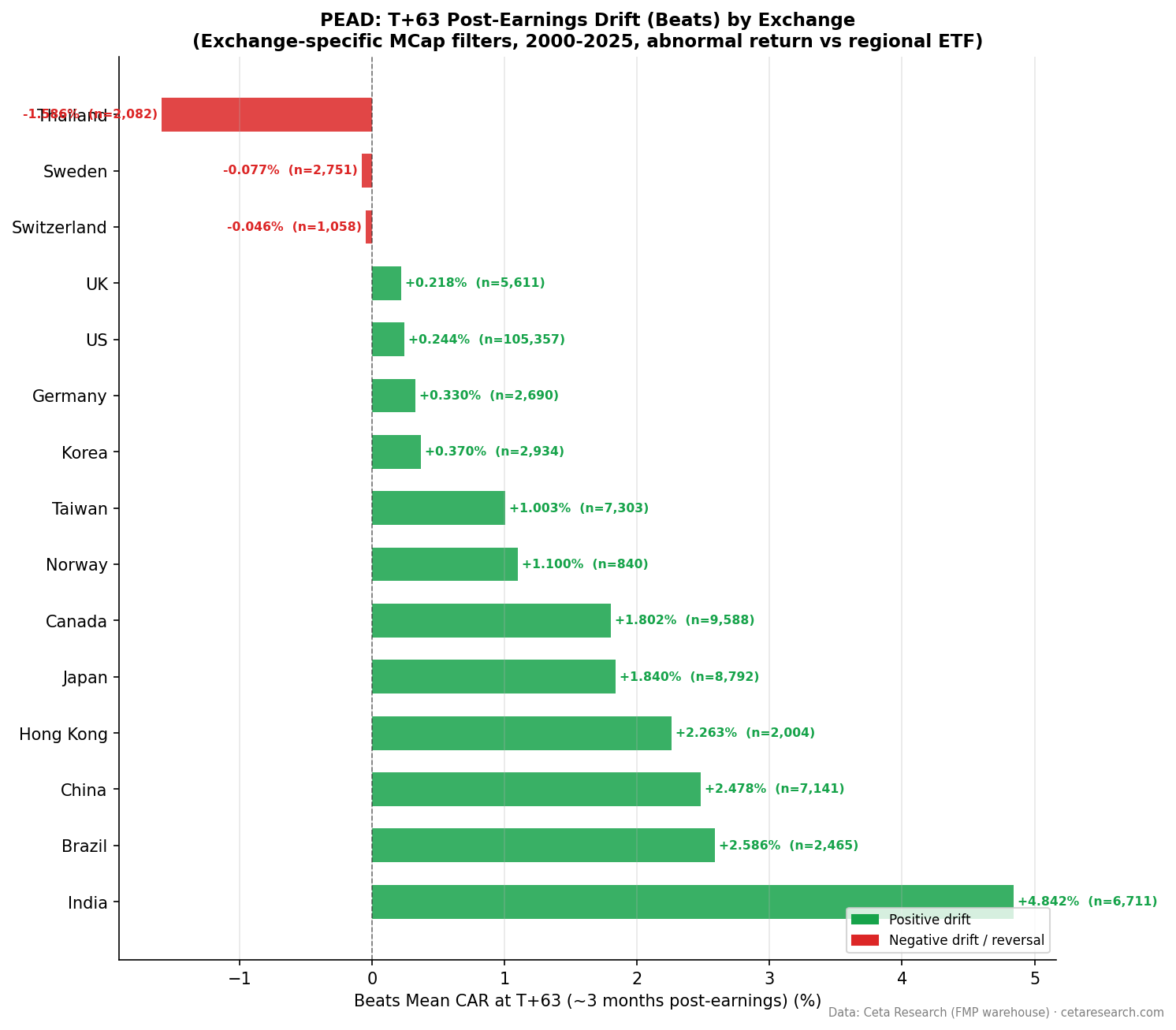

Earnings Surprise Drift in Canada: Symmetric PEAD on TSX, 26 Years

Canada's earnings surprise drift is clean, bilateral, and well-behaved. With a 50.5% beat rate, TSX earnings announcements split nearly evenly between beats and misses. Both sides drift in the expected direction. Biggest beats produce +2.27% cumulative abnormal return at T+63, biggest misses produce -1.87%. The Q5-Q1 spread of +4.14% is consistent and statistically significant on both tails.

Contents

- Method

- The Strategy

- What We Found

- Positive vs Negative Surprise Drift

- Quintile Analysis at T+63

- Canada vs the US

- When It Works and When It Struggles

- Run It Yourself

- Limitations

- Part of a Series

- References

Method

| Parameter | Details |

|---|---|

| Data source | FMP earnings_surprises + stock_eod (Ceta Research warehouse) |

| Universe | TSX — market cap threshold applied per exchange |

| Period | 2000–2025 (26 years) |

| Events | 18,999 total (deduplicated per symbol/date) |

| Benchmark | Equal-weighted TSX market return |

| Surprise metric | (epsActual − epsEstimated) / ABS(epsEstimated) |

| Windows | T+1, T+5, T+21, T+63 trading days |

The Strategy

Post-Earnings Announcement Drift (PEAD) is a documented market anomaly. Ball and Brown (1968) showed stocks continue moving in the direction of their earnings surprise for weeks after announcement. Bernard and Thomas (1989) confirmed the drift persists for up to 60 trading days. Foster, Olsen, and Shevlin (1984) extended the analysis across different earnings contexts.

The underlying mechanism is behavioral: markets underreact to earnings news at announcement, then gradually price in the information. Canada provides a useful test for this in a developed, mid-sized market with meaningful commodity exposure (energy, mining) alongside financial and tech sectors.

What We Found

Positive vs Negative Surprise Drift

| Direction | Events | Beat% | T+1 | T+5 | T+21 | T+63 |

|---|---|---|---|---|---|---|

| Positive surprises | 9,588 | 50.5% | +0.92% | +1.18% | +1.39% | +1.80% |

| Negative surprises | 9,411 | 49.5% | -0.65% | -1.00% | -0.98% | -0.97% |

Canada's PEAD is genuinely bilateral. Positive surprises build steadily from T+1 to T+63. Negative surprises show their sharpest move by T+5 (-1.00%) and then stabilize near -0.97% at T+63.

The near-equal event count (9,588 beats vs 9,411 misses) reflects a 50.5% beat rate that's far below the US (61.9%) and Japan (57.3%). Canadian analyst estimates aren't systematically conservative. You don't get the routine low-bar beats that inflate US beat rates. This produces a more balanced and arguably more informative surprise signal.

Quintile Analysis at T+63

| Quintile | Description | Events | CAR T+63 | t-stat | Hit Rate |

|---|---|---|---|---|---|

| Q5 | Biggest beats | 3,670 | +2.27% | +7.2 | 54.2% |

| Q4 | Moderate beats | — | +1.89% | — | — |

| Q3 | Near-consensus | — | +1.03% | — | — |

| Q2 | Moderate misses | — | -0.89% | — | — |

| Q1 | Worst misses | 3,735 | -1.87% | -5.6 | 42.4% |

The Q5-Q1 spread is +4.14% at T+63. Both Q5 (t=7.2) and Q1 (t=-5.6) are statistically significant. The hit rate for Q5 at 54.2% confirms the signal isn't driven by a few extreme outliers.

One detail worth noting: Q3 (near-consensus) produces +1.03% at T+63. This positive drift even for moderate surprises suggests a general tailwind to TSX equities in the sample period, or that the equal-weighted benchmark underperforms the event sample on average. The spread between Q5 and Q1 is the cleaner metric for the anomaly.

Q4 beats (+1.89%) nearly match Q5 (+2.27%) in magnitude, suggesting strong persistence in the upper portion of the distribution. You don't need the extreme top-quintile beat to capture meaningful drift in Canada.

Canada vs the US

The US beat rate of 61.9% inflates the positive event pool with routine conservative-guidance beats. Canada's 50.5% rate means positive surprises are genuine. The comparison shows:

| Metric | Canada | US |

|---|---|---|

| Beat rate | 50.5% | 61.9% |

| Q5 CAR T+63 | +2.27% | +1.05% |

| Q1 CAR T+63 | -1.87% | -2.67% |

| Q5-Q1 spread | +4.14% | +3.72% |

Canada's Q5 drift (+2.27%) is more than double the US Q5 (+1.05%). The miss side is shallower in Canada (-1.87% vs -2.67%). Overall the Canadian spread is wider, partly because the positive side works better.

When It Works and When It Struggles

Positive PEAD in Canada builds gradually, with each window incrementally larger than the last (T+1: +0.92%, T+5: +1.18%, T+21: +1.39%, T+63: +1.80%). The signal doesn't front-load. This gives more time to enter after the initial announcement.

Negative PEAD stabilizes quickly. The sharpest move is at T+5 (-1.00%), and the drift barely changes from there to T+63 (-0.97%). Short-side strategies in Canada capture most of their return within the first week.

Canada's commodity-heavy sectors (energy, mining) introduce event-specific volatility. A negative earnings surprise for an oil company during a commodity price decline carries different information content than a tech company miss. The quintile analysis aggregates across all sectors, so sector-specific implementation will see different magnitudes.

Run It Yourself

python3 earnings-surprise/screen.py --preset canada

-- Recent large earnings surprises on TSX

WITH deduped AS (

SELECT

es.symbol,

es.date,

es.epsActual,

es.epsEstimated,

(es.epsActual - es.epsEstimated) / NULLIF(ABS(es.epsEstimated), 0) AS std_surprise,

ROW_NUMBER() OVER (PARTITION BY es.symbol, es.date ORDER BY es.lastUpdated DESC) AS rn

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE p.exchange = 'TSX'

AND p.isActivelyTrading = true

AND es.date >= CURRENT_DATE - INTERVAL '90 days'

AND ABS(es.epsEstimated) > 0.01

)

SELECT

symbol,

date,

epsActual,

epsEstimated,

ROUND(std_surprise * 100, 1) AS surprise_pct

FROM deduped

WHERE rn = 1

AND ABS(std_surprise) > 0.10

ORDER BY date DESC, std_surprise DESC

LIMIT 50

Run this query on Ceta Research →

Limitations

18,999 events provides solid statistical power. The sample is well-distributed across the 26-year period, with TSX having consistent analyst coverage from the early 2000s onward.

Canada's resource sector introduces sector concentration in the event pool. Energy and mining companies represent a higher share of TSX events than they would in the US or Europe. Commodity price cycles affect earnings predictability in these sectors, which may create periods where analyst estimates are systematically off in one direction.

The market cap threshold excludes many small-cap TSX Venture Exchange listings. The results reflect the main TSX universe rather than the full Canadian equity market, which is appropriate for tradeable strategies but limits generalization to micro-caps.

Part of a Series

- PEAD Across 14 Global Exchanges: The Drift Is Universal

- Earnings Surprise Drift on US Stocks: 170,000 Events, 26 Years

References

- Ball, R. & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research.

- Bernard, V. & Thomas, J. (1989). Post-earnings-announcement drift: Delayed price response or risk premium? Journal of Accounting Research.

- Foster, G., Olsen, C. & Shevlin, T. (1984). Earnings releases, anomalies, and the behavior of security returns. The Accounting Review.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse