Earnings Surprise Drift on US Stocks: 170,000 Events, 26 Years

Earnings misses cause 8x more drift than beats on US stocks. We tested 170,115 earnings announcements from 2000 to 2025. Negative surprises produce -2.00% cumulative abnormal return at T+63. Positive surprises produce just +0.24%. The Post-Earnings Announcement Drift anomaly is real, but the edge is concentrated almost entirely on the short side.

Contents

- Method

- The Strategy

- What We Found

- Positive vs Negative Surprise Drift

- Quintile Analysis at T+63

- Beat Rate Trend

- When It Works and When It Struggles

- Run It Yourself

- Limitations

- Part of a Series

- References

Method

| Parameter | Details |

|---|---|

| Data source | FMP earnings_surprises + stock_eod (Ceta Research warehouse) |

| Universe | NYSE, NASDAQ, AMEX — market cap threshold applied per exchange |

| Period | 2000–2025 (26 years) |

| Events | 170,115 total (deduplicated per symbol/date) |

| Benchmark | Equal-weighted market return, same exchange |

| Surprise metric | (epsActual − epsEstimated) / ABS(epsEstimated) |

| Windows | T+1, T+5, T+21, T+63 trading days |

The Strategy

Post-Earnings Announcement Drift (PEAD) is one of the oldest documented market anomalies. The finding: stocks with large positive earnings surprises continue drifting up for weeks after the announcement. Stocks with large negative surprises continue drifting down.

Ball and Brown documented this in 1968. Bernard and Thomas replicated it in 1989 and showed the drift persists for up to 60 trading days. Foster, Olsen, and Shevlin extended the analysis in 1984. Despite decades of academic attention, the drift hasn't been fully arbitraged away.

The mechanism is behavioral. Markets underreact to earnings news on announcement day, then gradually incorporate the signal over the following weeks. This is especially pronounced for negative surprises, where investors appear reluctant to fully price in bad news immediately.

We stratified all events into quintiles by standardized surprise: Q1 is the worst 20% of misses, Q5 is the best 20% of beats.

What We Found

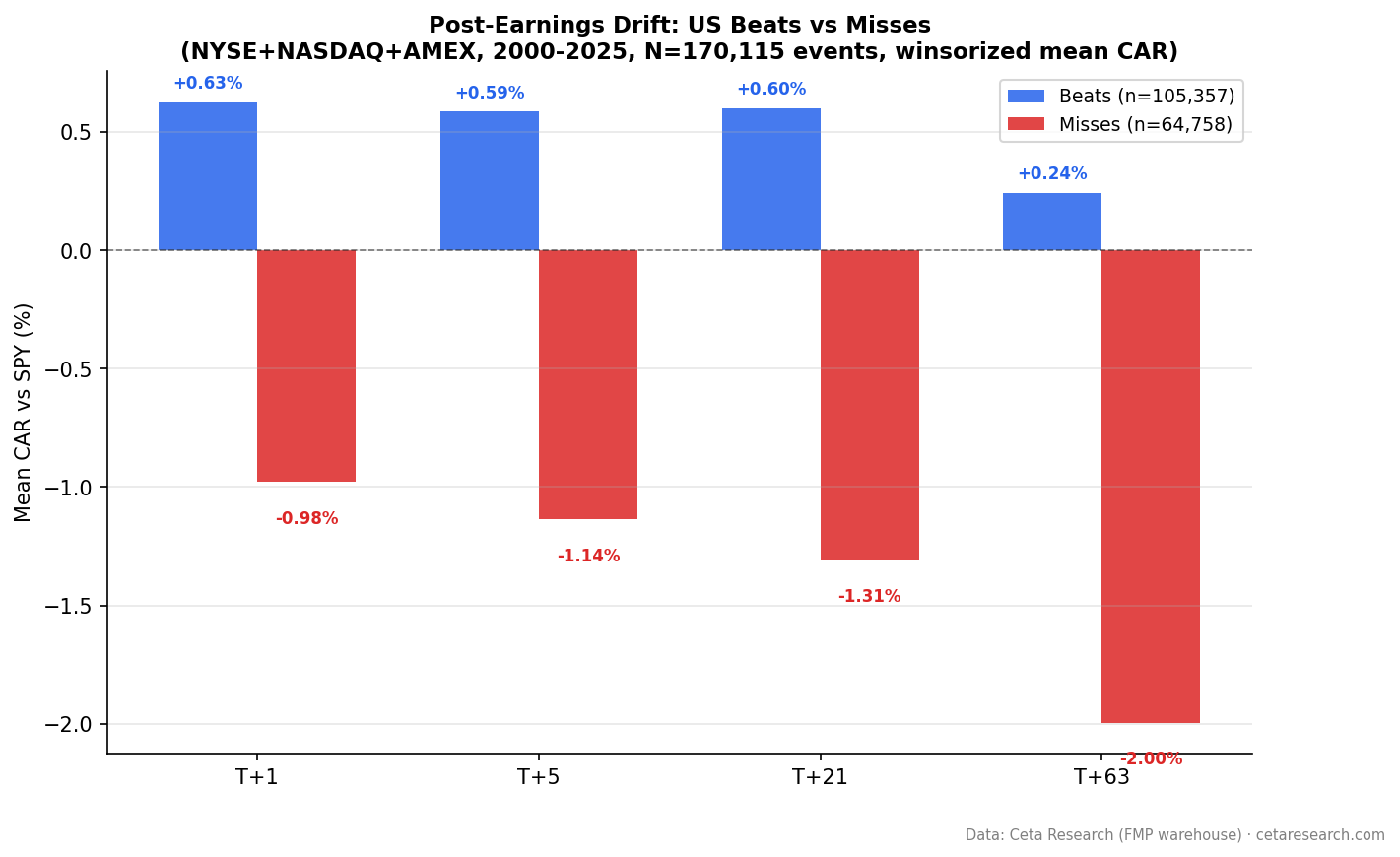

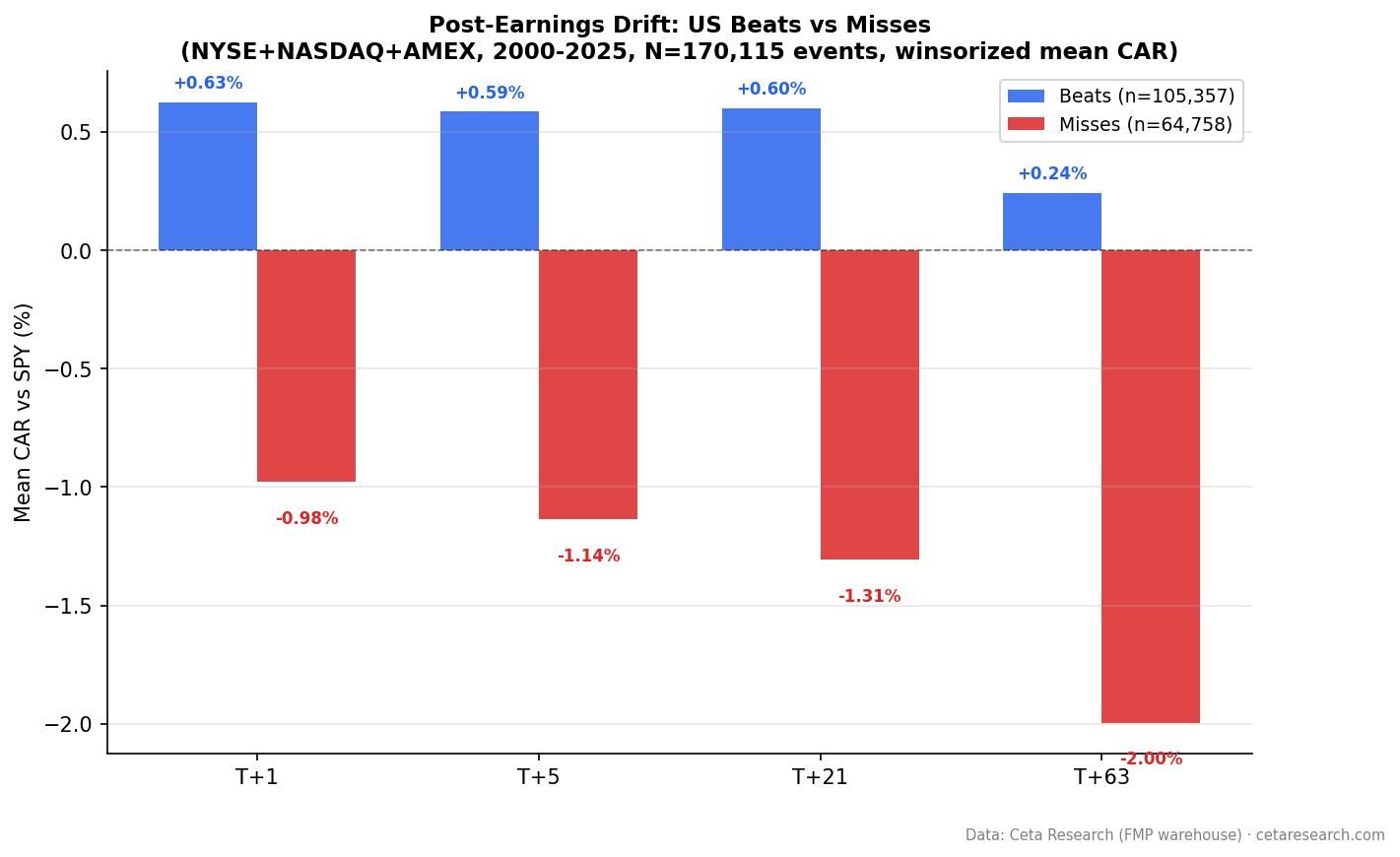

Positive vs Negative Surprise Drift

| Direction | Events | T+1 | T+5 | T+21 | T+63 |

|---|---|---|---|---|---|

| Positive surprises | 105,357 (61.9%) | +0.63% | +0.59% | +0.60% | +0.24% |

| Negative surprises | 64,758 (38.1%) | -0.98% | -1.14% | -1.31% | -2.00% |

The asymmetry is stark. Positive surprises drift up modestly early (+0.63% at T+1) then fade to near zero by T+63 (+0.24%). Negative surprises keep drifting down through the entire 63-day window, reaching -2.00%.

That's an 8:1 magnitude ratio at T+63. Misses hurt far more than beats help.

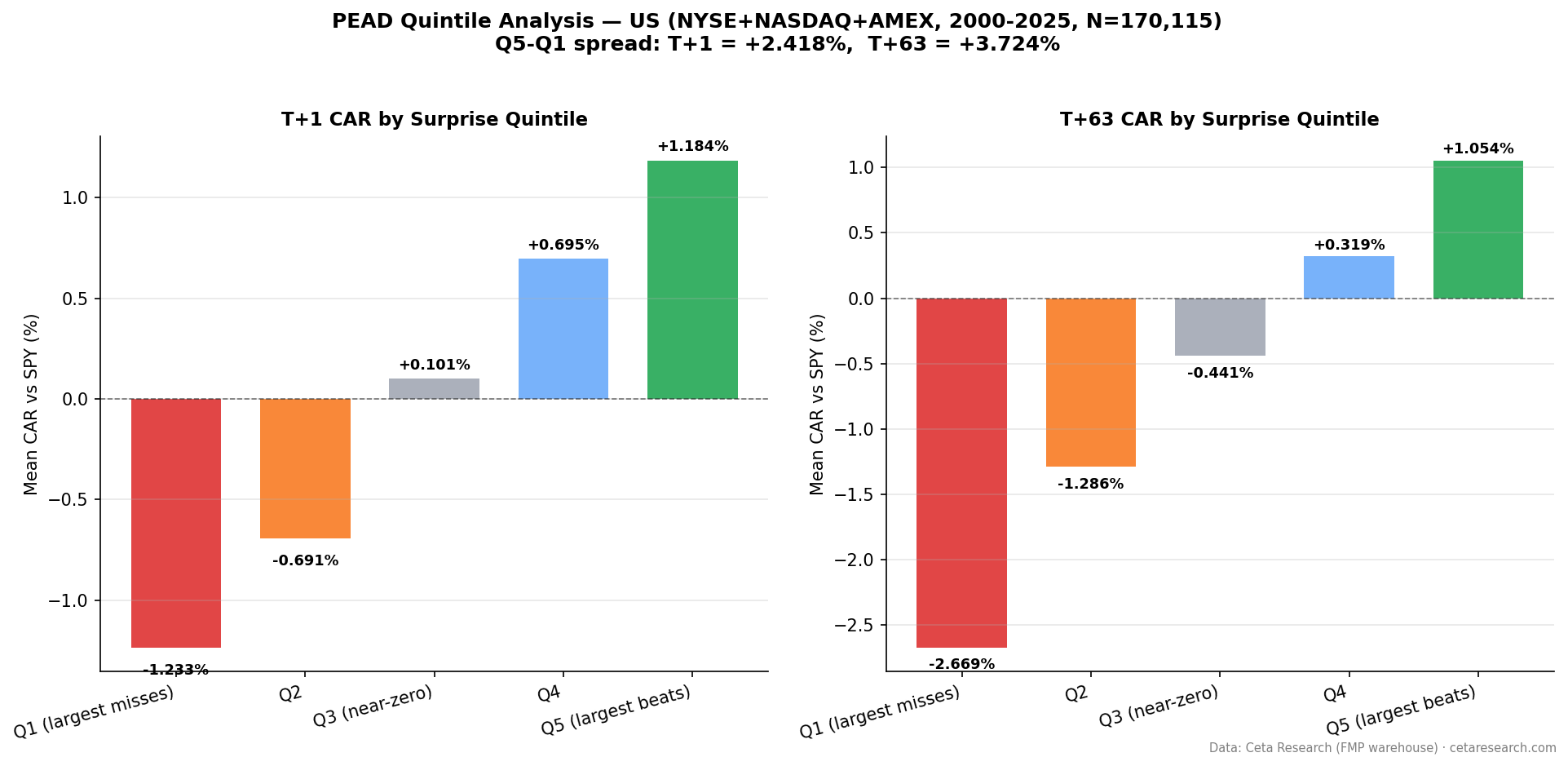

Quintile Analysis at T+63

| Quintile | Description | Events | CAR at T+63 |

|---|---|---|---|

| Q5 | Biggest beats | 34,029 | +1.05% |

| Q4 | Moderate beats | — | +0.32% |

| Q3 | Near-consensus | — | -0.44% |

| Q2 | Moderate misses | — | -1.29% |

| Q1 | Worst misses | 32,952 | -2.67% |

The Q5-Q1 spread is +3.72% at T+63. That's a meaningful edge, and again, it's driven more by the Q1 tail (-2.67%) than the Q5 tail (+1.05%).

Beat Rate Trend

The share of positive surprises has grown steadily. Around 2000, roughly 57% of US earnings came in above estimates. By 2006, that figure reached 62%. Post-2018, beat rates run 65–70%.

This reflects guidance conservatism. Companies have learned to set expectations low enough to beat reliably. The practical implication: a raw "positive surprise" is less informative today than it was in 2000. The magnitude of the beat matters more than the direction.

When It Works and When It Struggles

The drift is most pronounced in the days immediately after the announcement. The T+1 reaction captures initial underreaction. By T+21 to T+63, the negative surprise drift continues building while the positive surprise drift fades.

Negative PEAD tends to be stronger during risk-off environments. When market volatility is elevated, investors are slower to react to bad news. The drift gets longer and deeper.

Positive PEAD fades faster in trending bull markets. When sentiment is bullish, beats get priced in quickly. The drift window compresses.

Run It Yourself

Live screen using the Ceta Research data API:

-- Most recent earnings surprises with large positive standardized surprise

WITH deduped AS (

SELECT

es.symbol,

es.date,

es.epsActual,

es.epsEstimated,

(es.epsActual - es.epsEstimated) / NULLIF(ABS(es.epsEstimated), 0) AS std_surprise,

ROW_NUMBER() OVER (PARTITION BY es.symbol, es.date ORDER BY es.lastUpdated DESC) AS rn

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE p.exchange IN ('NYSE', 'NASDAQ', 'AMEX')

AND p.marketCap >= 500000000

AND p.isActivelyTrading = true

AND es.date >= CURRENT_DATE - INTERVAL '90 days'

AND ABS(es.epsEstimated) > 0.01

)

SELECT

symbol,

date,

epsActual,

epsEstimated,

ROUND(std_surprise * 100, 1) AS surprise_pct

FROM deduped

WHERE rn = 1

AND std_surprise > 0.10

ORDER BY date DESC, std_surprise DESC

LIMIT 50

Run this query on Ceta Research →

Limitations

PEAD event studies assume you can trade at or near the closing price on announcement day. In practice, many earnings come after hours, and the T+1 open reflects immediate price discovery. The T+1 CAR in this study uses closing prices, so real-world execution will capture a portion of that initial move, not all of it.

Transaction costs matter. At 170,000 events over 26 years, the average event generates only +0.24% positive drift at T+63. A long-only PEAD strategy on positive surprises would need to clear commissions and slippage on a thin edge. The short side is more actionable, -2.00% at T+63 provides more margin.

Quintile assignments depend on analyst consensus estimates. Estimate quality varies across stocks and time periods. Small-cap stocks with sparse coverage have noisier estimates, which affects quintile accuracy.

Part of a Series

- PEAD Across 14 Global Exchanges: The Drift Is Universal

- India Earnings Surprise Drift: Strongest PEAD Globally

References

- Ball, R. & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research.

- Bernard, V. & Thomas, J. (1989). Post-earnings-announcement drift: Delayed price response or risk premium? Journal of Accounting Research.

- Foster, G., Olsen, C. & Shevlin, T. (1984). Earnings releases, anomalies, and the behavior of security returns. The Accounting Review.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse