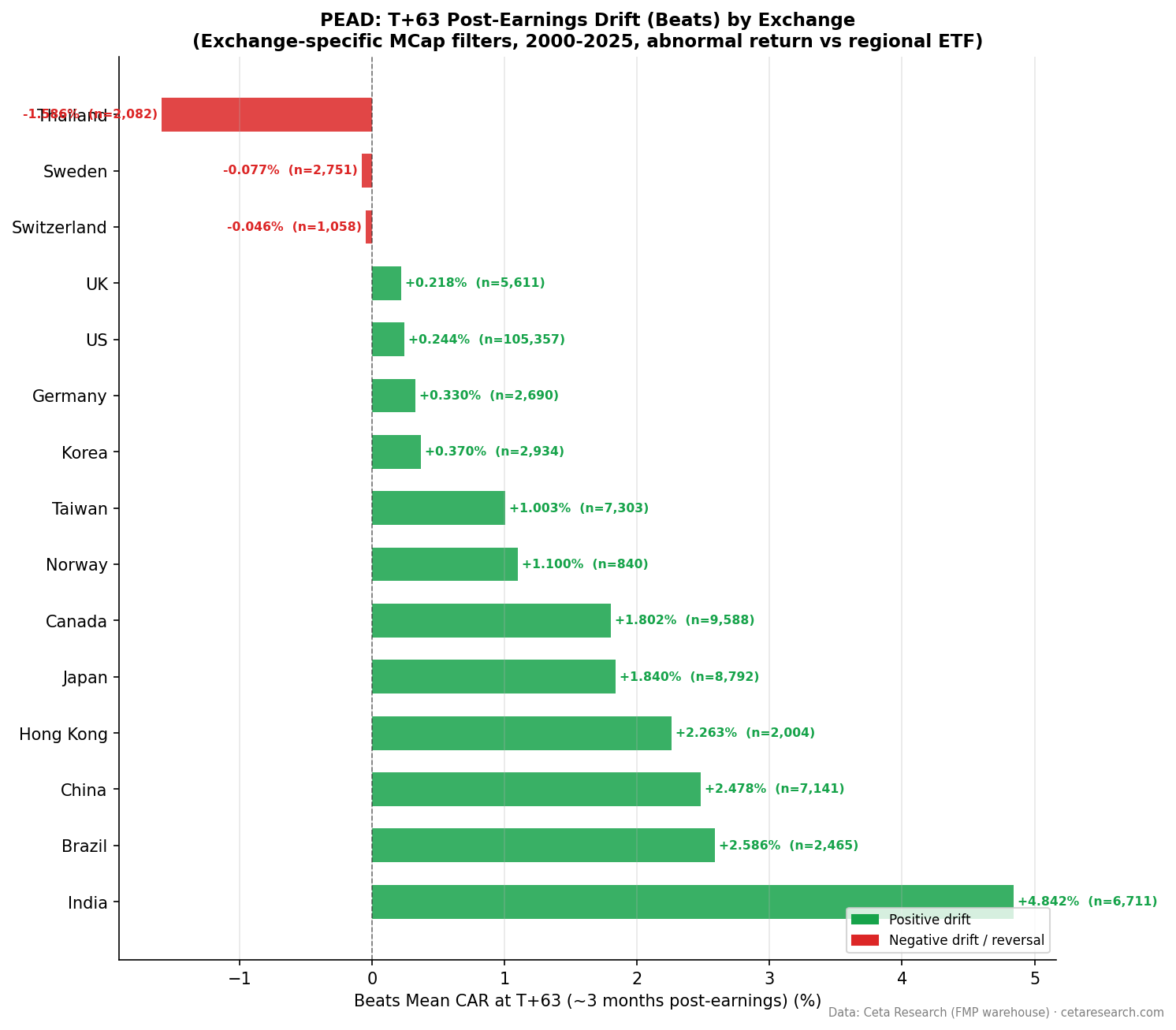

Earnings Surprise Drift in Japan: 15,000 Events, Strong PEAD Both Ways

Japan has the second-highest beat rate of any exchange we tested: 57.3% of earnings announcements come in above estimates. The drift is real in both directions. Biggest beats produce +3.02% cumulative abnormal return at T+63. Biggest misses fall -2.00%. The Q5-Q1 spread of +5.01% puts Japan among the stronger PEAD markets globally, and unlike some Asian exchanges, both sides of the drift contribute.

Contents

- Method

- The Strategy

- What We Found

- Positive vs Negative Surprise Drift

- Quintile Analysis at T+63

- Japan's Beat Rate Context

- When It Works and When It Struggles

- Run It Yourself

- Limitations

- Part of a Series

- References

Method

| Parameter | Details |

|---|---|

| Data source | FMP earnings_surprises + stock_eod (Ceta Research warehouse) |

| Universe | JPX — market cap threshold applied per exchange |

| Period | 2000–2025 (26 years) |

| Events | 15,352 total (deduplicated per symbol/date) |

| Benchmark | Equal-weighted JPX market return |

| Surprise metric | (epsActual − epsEstimated) / ABS(epsEstimated) |

| Windows | T+1, T+5, T+21, T+63 trading days |

The Strategy

Post-Earnings Announcement Drift (PEAD) is one of the most replicated anomalies in finance. Ball and Brown (1968) first documented that stocks continue drifting in the direction of their earnings surprise for weeks after announcement. Bernard and Thomas (1989) showed the effect persists for up to 60 trading days. Foster, Olsen, and Shevlin (1984) confirmed the pattern across different earnings windows.

The mechanism is behavioral: markets underreact to earnings news on announcement day, then gradually price in the information over the following weeks. We tested whether this holds for Japanese equities over a 26-year sample.

What We Found

Positive vs Negative Surprise Drift

| Direction | Events | Beat% | T+1 | T+5 | T+21 | T+63 |

|---|---|---|---|---|---|---|

| Positive surprises | 8,792 | 57.3% | +1.10% | +1.04% | +1.43% | +1.84% |

| Negative surprises | 6,560 | 42.7% | -1.52% | -1.76% | -1.63% | -1.56% |

Japan's PEAD is symmetric. Beats drift up consistently through all four windows. Misses drift down immediately and hold near that level through T+63. The T+1 gap on the negative side (-1.52%) is larger than the positive side (+1.10%), suggesting Japanese markets react sharply to bad news on the announcement day itself.

The drift on positive surprises builds gradually: +1.10% at T+1, then +1.84% by T+63. Negative surprises show their sharpest move early (-1.76% by T+5) then stabilize.

Quintile Analysis at T+63

| Quintile | Description | Events | CAR T+63 | t-stat | Hit Rate |

|---|---|---|---|---|---|

| Q5 | Biggest beats | 2,667 | +3.02% | +10.8 | 56.6% |

| Q4 | Moderate beats | — | +2.10% | — | — |

| Q3 | Near-consensus | — | -0.01% | — | — |

| Q2 | Moderate misses | — | -1.20% | — | — |

| Q1 | Worst misses | 2,645 | -2.00% | -7.2 | 42.3% |

The Q5-Q1 spread is +5.01% at T+63. Q5 has a t-stat of 10.8 and a 56.6% hit rate. Q1 has a t-stat of -7.2. Both sides are statistically robust. Q3 (near-consensus surprises) is essentially flat at -0.01%, confirming that the drift is concentrated in the tails.

Japan's PEAD is distinctive globally: the miss-side drift (-2.00% for Q1) is almost exactly as large as the beat-side drift (+3.02% for Q5). This bilateral structure contrasts with markets like India, where misses barely drift at all, or China, where the miss side is also weak.

Japan's Beat Rate Context

Japan's 57.3% beat rate is the second-highest globally after the US (61.9%). This matters because it suggests that Japanese analyst estimates are moderately conservative, though not as systematically so as in the US. The healthy volume of both beats and misses produces a well-balanced event distribution: 8,792 positive events vs 6,560 negative events.

The bilateral symmetry of Japan's drift creates an unusual opportunity. Unlike markets where only one side is actionable, Japan supports both a long-the-beat and short-the-miss approach.

When It Works and When It Struggles

The T+1 reaction on the negative side is particularly sharp (-1.52% on announcement day). This suggests Japanese markets price in bad news quickly on the announcement itself. The following drift through T+5 is additional.

Positive surprises take longer to be absorbed. The drift from T+1 to T+63 is steady (+1.10% to +1.84%), suggesting a longer window for capturing the beat-side signal compared to markets with faster information diffusion.

Japan's market structure may contribute to this pattern. Institutional ownership is high, but sell-side coverage is concentrated in large-cap names. Smaller and mid-cap stocks in the JPX universe have thinner analyst coverage, which can create wider initial mispricing when surprises occur.

Run It Yourself

python3 earnings-surprise/screen.py --preset japan

-- Recent large earnings surprises on JPX

WITH deduped AS (

SELECT

es.symbol,

es.date,

es.epsActual,

es.epsEstimated,

(es.epsActual - es.epsEstimated) / NULLIF(ABS(es.epsEstimated), 0) AS std_surprise,

ROW_NUMBER() OVER (PARTITION BY es.symbol, es.date ORDER BY es.lastUpdated DESC) AS rn

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE p.exchange = 'JPX'

AND p.isActivelyTrading = true

AND es.date >= CURRENT_DATE - INTERVAL '90 days'

AND ABS(es.epsEstimated) > 0.01

)

SELECT

symbol,

date,

epsActual,

epsEstimated,

ROUND(std_surprise * 100, 1) AS surprise_pct

FROM deduped

WHERE rn = 1

AND std_surprise > 0.10

ORDER BY date DESC, std_surprise DESC

LIMIT 50

Run this query on Ceta Research →

Limitations

15,352 events over 26 years is a solid sample. Coverage is thinner in the early 2000s, when fewer Japanese companies had systematic consensus estimates in our FMP warehouse. Results from 2000–2004 carry wider confidence intervals.

Japanese earnings calendars differ from Western norms. Many Japanese companies announce annual results in May, creating seasonality in event density. Quarterly reporting is less standardized than in the US, which means T+63 windows can span across subsequent earnings announcements for some companies.

Currency effects aren't controlled. The CAR computation uses JPY-denominated returns against a JPY benchmark, so FX doesn't introduce distortion within the study, but investors converting results to other currencies will face additional variance.

Part of a Series

- PEAD Across 14 Global Exchanges: The Drift Is Universal

- Earnings Surprise Drift on US Stocks: 170,000 Events, 26 Years

References

- Ball, R. & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research.

- Bernard, V. & Thomas, J. (1989). Post-earnings-announcement drift: Delayed price response or risk premium? Journal of Accounting Research.

- Foster, G., Olsen, C. & Shevlin, T. (1984). Earnings releases, anomalies, and the behavior of security returns. The Accounting Review.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse