Post-Earnings Drift Across 14 Global Exchanges: PEAD Is Universal

We tested Post-Earnings Announcement Drift on 14 global exchanges using 300,000+ earnings events from 2000 to 2025. The main finding is simple: PEAD is universal. Every exchange in our study shows a positive Q5-Q1 quintile spread at T+63. India leads at +7.59%. Sweden trails at +0.91%. But the direction is consistent everywhere. Beat estimates, and stocks drift up. Miss them, and they drift down.

Contents

- Method

- The Strategy

- What We Found

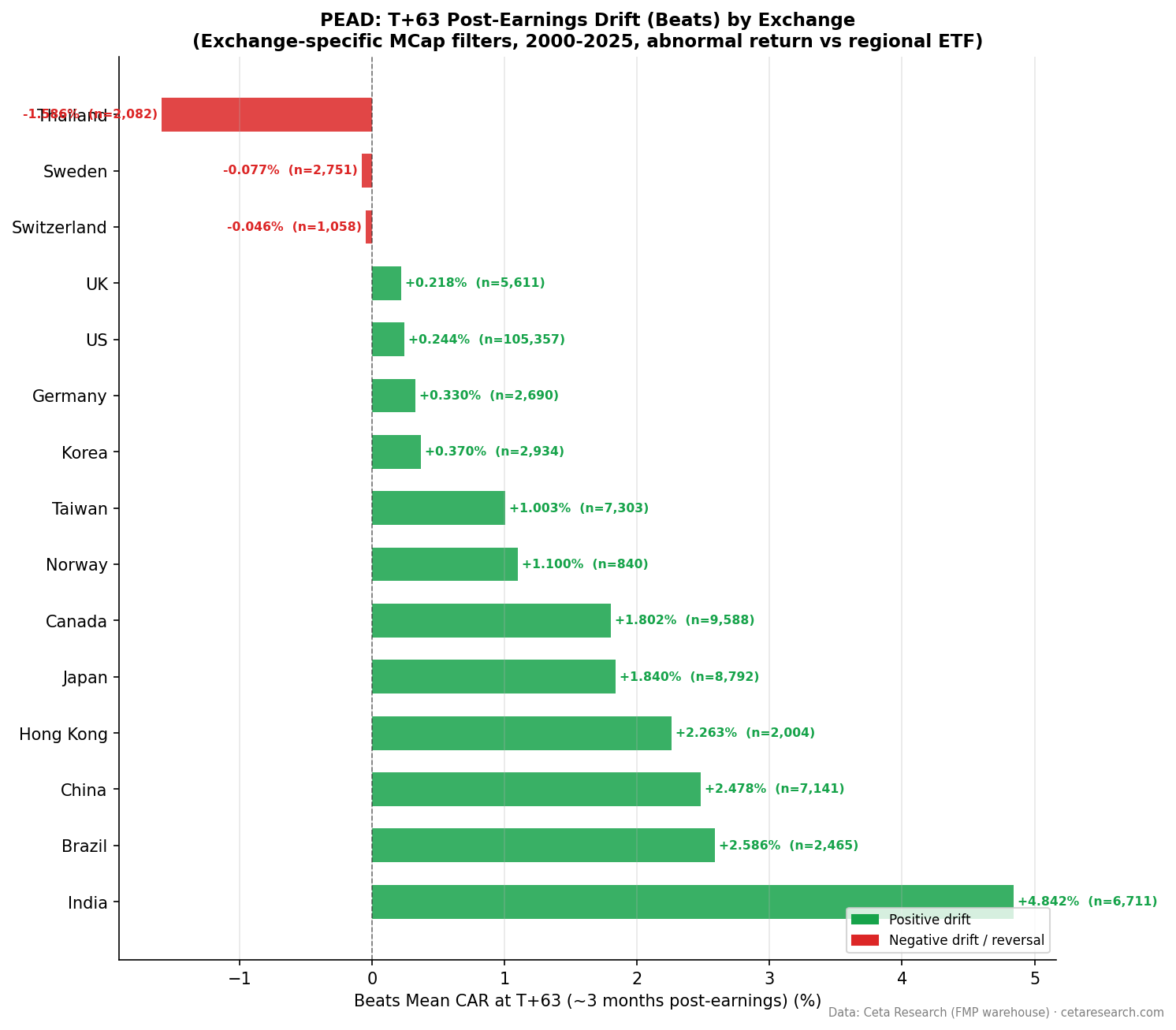

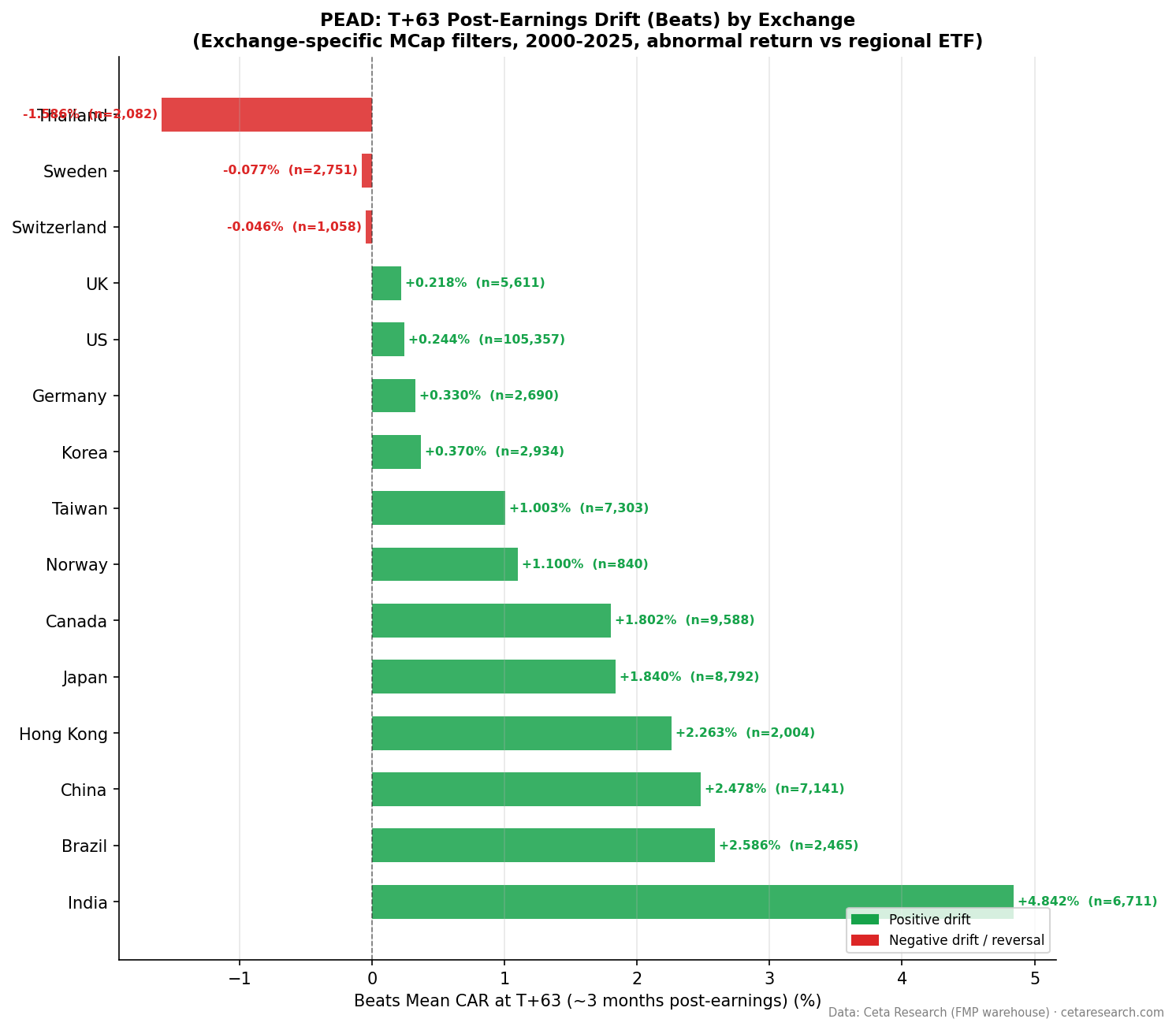

- Full Exchange Comparison (sorted by Q5-Q1 spread at T+63)

- Asian Markets Lead on Drift Magnitude

- Beat Rate Varies Widely

- Misses Hurt More Than Beats Help. In Most Markets

- When It Works and When It Struggles

- Run It Yourself

- Limitations

- Part of a Series

- References

Method

| Parameter | Details |

|---|---|

| Data source | FMP earnings_surprises + stock_eod (Ceta Research warehouse) |

| Universe | 14 exchanges — market cap threshold applied per exchange |

| Period | 2000–2025 (up to 26 years, varies by exchange) |

| Total events | 303,519 across all exchanges |

| Benchmark | Equal-weighted market return per exchange |

| Surprise metric | (epsActual − epsEstimated) / ABS(epsEstimated) |

| Quintile stratification | Q1 (worst misses) to Q5 (biggest beats) |

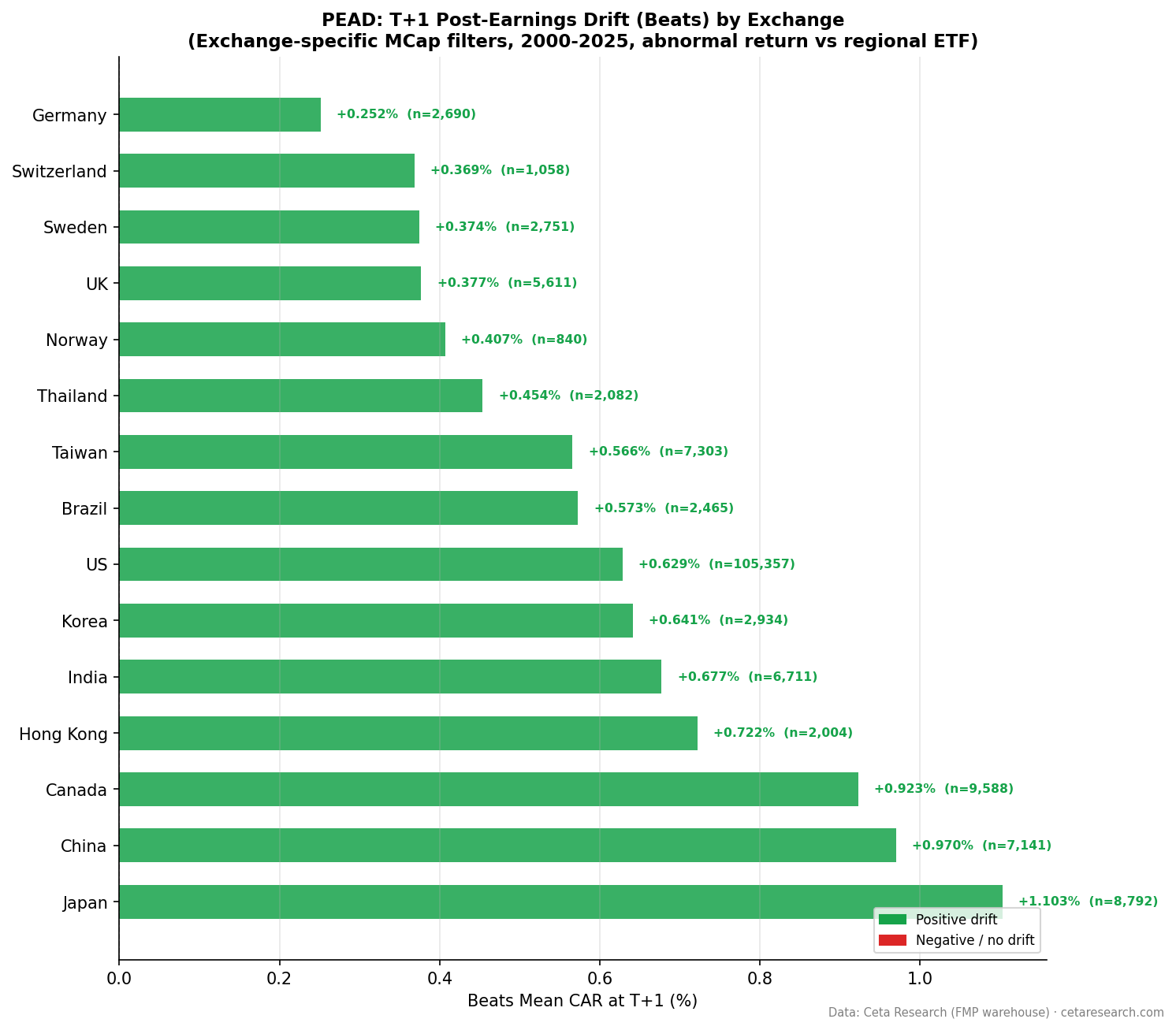

| Windows | T+1, T+5, T+21, T+63 trading days |

Note: XETRA (Germany) data in this warehouse is sparse before 2020, making it effectively a 5-year study (2020–2025). XETRA results should be treated as preliminary. Norway (OSL) was excluded from the main comparison due to a negative Q5-Q1 spread (-0.88%) on a small sample of 1,706 events.

The Strategy

PEAD is one of the most studied anomalies in academic finance. Ball and Brown (1968) first documented that earnings surprises predict post-announcement returns. Bernard and Thomas (1989) showed the drift persists for 60 trading days and challenged risk-based explanations for its persistence.

The standard interpretation is behavioral: markets underreact to earnings news on announcement day, then gradually reprice over weeks. The question we asked is whether this is a US-specific phenomenon or whether it generalizes globally.

Our global study covers 14 exchanges across North America, Europe, Asia, and Latin America. Each exchange is analyzed independently with its own benchmark return.

What We Found

Full Exchange Comparison (sorted by Q5-Q1 spread at T+63)

| Exchange | Events | Beat% | Pos T+63 | Neg T+63 | Q5-Q1 T+63 |

|---|---|---|---|---|---|

| BSE+NSE (India) | 14,360 | 46.7% | +4.84% | +0.08% | +7.59% |

| TAI+TWO (Taiwan) | 16,696 | 43.7% | +1.00% | -2.38% | +5.47% |

| SET (Thailand) | 4,540 | 45.9% | -1.59% | -5.11% | +5.43% |

| HKSE (Hong Kong) | 4,461 | 44.9% | +2.26% | -0.84% | +5.30% |

| JPX (Japan) | 15,352 | 57.3% | +1.84% | -1.56% | +5.01% |

| SHZ+SHH (China) | 20,667 | 34.6% | +2.48% | -0.08% | +4.76% |

| TSX (Canada) | 18,999 | 50.5% | +1.80% | -0.97% | +4.14% |

| LSE (UK) | 12,648 | 44.4% | +0.22% | -2.14% | +3.99% |

| XETRA (Germany)* | 5,851 | 46.0% | +0.33% | -2.09% | +3.91% |

| NYSE+NASDAQ+AMEX (US) | 170,115 | 61.9% | +0.24% | -2.00% | +3.72% |

| KSC (Korea) | 6,878 | 42.7% | +0.37% | -1.76% | +3.71% |

| SAO (Brazil) | 5,292 | 46.6% | +2.59% | -0.24% | +3.38% |

| SIX (Switzerland) | 2,077 | 50.9% | -0.05% | -1.85% | +2.57% |

| STO (Sweden) | 5,583 | 49.3% | -0.08% | -0.54% | +0.91% |

*XETRA data is sparse before 2020. Treat as a 5-year study only.

Asian Markets Lead on Drift Magnitude

The top 6 exchanges by Q5-Q1 spread are all in Asia: India, Taiwan, Thailand, Hong Kong, Japan, China. Western markets. US, UK, Germany, Switzerland, Sweden, cluster in the bottom half.

One interpretation: Asian markets are less efficient at incorporating earnings information, which creates a wider and longer drift window. Analyst coverage is thinner, institutional trading is less dominant in some markets, and retail participation is higher. All of these factors slow price discovery.

Beat Rate Varies Widely

| Beat rate | Exchanges |

|---|---|

| >57% | JPX (57.3%), NYSE+NASDAQ+AMEX (61.9%) |

| ~50% | TSX (50.5%), SIX (50.9%), STO (49.3%) |

| 43–47% | BSE+NSE, TAI+TWO, SET, HKSE, LSE, XETRA, SAO |

| <43% | KSC (42.7%), SHZ+SHH (34.6%) |

China's 34.6% beat rate stands out. More than 65% of Chinese earnings announcements miss estimates. This is structurally different from the US (61.9% beats), where guidance conservatism has pushed beat rates higher over time. China's low beat rate suggests analyst estimates are less prone to sandbagging.

Japan's 57.3% beat rate is the second highest, which mirrors the US in terms of guidance management maturity.

Misses Hurt More Than Beats Help. In Most Markets

In 9 of 14 exchanges, the absolute magnitude of negative surprise drift exceeds the magnitude of positive surprise drift. Thailand is the most extreme: Pos T+63 is -1.59% (slight negative drift even for beats) while Neg T+63 is -5.11%. The asymmetry there runs in the opposite direction of India.

India and China are the exceptions where negative surprises produce flat or near-zero drift. Both markets are largely long-only in practice, and this data supports a long-only PEAD approach there.

When It Works and When It Struggles

The T+1 reaction captures the immediate underreaction. The T+63 drift captures the continued repricing over the following quarter.

Markets with higher retail participation and lower institutional coverage tend to show stronger drift. The mechanism is slower price discovery, not stronger initial underreaction.

During market-wide stress (sharp drawdowns), PEAD drift tends to get noisier. Macro factors dominate single-stock earnings signals in those periods.

Run It Yourself

-- Global earnings surprise screen with exchange filter

WITH deduped AS (

SELECT

es.symbol,

es.date,

p.exchange,

es.epsActual,

es.epsEstimated,

(es.epsActual - es.epsEstimated) / NULLIF(ABS(es.epsEstimated), 0) AS std_surprise,

ROW_NUMBER() OVER (PARTITION BY es.symbol, es.date ORDER BY es.lastUpdated DESC) AS rn

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE p.isActivelyTrading = true

AND es.date >= CURRENT_DATE - INTERVAL '30 days'

AND ABS(es.epsEstimated) > 0.01

)

SELECT

symbol,

exchange,

date,

ROUND(std_surprise * 100, 1) AS surprise_pct,

epsActual,

epsEstimated

FROM deduped

WHERE rn = 1

AND std_surprise > 0.15

ORDER BY date DESC, std_surprise DESC

LIMIT 100

Run this query on Ceta Research →

Limitations

Exchange coverage varies by data depth. XETRA has meaningful data only from 2020 onward. OSL (Norway) was excluded due to its small sample and negative spread result. Results for thin-sample exchanges (SIX, SET, HKSE) carry wider confidence intervals than the larger exchanges (NYSE+NASDAQ+AMEX, SHZ+SHH, TSX).

Benchmark construction uses equal-weighted exchange returns. A market-cap-weighted benchmark would shift the absolute CAR numbers but shouldn't change relative rankings or the Q5-Q1 spread materially.

PEAD edge erodes as implementation capacity fills. The spreads here represent the gross anomaly, not a live trading strategy after costs.

Part of a Series

- Earnings Surprise Drift on US Stocks: 170,000 Events, 26 Years

- India Earnings Surprise Drift: Strongest PEAD Globally

References

- Ball, R. & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research.

- Bernard, V. & Thomas, J. (1989). Post-earnings-announcement drift: Delayed price response or risk premium? Journal of Accounting Research.

- Foster, G., Olsen, C. & Shevlin, T. (1984). Earnings releases, anomalies, and the behavior of security returns. The Accounting Review.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse