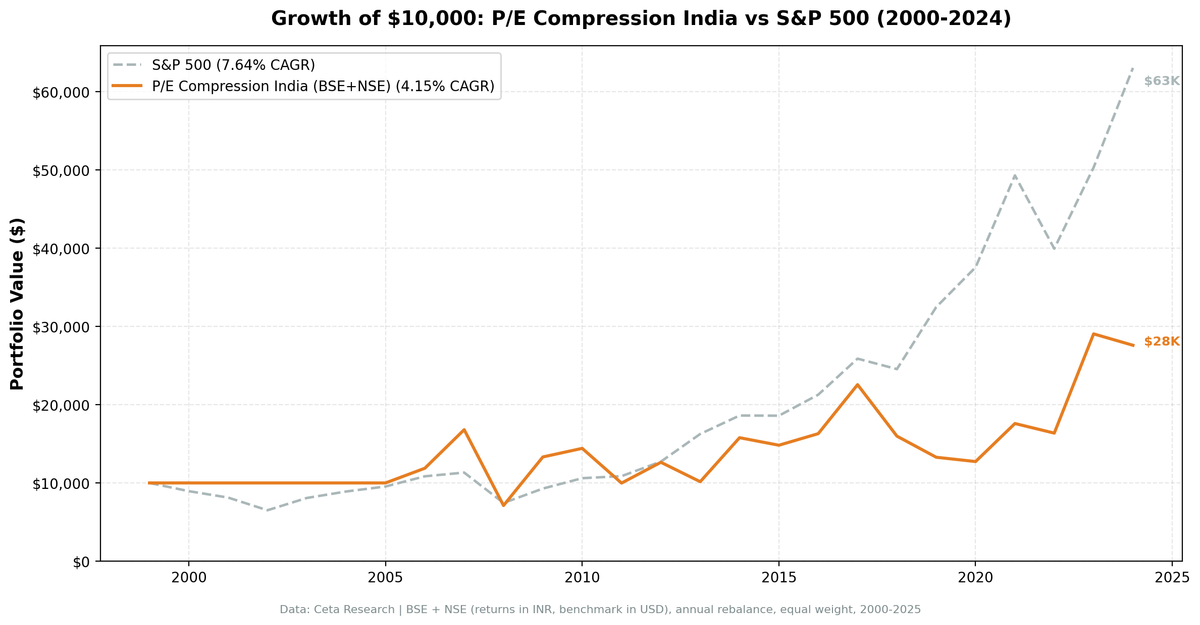

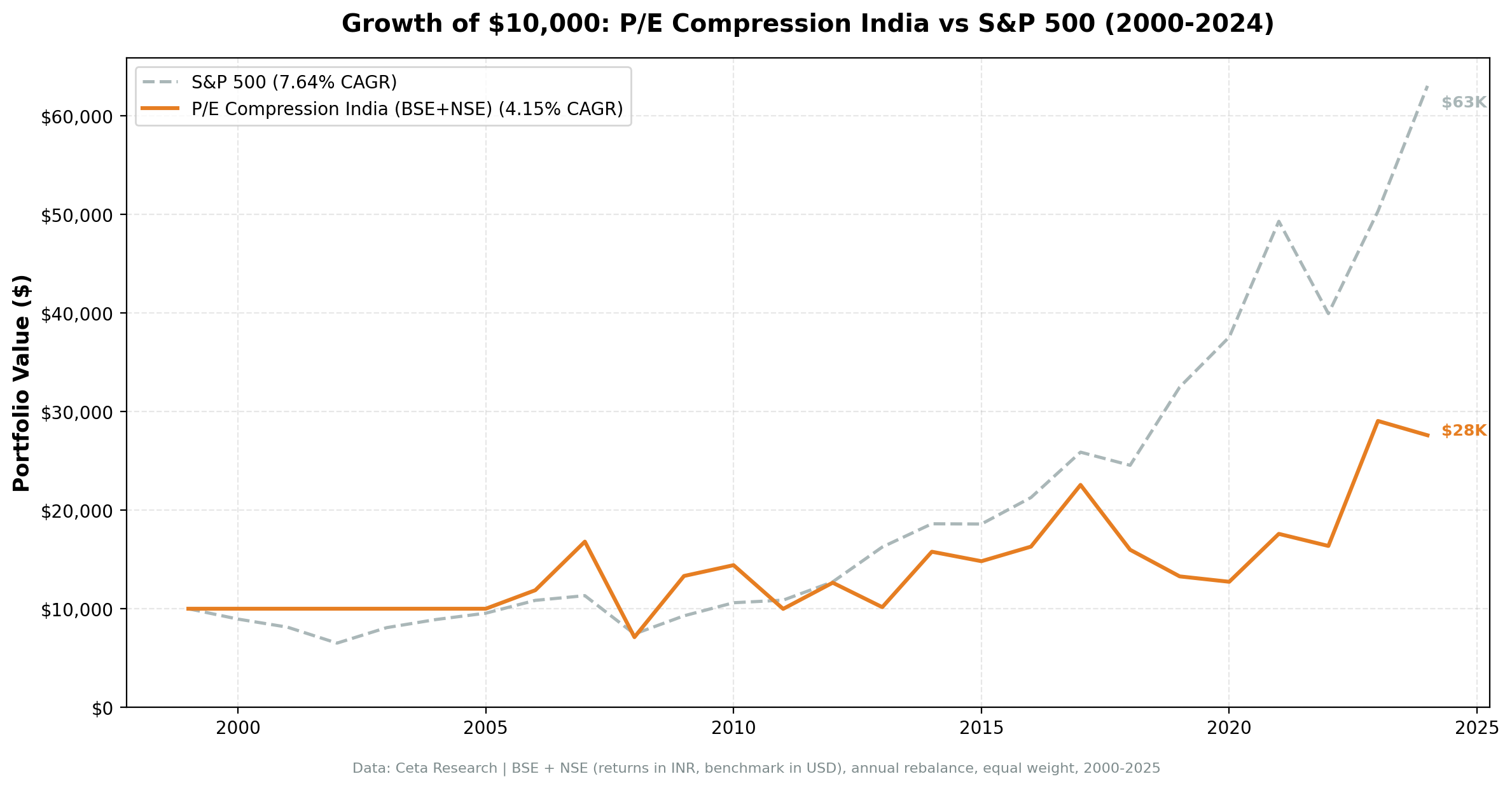

India P/E Compression: Negative Sharpe and 102% Down-Capture

P/E compression on Indian stocks underperforms SPY by 3.50% annually with a negative Sharpe ratio (-0.071) and 102% down-capture. The strategy amplified losses instead of protecting downside. When SPY lost 10%, this portfolio lost 10.2%. Extreme volatility makes P/E compression unreliable: compressed multiples are often justified by genuine earnings risk, not temporary sentiment.

Contents

Method

- Universe: BSE + NSE, market cap > ₹50B

- Period: 2000-2025 (25 years)

- Benchmark: S&P 500 Total Return (SPY, USD)

Returns in INR. Benchmark in USD.

What We Found

| Metric | India | S&P 500 |

|---|---|---|

| CAGR | 4.15% | 7.64% |

| Excess | -3.50% | - |

| Sharpe | -0.071 | 0.322 |

| MaxDD | -57.67% | -34.90% |

| Down-Cap | 101.78% | 100% |

| Avg Stocks | 24.3 | - |

| Cash | 6/25 (24%) | - |

Negative Sharpe ratio means the strategy delivered negative risk-adjusted returns. The -57.67% max drawdown is catastrophic. 102% down-capture means the strategy amplified SPY's losses.

Why India Fails

Extreme volatility. Indian markets swing violently. P/E ratios compress and expand based on earnings volatility, policy changes, and liquidity shocks, not just sentiment. Mean reversion assumes stability. India doesn't have it.

Earnings quality. Indian companies have less predictable earnings. A compressed P/E often reflects genuine concern about future profitability, not temporary undervaluation.

Liquidity and information gaps. Emerging market stocks trade on less complete information. P/E compression can persist for years if fundamentals don't improve.

Currency volatility. INR/USD movements add noise, but even in local-currency terms, the strategy underperforms.

Methodology

- Screen: P/E compression ratio below 0.85 (current P/E at least 15% below 5-year average)

- Quality filters: ROE above 10%, debt-to-equity below 2.0

- Rebalancing: Annual, equal-weight top 30 qualifying stocks

- Period: 25 years of out-of-sample data (2000-2025)

The 24% cash rate (6 of 25 years) is the second-highest across all tested markets. The strategy often couldn't find 30 qualifying stocks in India, reducing diversification and amplifying concentration risk.

Run It Yourself

Screen Indian stocks with P/E compression filters on Ceta Research. Market cap threshold: INR 50B, P/E compression ratio below 0.85, ROE above 10%, D/E below 2.0.

Part of a Series: US +2.32% | UK +1.38% | China -8.32% | Hong Kong -7.91%

Conclusion

India's P/E compression strategy fails badly: -3.50% underperformance, negative Sharpe, 102% down-capture. High volatility makes compressed multiples often justified, not temporary. The strategy doesn't work in extreme emerging markets.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research. Returns in INR. github.com/ceta-research/backtests