P/E Compression Across 19 Markets: The Strategy That Works in the

We ran the same P/E compression screen across 19 exchanges globally: find stocks where the current annual P/E has compressed 15%+ below the company's own 5-year historical average, with fundamentals still intact. The results reveal a consistent geographic pattern that hasn't shown up this clearly in our other strategy backtests.

Contents

- Method

- The Pattern

- What's Driving the Split

- Where It Works: The "Mean Reversion" Environment

- Where It Fails: The "Structural Discount" Markets

- Germany: The Interesting Exception

- Japan: Not Quite Either

- Cash Periods as a Data Point

- Takeaway

- Run It Yourself

- Regional Analyses

In US, UK, and Canadian markets: the strategy outperforms. In Asian markets. China, Hong Kong, India, Korea, it fails, sometimes badly. Germany sits in the middle, underperforming despite clean data and a full 25-year history.

This isn't noise. It's a signal about how valuation compression is interpreted differently across market structures.

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: 19 exchanges, full exchange universe (not index-constrained), market cap > exchange-specific threshold

- Period: 2000-2025 (25 annual rebalance periods)

- Rebalancing: Annual (January), equal weight top 30 per exchange by compression score

- Benchmark: S&P 500 Total Return (SPY, USD)

- Currency note: All exchange returns are in local currency. Benchmark is USD. Direct comparison has currency effects.

Signal: current annual P/E < 85% of the company's 5-year FY average, with ROE > 10%, D/E < 2.0, P/E 5-40.

Full methodology: backtests/METHODOLOGY.md

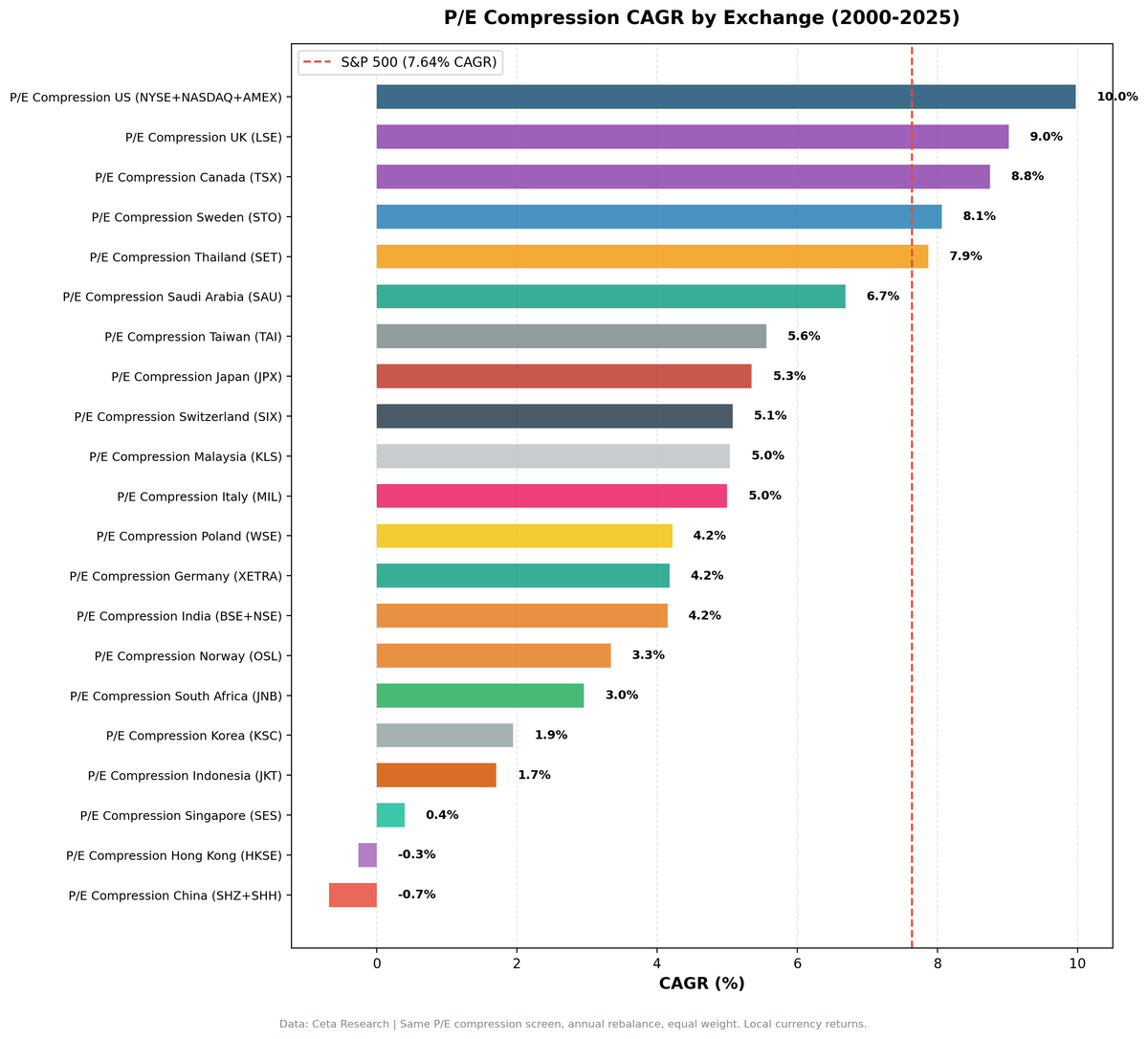

The Pattern

| Exchange | CAGR | vs SPY | Sharpe | MaxDD | Cash% | Avg Stocks |

|---|---|---|---|---|---|---|

| US (NYSE+NASDAQ+AMEX) | 9.97% | +2.32% | 0.382 | -42.82% | 0% | 25.4 |

| UK (LSE) | 9.02% | +1.38% | 0.253 | -39.85% | 0% | 14.0 |

| Canada (TSX) | 8.75% | +1.11% | 0.347 | -28.99% | 0% | 23.2 |

| Sweden (STO) | 8.06% | +0.41% | 0.313 | -32.26% | 40% | 22.1 |

| Thailand (SET) | 7.87% | +0.23% | 0.270 | -35.65% | 28% | 21.8 |

| Saudi Arabia (SAU) | 6.69% | -0.95% | 0.210 | -19.33% | 44% | 16.5 |

| Taiwan (TAI) | 5.56% | -2.08% | 0.236 | -14.99% | 36% | 27.7 |

| Japan (JPX) | 5.35% | -2.29% | 0.261 | -50.89% | 16% | 28.0 |

| Switzerland (SIX) | 5.08% | -2.56% | 0.264 | -40.68% | 4% | 15.0 |

| Malaysia (KLS) | 5.04% | -2.60% | 0.221 | -17.91% | 48% | 12.5 |

| Italy (MIL) | 5.00% | -2.64% | 0.085 | -47.73% | 48% | 13.2 |

| Poland (WSE) | 4.22% | -3.43% | 0.154 | -20.84% | 56% | 14.1 |

| Germany (XETRA) | 4.18% | -3.46% | 0.123 | -42.21% | 0% | 19.7 |

| India (BSE+NSE) | 4.15% | -3.50% | -0.071 | -57.67% | 24% | 24.3 |

| South Africa (JNB) | 2.96% | -4.68% | -0.385 | -36.18% | 44% | 13.4 |

| Korea (KSC) | 1.95% | -5.70% | -0.074 | -26.0% | 40% | 26.4 |

| Indonesia (JKT) | 1.71% | -5.93% | -0.023 | -25.98% | 44% | 21.4 |

| Hong Kong (HKSE) | -0.26% | -7.91% | -0.114 | -61.39% | 8% | 20.3 |

| China (SHZ+SHH) | -0.68% | -8.32% | -0.083 | -63.70% | 0% | 23.9 |

Cash% = percentage of years when fewer than 10 qualifying stocks were found and the portfolio held cash. Note on Sweden: positive excess return but 40% cash periods, strategy fired too infrequently for a reliable dedicated test.

Outperformers (positive excess CAGR): US, UK, Canada, Sweden (high cash), Thailand (borderline) Underperformers (negative excess CAGR): 14 of 19 exchanges

The S&P 500 benchmark is 7.64% CAGR over the period. Only 3 exchanges clearly beat it. This is an honest result.

What's Driving the Split

Where It Works: The "Mean Reversion" Environment

US, UK, and Canada share characteristics that make P/E mean reversion viable:

Mature, liquid markets. When a quality company's P/E compresses in these markets, it's often sector rotation, macro fear, or temporary earnings disappointment, not structural change. The mean reversion mechanism works because the underlying business quality is observable and the market eventually reprices it.

Value-weighted composition. The LSE and TSX are heavily weighted toward financials, energy, and materials, sectors with natural PE cycles. A compressed Canadian energy company at 12x vs its historical 20x is often genuinely cheap, not permanently repriced. The signal fires on the right companies.

Canada's extreme defensiveness. The TSX version produced the most unusual result: only 23.7% down capture. The portfolio absorbed less than a quarter of the S&P 500's downside in down years. The same compression signal, applied to a market with lower technology concentration and more cyclical depth, selected for businesses with far lower correlation to US market moves.

Where It Fails: The "Structural Discount" Markets

In China, Hong Kong, India, and Korea, the results are consistently negative. The strategy fires, there are plenty of qualifying stocks in all these markets, but the signal doesn't predict positive mean reversion.

China (SHZ+SHH): -0.68% CAGR, -8.32% excess. Zero cash periods means the strategy was always invested with 24 stocks on average. The signal fired but the returns were negative. Chinese value stocks have traded at structural discounts for a decade, compressed P/Es in China often mean the market correctly assigned a lower multiple due to governance, capital allocation, or macro risks.

Hong Kong (HKSE): -0.26% CAGR, -7.91% excess, 132.6% down capture. The down capture is the telling number. When global markets fell, Hong Kong P/E compression names fell more than the S&P 500. Compressed multiples became more compressed, then more compressed again.

India (BSE+NSE): 4.15% CAGR, -3.50% excess. India earned positive returns (the market went up over 25 years) but the compression signal added no alpha and worse risk (57.7% max drawdown, 101.8% down capture). The strategy matched the market's performance while losing more in crashes.

Korea (KSC): 1.95% CAGR, 40% cash. Korean value stocks have the "Korea discount", compressed multiples due to chaebol governance concerns and geopolitical risk. The compression signal picks up cheap companies but the re-rating doesn't happen.

Germany: The Interesting Exception

Germany (XETRA) defies the simple East-West story: 4.18% CAGR, -3.46% excess, 0% cash, 19.7 average stocks. The data is clean. The strategy found plenty of qualifying names every year. But it consistently underperformed.

XETRA sits between the clean mean-reversion environment of the UK/Canada and the structural-discount environment of Asia. German listed companies often have compressed P/Es for real reasons: cyclical exposure, export dependency, energy costs, or demographic headwinds. The quality filters (ROE > 10%, D/E < 2) capture some of this, but not all.

Germany's underperformance suggests that compressed P/Es in export-oriented industrial economies may reflect genuine macro risk repricing rather than temporary sentiment.

Japan: Not Quite Either

Japan (JPX): 5.35% CAGR, -2.29% excess, positive Sharpe (0.261). The only major Asian market with both clean data and a positive risk-adjusted return, just not a better return than the benchmark.

The "Japan discount" has been a known phenomenon for decades: Japanese companies trade at structurally lower multiples due to low ROE targets, excess cash hoarding, and historical governance issues. But Japan has been actively addressing this under the TSE governance reforms that began in 2023. The compression signal may work better in Japan going forward than it has historically.

Cash Periods as a Data Point

Some exchanges had high cash periods, meaning the signal fires infrequently there:

- Norway: 80% cash (only 5 invested years, results excluded from this table)

- Singapore: 52% cash, 7.8 avg stocks (excluded, too thin)

- Poland: 56% cash, Malaysia: 48% cash, Italy: 48% cash

For these markets, the PE compression signal with quality filters is too strict. The universe of qualifying stocks is too small to reliably build a 10+ stock portfolio. This suggests either the quality filters need recalibration or the strategy isn't suited to these markets at this threshold.

Takeaway

P/E compression mean reversion is a real phenomenon in Western markets. The mechanism, quality businesses temporarily repriced below their historical valuation norms, followed by re-rating, works in the US, UK, and Canada over a 25-year period with consistent frequency.

In Asian markets, the same signal selects for structurally cheap stocks that stay cheap. The compression is correct pricing, not temporary mispricing. The quality filters (ROE, D/E) aren't enough to separate the two.

Whether to use this strategy should depend on where you're investing, not just whether a P/E is below historical average.

Part of a Series: Japan | US | UK | UK | Thailand | Thailand | Switzerland | Switzerland

Run It Yourself

git clone https://github.com/ceta-research/backtests.git

cd backtests

# Run all exchanges

python3 pe-compression/backtest.py --global --output results/exchange_comparison.json --verbose

# Run specific exchange

python3 pe-compression/backtest.py --preset uk --output results.json

# Current screen (any exchange)

python3 pe-compression/screen.py --preset us

python3 pe-compression/screen.py --preset india

Regional Analyses

- US →, 9.97% CAGR, +2.32% excess, down capture 68.6%

- UK →, 9.02% CAGR, +1.38% excess, down capture 59.7%

- Canada →, 8.75% CAGR, +1.11% excess, down capture 23.7%

- Thailand →, 7.87% CAGR, +0.23% excess, down capture 35.7%

- Japan →, 5.35% CAGR, -2.29% excess, positive Sharpe

- Switzerland →, 5.08% CAGR, -2.56% excess, 15 avg stocks

- Germany →, 4.18% CAGR, -3.46% excess, 0% cash

- India →, 4.15% CAGR, -3.50% excess, negative Sharpe

- Hong Kong →, -0.26% CAGR, -7.91% excess, 132.6% down capture

- China →, -0.68% CAGR, -8.32% excess, A-share market analysis

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. All returns in local currency. Benchmark: SPY (USD). Full methodology: METHODOLOGY.md. Past performance doesn't guarantee future results.