Yield Gap Sweden: Strong Alpha with a 76% Win Rate vs Local Index (2000-2025)

We ran the yield gap strategy on Stockholm Stock Exchange stocks from 2000 to 2025. The result: 10.61% CAGR vs 2.95% for OMX Stockholm 30 (+7.66% excess), with a 76% annual win rate against the local index.

title: "Yield Gap Sweden: Strong Alpha with a 76% Win Rate vs Local Index (2000-2025)" slug: yield-gap-sweden-backtest publish_date: 2026-03-24 tags: [backtests, sweden-markets, value-investing, earnings-yield, STO] post_access: public excerpt: "We ran the yield gap strategy on Stockholm Stock Exchange stocks from 2000 to 2025. The result: 10.61% CAGR vs 2.95% for OMX Stockholm 30 (+7.66% excess), with a 76% annual win rate against the local index." authors: [Swas] feature_image: 1_sweden_cumulative_growth.png feature_image_alt: "Growth of $10,000: Yield Gap Sweden vs OMX Stockholm 30 (2000-2025)"

Contents

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Sweden doesn't come to mind first when thinking about value investing. But among the markets we tested, Stockholm delivered strong excess returns over the local index, with a 76% annual win rate against the OMX Stockholm 30 and a return profile that compounded well across multiple market cycles.

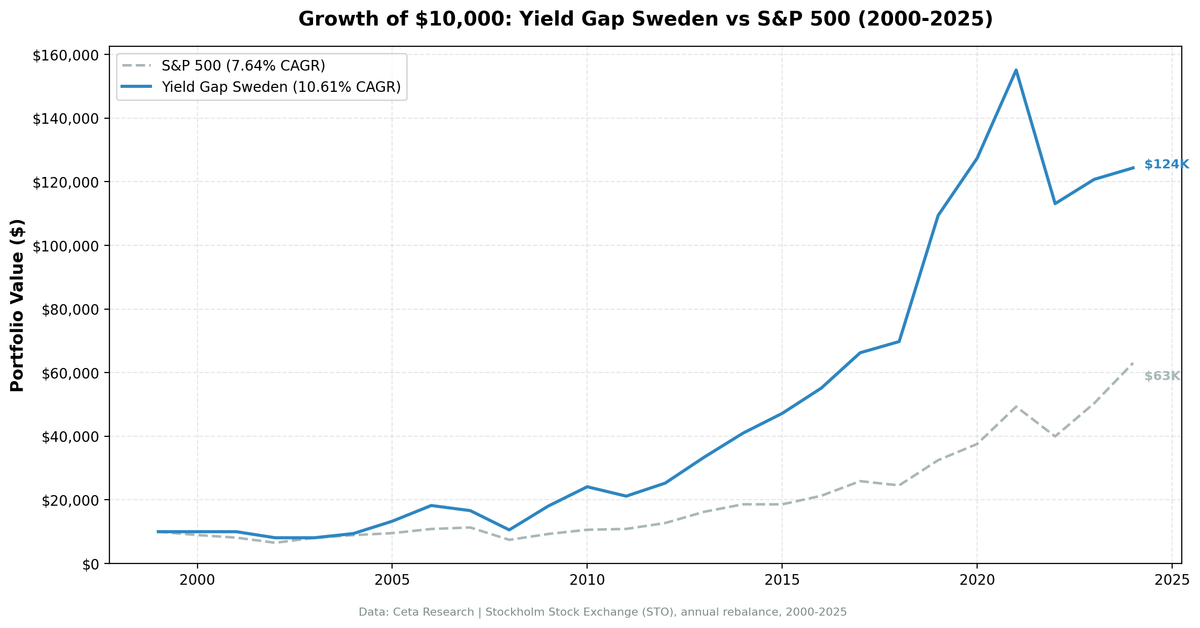

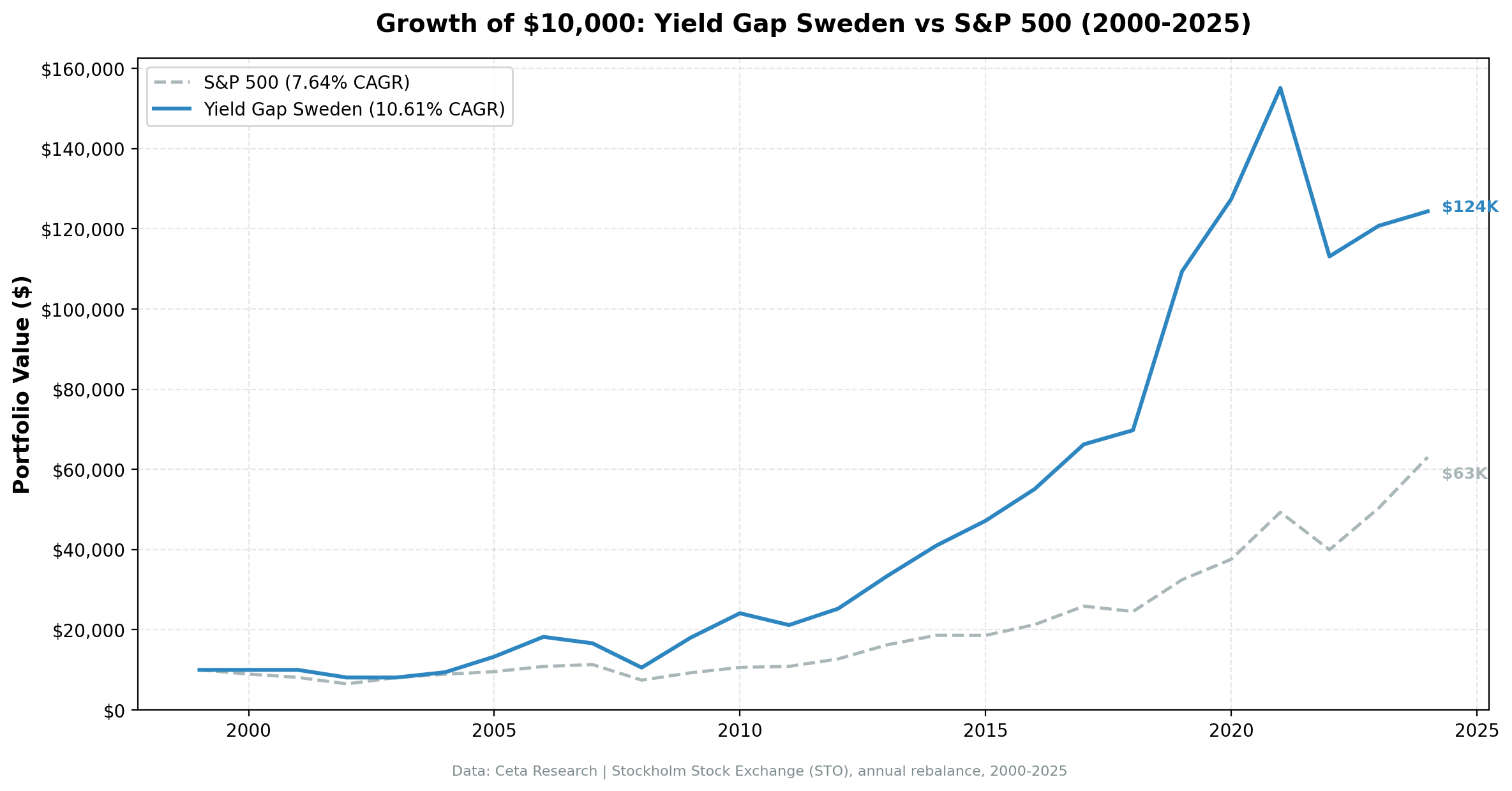

A $10,000 investment grew to $124,388 using this strategy. The OMX Stockholm 30 grew to about $20,700 over the same period. SPY grew to $63,066.

The Strategy

Sweden's risk-free rate over this period averaged roughly 2%, putting the effective threshold at 6% earnings yield (the 6% absolute floor applies, since rfr+3% = 5% is below the floor). PE ratios below ~16.7x.

Signal: - Earnings yield > 6% (PE < ~16.7x) - Earnings yield < 50% - ROE > 8% - D/E < 2.0

Portfolio construction: Top 30 by highest earnings yield, equal weight, annual January rebalance. Cash if fewer than 10 stocks qualify. Three years at the start of the backtest (2000, 2001, 2003) saw fewer than 10 qualifying stocks. The portfolio held cash for those years, which explains some of the early-period performance differences.

Methodology

- Universe: Stockholm Stock Exchange (STO)

- Market cap filter: SEK 2B+ at each rebalance date

- Data period: January 2000 through December 2025 (25 annual periods, 12% cash years — 3 of 25)

- Rebalancing: Annual (January)

- Point-in-time data: FY filings with 45-day filing lag

- Transaction costs: Size-tiered model

- Benchmark: OMX Stockholm 30 (local Swedish benchmark)

- Data source: Ceta Research FMP financial data warehouse

Full methodology at github.com/ceta-research/backtests/blob/main/METHODOLOGY.md.

Results

| Metric | Yield Gap Sweden | OMX Stockholm 30 |

|---|---|---|

| CAGR | 10.61% | 2.95% |

| Total return (25yr) | 1,143.9% | ~107% |

| Max drawdown | -42.06% | -38.16% |

| Sharpe ratio | 0.348 | — |

| Down capture vs OMX | 51.5% | — |

| Win rate vs OMX | 76.0% | — |

| Cash periods | 3 of 25 years (12%) | — |

| Avg stocks (invested) | 26.7 | — |

The 76% win rate means the strategy beat the local OMX Stockholm 30 in 17 of 22 invested years. That's an unusually consistent edge. The OMX Stockholm 30 was itself a weak index over this period, averaging 2.95% CAGR from 2000-2025. The context matters: Sweden's large-cap index underperformed dramatically while the yield gap screen kept compounding.

The 51.5% down-capture vs OMX means the strategy absorbed about half the local index's declines on average.

Annual returns (portfolio vs OMX Stockholm 30):

| Year | Portfolio | OMX 30 | Excess |

|---|---|---|---|

| 2000 | 0.00% (cash) | -14.04% | +14.04% |

| 2001 | 0.00% (cash) | -20.09% | +20.09% |

| 2002 | -19.10% | -38.16% | +19.06% |

| 2003 | 0.00% (cash) | +25.19% | -25.19% |

| 2004 | +16.28% | +16.03% | +0.26% |

| 2005 | +41.31% | +28.84% | +12.47% |

| 2006 | +37.15% | +20.84% | +16.32% |

| 2007 | -8.81% | -9.08% | +0.27% |

| 2008 | -36.46% | -34.45% | -2.01% |

| 2009 | +70.87% | +38.89% | +31.99% |

| 2010 | +33.66% | +22.14% | +11.53% |

| 2011 | -12.22% | -15.08% | +2.86% |

| 2012 | +19.34% | +13.06% | +6.28% |

| 2013 | +32.27% | +17.20% | +15.06% |

| 2014 | +22.68% | +10.53% | +12.15% |

| 2015 | +15.07% | -4.74% | +19.81% |

| 2016 | +16.78% | +9.50% | +7.28% |

| 2017 | +20.22% | +3.47% | +16.75% |

| 2018 | +5.31% | -11.01% | +16.32% |

| 2019 | +56.83% | +28.65% | +28.18% |

| 2020 | +16.44% | +4.80% | +11.63% |

| 2021 | +21.76% | +28.95% | -7.19% |

| 2022 | -27.08% | -15.07% | -12.01% |

| 2023 | +6.74% | +15.38% | -8.64% |

| 2024 | +3.00% | +4.76% | -1.75% |

Note: 2000, 2001, and 2003 show 0% returns. The portfolio held cash in those years because fewer than 10 stocks met the EY > 6% / ROE > 8% / D/E < 2 criteria. The STO universe took a few years to yield enough qualifying stocks.

What Drove the Returns

2005-2006 and 2009-2010 were transformative. Swedish industrials and consumer companies were genuinely cheap relative to earnings. The portfolio returned +41.31% in 2005 (vs OMX +28.84%) and +37.15% in 2006 (vs OMX +20.84%). The 2009 bounce of +70.87% vs OMX +38.89% added another enormous compounding step.

2019 stands out. +56.83% vs OMX +28.65% (+28.18% excess). Sweden had a broad population of high-earnings-yield industrial and specialty companies that rerated sharply that year. No single event explains it. A sustained mid-cap value recovery.

2018 showed defensive quality vs local index. +5.31% vs OMX -11.01% (+16.32% excess). The OMX Stockholm 30 fell hard while Swedish quality value stocks with simpler business models held up. The strategy's sector mix diverged meaningfully from the large-cap index.

2021-2024 was mixed. 2021 saw underperformance vs local (-7.19% excess), 2022 was the worst relative year (-12.01%), and 2023-2024 continued weak (-8.64%, -1.75%). The OMX Stockholm 30 in recent years has been driven by industrial heavyweights (Atlas Copco, Volvo) at elevated multiples. The yield gap screen, by construction, excluded them.

The cash years had mixed effects vs local. Holding cash in 2003 (when OMX returned +25.19%) was a -25pp miss. But 2000 (avoided -14.04%) and 2001 (avoided -20.09%) more than offset that. Net, cash years were a modest positive vs the index.

Run It Yourself

Full backtest:

git clone https://github.com/ceta-research/backtests.git

cd backtests

pip install -r requirements.txt

python3 yield-gap/backtest.py --preset sweden --output results.json --verbose

Limitations

Currency risk: Returns in SEK. SEK/USD has been volatile, particularly during the 2022-2023 period when SEK weakened substantially against USD. USD-based investors would have experienced lower returns.

Cash years create uncertainty: Three early years of cash holding mean the 25-year track record includes periods where the strategy simply wasn't active. The actual invested-period CAGR is higher than the headline number, but so is the realized sequence risk.

Small universe: STO has a smaller number of large-cap companies than US or UK markets. In some years, the portfolio held 20-25 stocks at maximum. Sector concentration is higher than in more liquid markets.

Sweden's economy is global: Swedish large-cap companies (engineering, industrials, financial) have heavy international revenue exposure. Returns are partly driven by global industrial cycle dynamics, not just Swedish domestic conditions.

Data: Ceta Research (FMP financial data warehouse), January 2000 through December 2025. Full methodology: github.com/ceta-research/backtests/blob/main/METHODOLOGY.md.

Academic references: Campbell, J.Y. & Vuolteenaho, T. (2004). "Bad Beta, Good Beta." American Economic Review, 94(5). Damodaran, A. (2012). "Equity Risk Premiums (ERP): Determinants, Estimation and Implications." Stern School of Business.

Past performance does not guarantee future results. This is educational content, not investment advice.