P/TBV Strategy in Canada: 25 Years, 0.77% Annual Edge, and an Honest

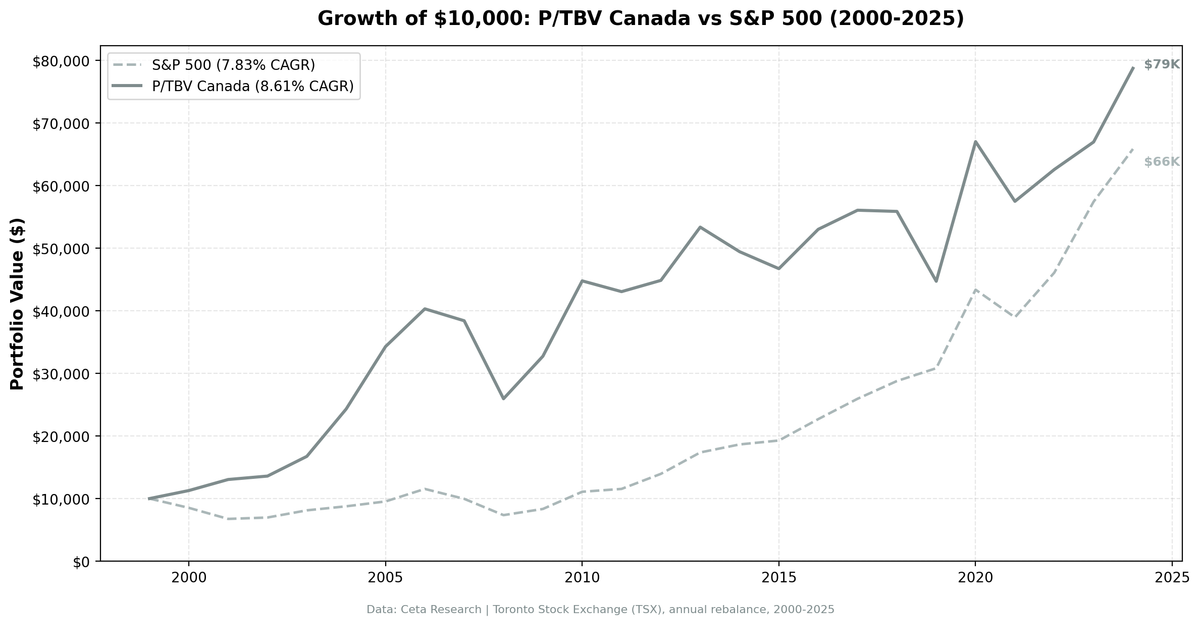

Over 25 years on the Toronto Stock Exchange, a Price-to-Tangible-Book strategy returned 8.61% annually against SPY's 7.83%, a margin of 0.77 percentage points. That's the narrowest outperformance of any market we publish a dedicated blog for. Canada works, barely, and understanding why it works helps explain where the strategy's limits are. This is an honest look at what 0.77% of annual edge actually means and what threatens it.

Contents

- What the Strategy Does

- The Numbers, Bluntly

- Annual Returns

- The Good Years

- The Oil Price Problem

- 2019: The Clearest Failure Year

- 2008: When the Strategy Broke Down

- What 0.77% Actually Means

- Why It Works Anyway

- Current Screen

- Limitations

What the Strategy Does

We screen TSX-listed companies for the lowest P/TBV ratios (market cap divided by tangible book, excluding goodwill and intangibles), apply quality filters of ROE > 8%, ROA > 3%, and operating margin > 10%, then hold the 30 cheapest qualifying stocks annually, rebalancing each July. Market cap floor: C$500M (roughly $362M USD). The strategy ran fully invested every year from 2000 through 2024, with no cash periods.

The Numbers, Bluntly

| Metric | Value |

|---|---|

| CAGR (2000-2024) | 8.61% |

| SPY CAGR | 7.83% |

| Excess return | +0.77% |

| Sharpe ratio | 0.305 |

| Max drawdown | -35.62% |

| Up capture | 90.52% |

| Down capture | 26.75% |

| Beta | 0.712 |

| Alpha | 2.31% |

| Invested periods | 25 of 25 years |

| Avg stocks held | 24.3 |

The Sharpe of 0.305 is below most of the exchanges we've tested. The up capture of 90.52% means Canada doesn't fully participate in SPY bull markets. On the other hand, down capture of 26.75% is exceptional: when SPY falls, Canada falls far less. Beta of 0.712 reflects real decoupling from US markets.

Annual Returns

| Year | Canada P/TBV | SPY | Difference |

|---|---|---|---|

| 2000 | +12.83% | -14.78% | +27.61% |

| 2001 | +15.66% | -20.77% | +36.43% |

| 2002 | +4.19% | +3.29% | +0.90% |

| 2003 | +23.16% | +16.44% | +6.72% |

| 2004 | +45.19% | +7.94% | +37.25% |

| 2005 | +41.02% | +8.86% | +32.16% |

| 2006 | +17.60% | +20.95% | -3.35% |

| 2007 | -4.72% | -13.71% | +8.99% |

| 2008 | -32.44% | -26.14% | -6.30% |

| 2009 | +26.16% | +13.42% | +12.74% |

| 2010 | +36.79% | +32.94% | +3.85% |

| 2011 | -3.84% | +4.10% | -7.94% |

| 2012 | +4.17% | +20.85% | -16.68% |

| 2013 | +18.97% | +24.50% | -5.53% |

| 2014 | -7.35% | +7.38% | -14.73% |

| 2015 | -5.49% | +3.36% | -8.85% |

| 2016 | +13.46% | +17.73% | -4.27% |

| 2017 | +5.75% | +14.34% | -8.59% |

| 2018 | -0.34% | +10.91% | -11.25% |

| 2019 | -19.97% | +7.12% | -27.09% |

| 2020 | +49.88% | +40.68% | +9.20% |

| 2021 | -14.23% | -10.17% | -4.06% |

| 2022 | +8.84% | +18.31% | -9.47% |

| 2023 | +7.03% | +24.60% | -17.57% |

| 2024 | +17.58% | +14.67% | +2.91% |

The Good Years

The early returns look spectacular. In 2000 and 2001, when the S&P 500 fell 14.78% and 20.77% respectively, Canadian P/TBV stocks returned +12.83% and +15.66%. The explanation isn't complicated: Canadian markets were less exposed to US tech and telecom stocks at the height of the dot-com bubble. The tangible book screen selected resource companies, banks, and industrials that kept generating earnings through the downturn.

2004 and 2005 were the commodity supercycle years. Canada's natural resource sector exploded as oil, metals, and agricultural commodities ran. Energy and materials companies passed the P/TBV screen because their physical assets, pipelines, refineries, mines, were genuinely cheap relative to market cap before the commodity boom repriced them. Returns of +45.19% and +41.02% reflect the strategy being positioned well for an exogenous macro shift.

2020 deserves attention: +49.88% vs SPY +40.68%. The COVID recovery lifted resource stocks hard. Energy equities that had been beaten down through 2019 bounced sharply.

The Oil Price Problem

2014 and 2015 are the years that expose Canada's structural weakness. The strategy returned -7.35% in 2014 and -5.49% in 2015 as oil prices collapsed.

Here's the mechanism. Energy companies with large tangible asset bases, pipelines, rigs, drilling equipment, refineries, appear cheap by P/TBV when commodity prices are high enough that those assets generate strong cash flows. When oil prices fall, the earnings case collapses, but the assets don't immediately disappear from the balance sheet. The P/TBV ratio stays low because book value is still there, but the quality filters (ROE, ROA) eventually catch up. The timing lag means you can hold energy companies through a brutal drawdown before the filters remove them at the next annual rebalance.

This is the commodity version of an asset value trap. The book value is real. The assets exist. But assets that generate poor returns at current commodity prices aren't worth their book value in any meaningful sense. P/TBV works better for industrials and financials where the asset return relationship is more stable.

2019: The Clearest Failure Year

The strategy lost 19.97% in 2019. SPY gained 7.12%. That's a 27-point gap in the wrong direction, the worst relative year in the dataset.

The 2019 story is US growth dominance. Large-cap US technology companies drove SPY returns, and the macro environment strongly favored expensive, asset-light businesses. Canadian low-P/TBV companies, many of them in energy and materials, were going the wrong direction. Oil hadn't recovered. Canadian banks were under pressure from a housing market that looked stretched. The quality filters kept the screen out of the worst companies, but when the sector composition skews toward resources, there's nowhere to hide from a commodity downturn in a growth-dominant year.

2008: When the Strategy Broke Down

We want to be direct about 2008. The strategy lost 32.44% while SPY fell 26.14%. That's worse performance during the financial crisis.

The reasons aren't hard to find. Canadian banks, which pass P/TBV screens on the basis of loan book assets, took significant losses as credit markets froze. Canadian energy companies fell with oil prices. The quality filters worked at the previous July rebalance, but the 12-month holding period meant companies that looked sound in mid-2007 were held through the worst of the crisis.

The down capture of 26.75% is a long-run average that looks good, but 2008 shows it's not uniformly protective. Individual crisis years can break the pattern.

What 0.77% Actually Means

A $100,000 investment at 8.61% CAGR over 25 years grows to approximately $768,000. The same amount at SPY's 7.83% grows to roughly $654,000. The difference is $114,000, more than the original investment, just from the 0.77% annual margin.

That's the case for running this strategy in Canada. The annual edge looks thin in any given year. Compounded over a quarter century, it's not trivial.

The years where Canada outperforms tend to be concentrated: 2000-2005, 2009-2010, 2020, 2024. The years where Canada underperforms also cluster: 2012-2013, 2016-2019, 2022-2023. This isn't a strategy that grinds out small edges every year. It's lumpy, and you need the discipline to hold through the underperformance stretches to capture the surplus when the cycle turns.

Why It Works Anyway

Canada's TSX has a natural asset intensity that suits P/TBV. Banks hold loan books as their primary assets. Energy companies hold wells and infrastructure. Industrials hold machinery. These aren't the businesses where stripping goodwill destroys the balance sheet.

The quality filters do meaningful work. Without ROE > 8%, the screen would pull in distressed energy companies and struggling miners. With the filters, it selects the cheapest among companies still earning their cost of capital. That's not the same as buying cheap junk.

The key risk: when commodity prices drive the return dispersion (as in 2014, 2015, 2019), the strategy's selection of tangible-asset companies biases it toward sectors that hurt during commodity downturns. There's no clean way to solve this without changing the strategy's fundamental character.

Current Screen

The live P/TBV screen for TSX-listed companies is available at cetaresearch.com/data-explorer. Filter by exchange TSX, apply the quality thresholds, and sort by P/TBV ascending to see current candidates.

Limitations

Currency: returns are in Canadian dollars. For USD investors, CAD/USD movements add variance not shown here.

The mktcap threshold of C$500M is relatively low. In thin sectors (2014-2015 energy bust), qualifying companies may still include companies under duress that pass quality filters at the last rebalance date before their deterioration shows up in reported financials.

Commodity sensitivity is structural, not a data artifact. If Canada's TSX composition shifts away from resources, the strategy's behavior will change.

Part of a Series: Global | US | UK | Sweden | India | Germany | China

Data: Ceta Research (FMP financial data warehouse), 2000-2024. Universe: Toronto Stock Exchange, mktcap > C$500M. Annual rebalance, July. Equal weight, top 30 by P/TBV ascending.