Canada's Best Deleveraging Result Is a Risk Story, Not a Return Story

The TSX produces the best risk-adjusted result of any exchange we tested. Sharpe 0.383. Down capture 48.75%. Max drawdown -42.51%, lower than SPY's -45.53% over the same period.

Contents

- The Strategy

- Results

- Why Resource Economies Reward Deleveraging

- The Strong Periods

- The Weak Stretch: 2012-2021

- The Down Capture Story

- Full Annual Returns

- Run This Screen

- Limitations

- Takeaway

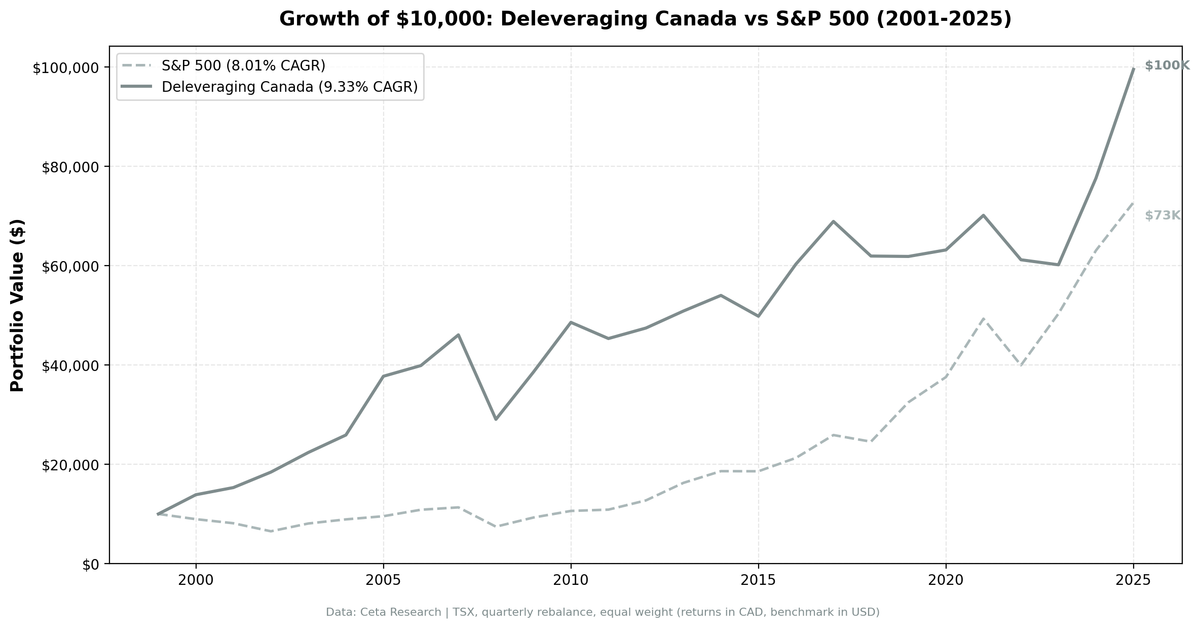

The headline return of 9.33% CAGR vs SPY's 8.01% barely registers as outperformance. But a portfolio that earns +1.32% more per year than the market while falling only half as much when markets drop isn't a modest result. It's a different kind of result.

Part of the Deleveraging series. US flagship blog

Returns are in CAD. SPY is in USD.

The Strategy

We screen TSX-listed stocks quarterly for companies meeting two conditions:

- Debt-to-equity ratio declined at least 10% year-over-year (annual filing data, 45-day lag)

- Return on equity above 8%

From that filtered universe, we hold the top 30 stocks ranked by magnitude of D/E reduction. Equal-weight, quarterly rebalance.

The ROE filter does the heavy lifting. Without it, the signal catches distressed companies shedding debt because their lenders are demanding it. With it, the screen targets profitable businesses that are voluntarily reducing leverage while generating returns for shareholders.

Methodology

| Parameter | Value |

|---|---|

| Universe | TSX (Canada) |

| Signal | D/E reduction ≥ 10% YoY + ROE > 8% |

| Prior D/E | > 0.1 (excludes near-zero leverage) |

| Market cap | > C$500M |

| Selection | Top 30 by D/E reduction magnitude |

| Weighting | Equal weight |

| Rebalance | Quarterly |

| Filing lag | 45 days (annual data) |

| Period | Q1 2000 - Q4 2025 |

| Returns currency | CAD |

Results

The strategy was always invested. Zero cash periods across 103 quarters. The +1.32% excess return and 48.75% down capture are uninterrupted 25-year numbers.

Key Performance Metrics

| Metric | Deleveraging (Canada) | SPY |

|---|---|---|

| CAGR | 9.33% | 8.01% |

| Excess vs SPY | +1.32% | — |

| Total Return | 895.39% | 627.45% |

| $10K → | $99,500 | $73,000 |

| Max Drawdown | -42.51% | -45.53% |

| Sharpe Ratio | 0.383 | — |

| Volatility | 17.85% | — |

| Up Capture | 81.24% | 100% |

| Down Capture | 48.75% | 100% |

| Beta | 0.742 | 1.00 |

| Alpha | 2.75% | — |

| Win Rate vs SPY | 50.49% | — |

| Avg Stocks Held | 24.7 | — |

| Cash Periods | 0 of 103 | — |

Two numbers stand out. Down capture of 48.75% means when the market falls, this portfolio historically falls about half as much. Max drawdown of -42.51% is lower than SPY's -45.53%, which is unusual for a concentrated 25-stock screen. Most active strategies have higher drawdowns than the index, not lower.

The $10K → $99.5K vs $73K comparison tells the compounding story. The strategy doesn't produce dramatic annual spreads. It compounds steadily with lower volatility, and over 25 years that adds up to $26K more per $10K invested.

Why Resource Economies Reward Deleveraging

Canada's TSX is nothing like the S&P 500. Energy, materials, and industrials dominate the index. These are sectors where cash flows are cyclical, leverage is structural, and companies that actively reduce debt during good years are genuinely different from those that don't.

A technology company deleveraging on the S&P 500 might be doing so for many reasons, some of which reflect genuine quality and some of which reflect quiet deterioration. The signal is noisy. In an efficient market with deep analyst coverage, that noise gets priced quickly, often before you can act on it.

A Canadian oil sands or mining company paying down 15% of its debt during a commodity upcycle while generating 12% ROE is a cleaner signal. The company has real cash flows, real capital discipline, and less institutional coverage chasing the same data. The TSX's mid-cap energy and materials universe doesn't attract the same density of analysts, hedge fund models, and algorithmic pricing that US markets do. The signal has more room to work.

The sector composition also creates a natural asymmetry around commodity cycles. When global commodity prices rise, Canadian resource companies generate outsized cash flows. The deleveraging signal captures those that are using that cash to strengthen their balance sheets rather than increase dividends or repurchase shares. That subset has historically had better outcomes in the next downturn.

That structural logic explains the three periods where the strategy did its best work.

The Strong Periods

2000-2002: Dotcom crash, +49%, +20%, +40% excess

Three consecutive years of large outperformance. The dotcom crash destroyed US technology companies with thin margins, speculative balance sheets, and no path to profitability. Canada's TSX, heavy in energy and materials, wasn't the same market. Companies in oil sands, diversified mining, and Canadian industrials were using commodity revenues to pay down debt. The deleveraging signal fired on exactly the right businesses.

2000: +38.72% vs -10.50%. A +49.22% spread. 2001: +10.39% vs -9.17%. A +19.56% spread. 2002: +20.31% vs -19.92%. A +40.23% spread.

This is the ideal environment for the strategy: a selective bear market that punishes leverage in one sector while leaving profitable, debt-reducing companies in other sectors mostly untouched.

2005: +45.71%, +38.5% excess

The early commodity supercycle. Energy and materials companies had strong cash flows and were deploying them against debt. ROE was elevated, D/E ratios were falling, and the signal was capturing genuinely healthy businesses at the right moment in the cycle.

2007: +15.51%, +11.1% excess

Solid outperformance going into the financial crisis. Resource companies remained profitable while the credit bubble grew in the US.

2009-2010: +32.75% then +25.98%

Recovery outperformance. Companies that had maintained balance sheet discipline through the downturn were positioned better for the rebound than the leveraged ones that had been forced into restructuring.

2024-2025: Signal revival

2024: +28.99% vs +25.28% (+3.71% excess). 2025: +28.23% vs +15.34% (+12.89% excess).

Two consecutive years of outperformance, with the 2025 margin the strongest since the early 2000s commodity cycle. Canadian energy and materials companies benefited from commodity demand, and the deleveraging filter captured the disciplined subset.

The Weak Stretch: 2012-2021

Being honest about the bad years matters.

From 2012 to 2021, the strategy underperformed in most years, with several large gaps:

2013: +7.22% vs +27.77% (-20.55%). US equities began their tech-driven expansion. Canadian energy and materials companies faced commodity price softness as China growth slowed.

2019: -0.13% vs +32.31% (-32.44%). Almost flat while SPY gained a third of its value. Pipeline capacity constraints and US shale competition pressured Canadian energy profitability. Companies that had been deleveraging were running into earnings headwinds.

2020: +2.12% vs +15.64% (-13.52%). A COVID year driven by US tech recovery.

2021: +11.04% vs +31.26% (-20.22%). Strong absolute return, but a large gap in a year when speculative growth dominated.

The ZIRP era (2012-2021) created a specific problem for this strategy. When interest rates are near zero, the signal that distinguishes a genuinely disciplined company from a merely profitable one becomes weaker. Every company could borrow cheaply, so voluntary deleveraging was less meaningful as a differentiator. The TSX's sector bias toward energy and materials compounded this: those sectors underperformed US technology by historic margins during this window.

The weak stretch is real. Anyone running this strategy from 2012 forward would have underperformed SPY for most of a decade. That requires conviction the 25-year data and structural logic support.

The Down Capture Story

The 48.75% down capture is the most distinctive number in this backtest.

In years when SPY falls, this portfolio historically falls roughly half as much. The reasons compound:

Beta of 0.742 means the portfolio has lower systematic market exposure than SPY. The ROE + deleveraging filter naturally excludes the most financially fragile companies, which tend to fall the hardest in drawdowns. Canadian resource companies, when filtered for capital discipline, have real asset backing that supports valuations during equity market stress.

The 2008 example is instructive. The financial crisis hit leveraged financial companies, US banks, and over-extended mortgage lenders most acutely. Canadian resource companies that had been paying down debt weren't at the center of the crisis. The portfolio fell -36.94% vs SPY's -34.31%, a small difference in the worst year. That's the down capture holding even under the most severe conditions.

2022 shows the mechanism more cleanly. Rising rates hurt levered companies. The portfolio fell -12.77% vs SPY's -18.99%, a +6.22% relative result. Companies reducing debt are structurally less exposed to rate pressure.

Full Annual Returns

| Year | Strategy | SPY | Excess |

|---|---|---|---|

| 2000 | +38.72% | -10.50% | +49.22% |

| 2001 | +10.39% | -9.17% | +19.56% |

| 2002 | +20.31% | -19.92% | +40.23% |

| 2003 | +21.51% | +24.12% | -2.62% |

| 2004 | +15.67% | +10.24% | +5.43% |

| 2005 | +45.71% | +7.17% | +38.53% |

| 2006 | +5.70% | +13.65% | -7.95% |

| 2007 | +15.51% | +4.40% | +11.11% |

| 2008 | -36.94% | -34.31% | -2.63% |

| 2009 | +32.75% | +24.73% | +8.02% |

| 2010 | +25.98% | +14.31% | +11.67% |

| 2011 | -6.70% | +2.46% | -9.16% |

| 2012 | +4.66% | +17.09% | -12.43% |

| 2013 | +7.22% | +27.77% | -20.55% |

| 2014 | +6.19% | +14.50% | -8.30% |

| 2015 | -7.77% | -0.12% | -7.64% |

| 2016 | +21.09% | +14.45% | +6.64% |

| 2017 | +14.24% | +21.64% | -7.40% |

| 2018 | -10.12% | -5.15% | -4.97% |

| 2019 | -0.13% | +32.31% | -32.44% |

| 2020 | +2.12% | +15.64% | -13.52% |

| 2021 | +11.04% | +31.26% | -20.22% |

| 2022 | -12.77% | -18.99% | +6.22% |

| 2023 | -1.65% | +26.00% | -27.65% |

| 2024 | +28.99% | +25.28% | +3.71% |

| 2025 | +28.23% | +15.34% | +12.89% |

Returns are in CAD. SPY benchmark in USD.

Run This Screen

The SQL below replicates the current version of the screen on TSX stocks. It pulls the most recent two annual D/E ratios, computes the year-over-year change, filters for meaningful prior leverage, ROE above 8%, and market cap above C$500M. Results are sorted by largest D/E reduction.

WITH current_fy AS (

SELECT symbol, debtToEquityRatio AS de_current, date AS current_date

FROM financial_ratios

WHERE period = 'FY'

AND debtToEquityRatio IS NOT NULL

AND date >= CURRENT_DATE - INTERVAL 18 MONTH

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) = 1

),

prior_fy AS (

SELECT symbol, debtToEquityRatio AS de_prior

FROM financial_ratios

WHERE period = 'FY'

AND debtToEquityRatio IS NOT NULL

AND date >= CURRENT_DATE - INTERVAL 30 MONTH

AND date < CURRENT_DATE - INTERVAL 12 MONTH

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) = 1

),

km AS (

SELECT symbol, returnOnEquityTTM AS roe, marketCap

FROM key_metrics_ttm

)

SELECT

c.symbol, p.companyName, p.exchange, p.sector,

ROUND(c.de_current, 2) AS de_current,

ROUND(pr.de_prior, 2) AS de_prior,

ROUND((c.de_current - pr.de_prior) / pr.de_prior * 100, 1) AS de_change_pct,

ROUND(k.roe * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 2) AS market_cap_bn

FROM current_fy c

JOIN prior_fy pr ON c.symbol = pr.symbol

JOIN km k ON c.symbol = k.symbol

JOIN profile p ON c.symbol = p.symbol

WHERE pr.de_prior > 0.1

AND c.de_current >= 0

AND (c.de_current - pr.de_prior) / pr.de_prior < -0.10

AND k.roe > 0.08

AND k.marketCap > 500000000

AND p.exchange IN ('TSX')

ORDER BY (c.de_current - pr.de_prior) / pr.de_prior ASC

LIMIT 30

Limitations

Sector concentration. The TSX's energy and materials weighting means this portfolio carries implicit sector bets. When commodities underperform, as they did through most of 2012-2021, the strategy underperforms. It's not a sector-neutral factor strategy. It's a factor strategy operating inside a cyclical sector ecosystem.

Currency. Returns are in CAD. For USD investors, the CAD/USD exchange rate adds volatility on top of market risk. Long-run CAD has been relatively stable against USD, but there are extended periods of divergence. The comparison to SPY in USD understates the currency risk for non-Canadian investors.

+1.32% excess is thin. Transaction costs, withholding taxes on dividends for foreign investors, and rebalancing friction can close this gap. The practical outperformance for many real investors is lower than the backtest figure.

Annual data lag. The 45-day filing lag creates backward-looking bias. Commodity companies can deteriorate faster than their annual filings reflect, particularly in sharp commodity downturns. The 2008 result (-2.6% relative, roughly matching SPY) partly reflects the strategy entering the year with strong balance sheet companies that deteriorated as the crisis deepened.

Concentrated selection. 24.7 average stocks is a small portfolio. Individual company events move annual returns in ways a broad index doesn't experience.

Takeaway

Canada's deleveraging backtest earns its ranking as the best risk-adjusted result in the global series, not because the excess return is large, but because the return comes with a risk profile that's genuinely different from the market.

Down capture of 48.75%. Max drawdown lower than SPY. Sharpe 0.383. Beta 0.742. A $10K investment compounding to $99.5K vs SPY's $73K.

The structural reason holds up. Canada's resource-heavy economy creates genuine, recurring opportunities for capital-disciplined companies to deleverage meaningfully. The TSX's thinner coverage and mid-cap cyclical composition give the signal room to work before the market fully prices it. The result is a portfolio that earns modestly more over 25 years while falling substantially less when markets drop.

The weak 2012-2021 stretch is honest context. This strategy doesn't outperform in a low-rate, tech-driven bull market that rewards leverage and growth. It outperforms in commodity cycles, rising rate environments, and selective bear markets that punish financial stress. The 2022 and 2025 results suggest that environment may be returning.

For investors who want Canadian equity exposure with lower volatility than the broad TSX and a systematic filter for capital discipline, the 25-year track record makes a defensible case.

Part of a Series: Global | US | India

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse). Backtest period Q1 2000 - Q4 2025. Returns in CAD. SPY benchmark in USD. Not investment advice.