Yield Gap UK: The Best-Performing Market in Our 20-Exchange Study

Contents

- The Strategy

- Methodology

- Results

- What Drives the UK Outperformance

- Why the UK Works for Value Investing

- Run It Yourself

- Limitations

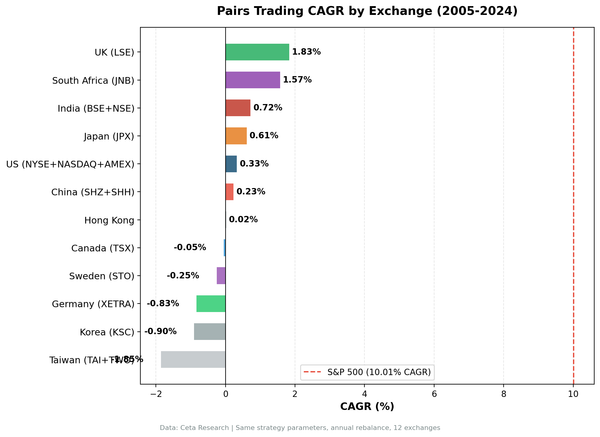

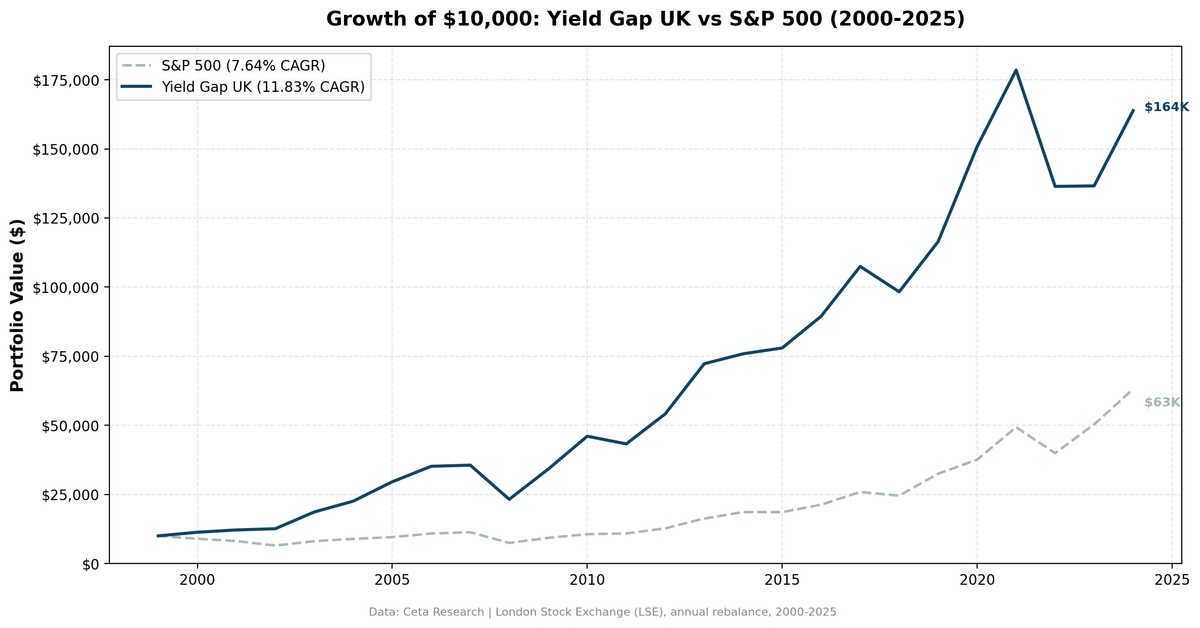

We tested the yield gap strategy across 20 equity markets. The UK came first. London Stock Exchange stocks with earnings yields 3+ percentage points above UK gilt rates returned 11.83% CAGR from 2000 to 2025, vs 7.64% for SPY. That's +4.19% annually, compounding over 25 years.

A $10,000 investment in January 2000 grew to $163,848. The same investment in SPY grew to $63,066.

The Strategy

The yield gap compares a stock's earnings yield (1/PE ratio) to the prevailing risk-free rate. For UK stocks, we use a 3.5% risk-free rate, reflecting the long-run average UK gilt yield. This sets the effective threshold at 6.5% earnings yield (PE < ~15.4x), slightly more demanding than the 6% US threshold.

Signal: - Earnings yield > max(6%, rfr + 3%) = 6.5% for UK (PE < ~15.4x) - Earnings yield < 50% - ROE > 8% - D/E < 2.0

Portfolio construction: Top 30 by highest earnings yield, equal weight, annual January rebalance. Cash if fewer than 10 stocks qualify.

Methodology

- Universe: London Stock Exchange (LSE)

- Market cap filter: £500M+ at each rebalance date

- Data period: January 2000 through December 2025 (25 annual periods, 0 cash years)

- Rebalancing: Annual (January)

- Point-in-time data: FY filings with 45-day filing lag

- Transaction costs: Size-tiered model

- Benchmark: SPY (used for all exchanges as the global capital cost benchmark)

- Data source: Ceta Research FMP financial data warehouse

Full methodology at github.com/ceta-research/backtests/blob/main/METHODOLOGY.md.

Results

| Metric | Yield Gap UK | SPY |

|---|---|---|

| CAGR | 11.83% | 7.64% |

| Total return (25yr) | 1,538.5% | 530.7% |

| Max drawdown | -34.75% | -45.50% |

| Sharpe ratio | 0.423 | — |

| Down capture vs SPY | 40.8% | — |

| Win rate vs SPY | 56.0% | — |

| Cash periods | 0 of 25 years | — |

| Avg stocks (invested) | 17.5 | — |

Two numbers stand out. First, the down-capture of 40.8%: when SPY fell, this portfolio on average fell less than half as much. Second, the max drawdown of -34.75% vs -45.50% for SPY, the strategy endured less peak-to-trough damage while delivering more return.

UK value stocks have long had a reputation for being better priced than their US counterparts. The data here supports that. The London market has consistently produced larger pools of high-earnings-yield, quality companies than US markets in relative terms, partly because UK investors have historically been more risk-averse and willing to pay dividends rather than growth premiums.

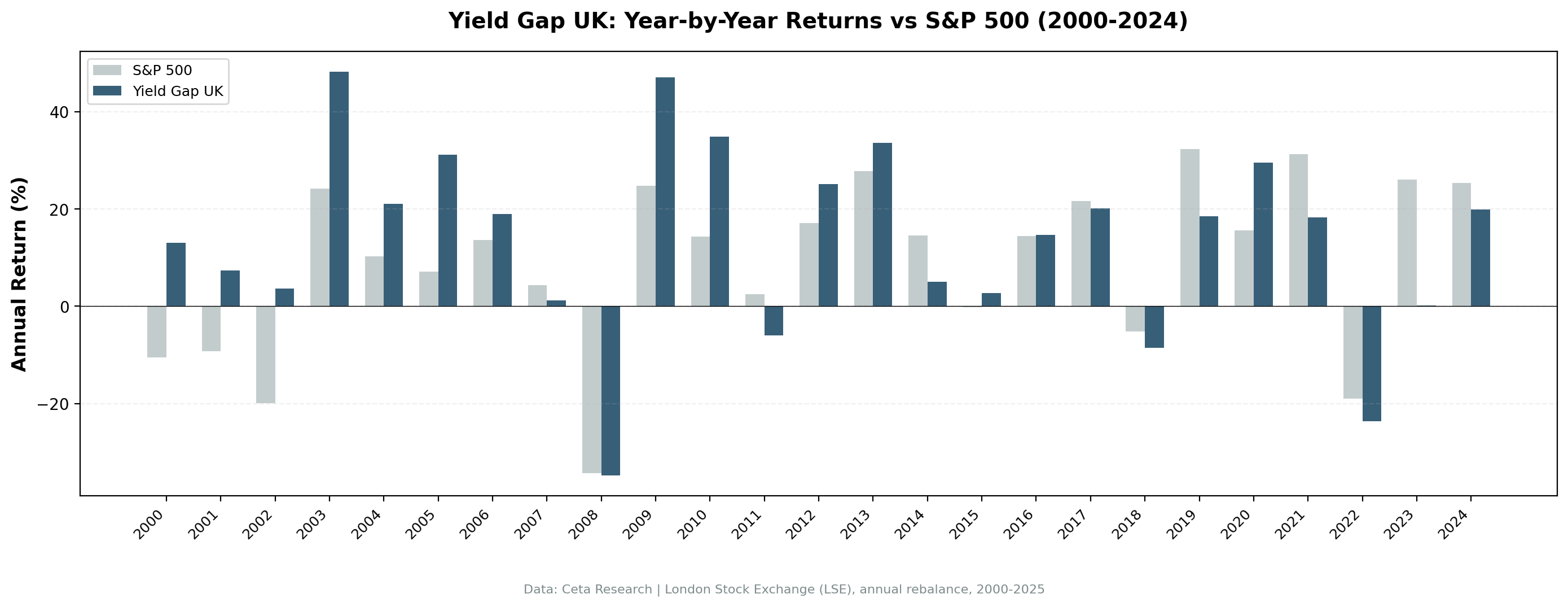

Annual returns:

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2000 | +13.06% | -10.50% | +23.56% |

| 2001 | +7.40% | -9.17% | +16.57% |

| 2002 | +3.61% | -19.92% | +23.53% |

| 2003 | +48.19% | +24.12% | +24.07% |

| 2004 | +20.99% | +10.24% | +10.75% |

| 2005 | +31.08% | +7.17% | +23.91% |

| 2006 | +18.96% | +13.65% | +5.31% |

| 2007 | +1.17% | +4.40% | -3.23% |

| 2008 | -34.75% | -34.31% | -0.44% |

| 2009 | +47.08% | +24.73% | +22.35% |

| 2010 | +34.84% | +14.31% | +20.53% |

| 2011 | -6.03% | +2.46% | -8.49% |

| 2012 | +25.05% | +17.09% | +7.96% |

| 2013 | +33.56% | +27.77% | +5.79% |

| 2014 | +5.00% | +14.50% | -9.50% |

| 2015 | +2.76% | -0.12% | +2.88% |

| 2016 | +14.72% | +14.45% | +0.27% |

| 2017 | +20.16% | +21.64% | -1.48% |

| 2018 | -8.56% | -5.15% | -3.41% |

| 2019 | +18.50% | +32.31% | -13.81% |

| 2020 | +29.53% | +15.64% | +13.89% |

| 2021 | +18.31% | +31.26% | -12.95% |

| 2022 | -23.57% | -18.99% | -4.58% |

| 2023 | +0.15% | +26.00% | -25.85% |

| 2024 | +19.92% | +25.28% | -5.36% |

What Drives the UK Outperformance

The dotcom bust gave UK value a massive head start. From 2000 to 2005, the UK portfolio delivered six consecutive years of positive returns while SPY spent three years in the red. UK markets had less exposure to the late-1990s technology valuations that drove US growth stocks to extreme multiples. Earnings-yield investing in the UK during this period meant owning industrial, energy, and financial companies that simply kept earning.

2008 was different. The UK portfolio fell -34.75% in 2008, nearly identical to SPY's -34.31%. The financial crisis hit UK banks and insurers hard, and the LSE had significant exposure to those sectors. There was no defensive cushion in 2008. The recovery, though, was strong: +47.08% in 2009 vs +24.73%.

2020 showed the strategy's defensive strength in a different crisis. During COVID, UK yield gap stocks returned +29.53% vs +15.64% for SPY. UK value stocks had sold off more severely during the initial COVID crash, then recovered sharply once the market recognized the businesses remained intact.

2023 was the worst year. The portfolio returned +0.15% vs +26.00% for SPY (-25.85% relative). This was a year of heavy concentration in SPY, the Magnificent Seven dominated returns, and earnings-yield screens had zero exposure to any of those names. This is a structural limitation of the strategy, not a random bad year.

Why the UK Works for Value Investing

The UK market has structural characteristics that favor earnings-yield strategies. The corporate culture emphasizes dividends over buybacks and growth reinvestment. Accounting standards and governance norms tend toward conservative financial reporting. The market has historically attracted investors who think in terms of yield and fundamental value rather than growth optionality.

This means high-earnings-yield UK stocks are often genuinely cheap, temporarily ignored by growth-oriented global capital flows, rather than cheap for structural reasons. The UK discount to global markets has been a recurring feature since 2016, and earnings-yield screens have harvested some of that discount consistently.

Part of a Series: Global | US | Sweden | India | Canada

Run It Yourself

Current UK yield gap screen:

SELECT

k.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(k.earningsYieldTTM * 100, 2) AS earnings_yield_pct,

ROUND(1.0 / NULLIF(k.earningsYieldTTM, 0), 1) AS implied_pe,

ROUND(k.returnOnEquityTTM * 100, 2) AS roe_pct,

ROUND(fr.debtToEquityRatioTTM, 2) AS debt_to_equity,

ROUND(k.freeCashFlowYieldTTM * 100, 2) AS fcf_yield_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM key_metrics_ttm k

JOIN profile p ON k.symbol = p.symbol

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

WHERE k.earningsYieldTTM > 0.065 -- EY > 6.5% (rfr=3.5%+3%)

AND k.earningsYieldTTM < 0.50

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL

OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 500000000 -- £500M+

AND (p.industry IS NULL OR p.industry NOT LIKE 'Asset Management%')

AND (p.industry IS NULL OR p.industry NOT LIKE 'Shell Companies%')

AND p.exchange IN ('LSE')

ORDER BY k.earningsYieldTTM DESC

LIMIT 30

Run this query on Ceta Research Data Explorer

Full backtest:

git clone https://github.com/ceta-research/backtests.git

cd backtests

pip install -r requirements.txt

python3 yield-gap/backtest.py --preset uk --output results.json --verbose

Limitations

Currency risk not modeled: Returns are in local currency (GBP). A USD-based investor would face GBP/USD fluctuations on top of the equity returns. GBP weakened after Brexit (2016) and during the 2022 Truss budget crisis, both periods would have reduced USD returns.

Small average portfolio: The strategy averaged 17.5 stocks when invested, below the 22-30 range of other markets. Concentration risk is higher. A single sector event (2008 financials) can dominate the portfolio.

Political and regulatory risk: UK markets carry Brexit-related risks, financial regulation changes, and tax policy uncertainty that don't appear in the backtest data.

Survivorship bias and FMP coverage: LSE coverage in FMP is broad but may underrepresent smaller companies that were acquired or delisted mid-period.

Data: Ceta Research (FMP financial data warehouse), January 2000 through December 2025. Full methodology: github.com/ceta-research/backtests/blob/main/METHODOLOGY.md.

Academic references: Campbell, J.Y. & Vuolteenaho, T. (2004). "Bad Beta, Good Beta." American Economic Review, 94(5). Damodaran, A. (2012). "Equity Risk Premiums (ERP): Determinants, Estimation and Implications." Stern School of Business.