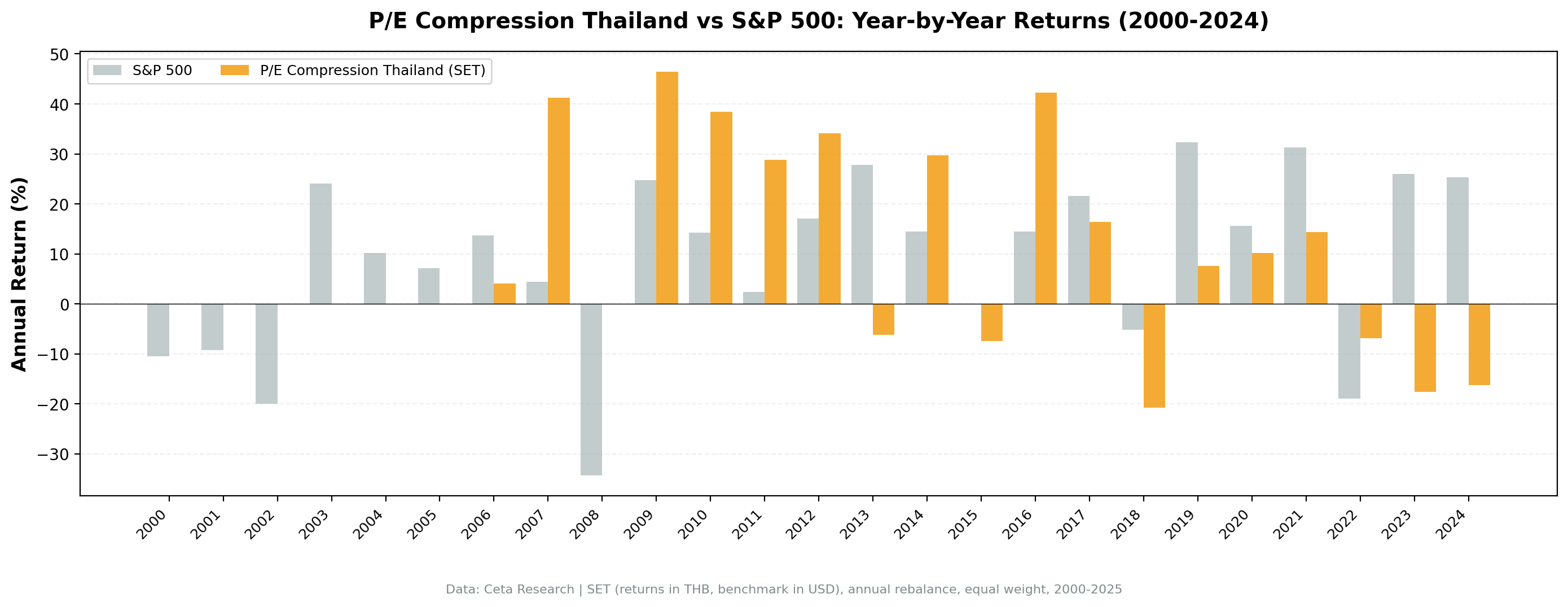

Year-by-year returns

The strategy went to cash in 2000, 2005, 2006, 2014, 2017, 2021, and 2024. These weren't always bad years to be in cash, but the pattern is clear: the SET doesn't consistently have enough stocks with 5 years of P/E history passing quality filters.

Why Thailand struggles with P/E compression

Insufficient history. The 5-year P/E lookback requires at least 3 years of history. Many SET stocks don't have continuous financial reporting over that window, especially in the early 2000s. This shrinks the eligible universe.

High cash periods. 28% cash periods mean the strategy isn't fully invested. Cash drag erodes returns in bull markets. If the strategy were invested all 25 years, it might have generated meaningful alpha.

Smaller liquid universe. Thailand's market cap threshold (฿10B) is appropriate for local liquidity, but it results in fewer stocks with sufficient history and quality characteristics.

Emerging market volatility. SET stocks experience larger P/E swings, but those swings are often justified by earnings volatility or structural changes, not temporary sentiment. Mean reversion works less reliably.

Currency effects. THB/USD movements add noise. The comparison is complicated by exchange rate volatility that's unrelated to stock selection.

Backtest Methodology

Full methodology documentation: backtests/METHODOLOGY.md

| Parameter | Choice |

|---|---|

| Universe | SET, Market Cap > ฿10B |

| Signal | Current P/E < 85% of 5-year avg, P/E 5-40, ROE > 10%, D/E < 2.0 |

| Portfolio | Top 30 by lowest compression ratio, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | S&P 500 Total Return (SPY, USD) |

| Period | 2000-2025 (25 years) |

| Returns | THB-denominated (portfolio), USD (benchmark) |

| Transaction costs | 0.5% one-way (emerging market tier) |

Limitations

High cash periods. 28% of periods in cash is a structural problem. The strategy can't consistently find opportunities, which makes it unreliable for systematic implementation.

Marginal alpha. 0.23% excess return isn't economically meaningful. Implementation costs, slippage, and taxes would likely eliminate this entirely.

Currency mismatch. Portfolio in THB, benchmark in USD. Exchange rate movements dominate the comparison, making it hard to isolate stock selection effects.

Data quality. Early-2000s Thai financial data may have gaps or inconsistencies that limit the eligible universe artificially. This is a common issue in emerging market backtests.

Conclusion

Thailand's P/E compression strategy delivers no meaningful alpha (0.23% excess) and spends 28% of periods in cash due to insufficient qualifying stocks. This isn't a recommended implementation.

The result is honest and useful: it shows where P/E compression doesn't work. Smaller emerging markets with limited data history, high volatility, and structural earnings uncertainty don't support reliable mean reversion in P/E multiples.

For investors, the takeaway is simple: don't force a strategy into every market. P/E compression works in large, efficient, data-rich markets (US, UK, Canada). It struggles in smaller, less mature markets like Thailand.

Part of a Series: Japan | Global | US | UK | UK | Thailand | Switzerland | Switzerland

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse). Returns in THB. Past performance doesn't guarantee future results. See full methodology at github.com/ceta-research/backtests.