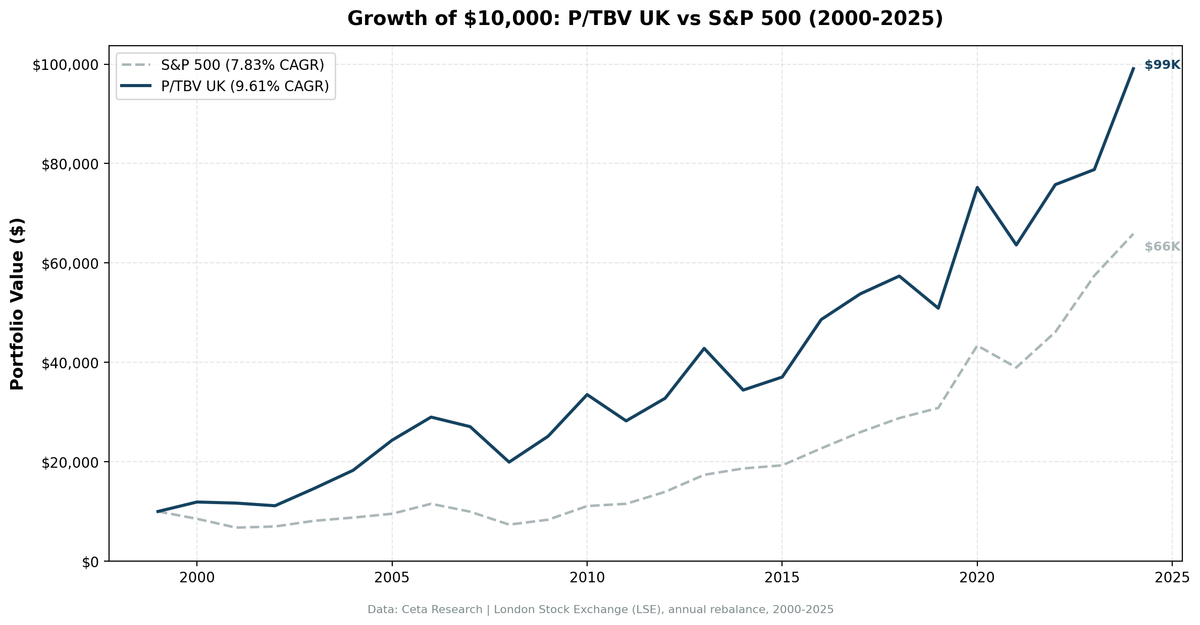

Price-to-Tangible-Book in the UK: 9.61% CAGR with the Lowest Drawdown

The P/TBV strategy on the London Stock Exchange returned 9.61% annualised over 25 years against SPY's 7.83%, adding 1.78% per year while drawing down to only -31.25% at its worst. That maximum drawdown figure is the standout: it's the lowest of any outperforming exchange we tested, and it comes from a market structurally tilted toward physical assets. When the strategy does fall, it falls less far than its US equivalent.

Contents

The Strategy

Price-to-Tangible-Book strips goodwill and intangibles out of book value before dividing into market cap. The formula: P/TBV = marketCap / (totalStockholdersEquity - goodwill - intangibleAssets). What remains is the value of things you can actually touch: factories, equipment, land, inventory, receivables.

This distinction matters enormously in a market like the UK, where industrials, financials, and energy companies dominate the large-cap index. These businesses carry real asset bases. A bank's book value is largely loans and securities. A manufacturer's book value is machinery and property. Stripping intangibles gives you a cleaner picture of whether you're paying a fair price for the physical business.

Quality filters prevent the strategy from buying cheap-but-broken companies. We require ROE above 8%, ROA above 3%, and operating profit margin above 10%. These thresholds keep the portfolio in profitable businesses with real earnings power, not just cheap balance sheets.

| Parameter | Value |

|---|---|

| Signal | P/TBV ascending (lowest first) |

| Quality filters | ROE > 8%, ROA > 3%, OPM > 10% |

| Rebalance | Annual (July), 45-day filing lag |

| Portfolio size | Top 30, equal weight |

| Minimum stocks | 10 (else cash) |

| Market cap threshold | £500M (~$635M USD) |

| Universe | London Stock Exchange |

| Period | 2000-2025 (25 years) |

| Benchmark | SPY |

What We Found

The UK never went to cash over 25 years, averaging 20.7 stocks per period. That consistency matters. The strategy always found enough qualifying companies, which reflects how tangible-asset-heavy the LSE universe is relative to US markets where software and pharma companies (heavy on intangibles) dominate.

The down-capture ratio of 36.47% is what separates this from a plain UK equity bet. In years where SPY fell, the UK P/TBV portfolio typically fell much less. In 2007, SPY dropped 13.71%. The strategy lost only 6.62%, roughly half. In 2008, both fell similarly (-26.38% vs -26.14%), which represents the worst-case scenario. The financial crisis hit UK banks as hard as any market, and banks are a substantial part of the low P/TBV universe. That one year is the exception, not the rule.

Three years stand out for different reasons. The 2003-2005 stretch produced +31%, +25%, and +33% in consecutive years. UK industrials and financials were deep value coming out of the 2001-2002 downturn, and the strategy captured that recovery cleanly. In 2016, the strategy returned +31.23% against SPY's +17.73%. The Brexit vote repriced UK assets aggressively lower in GBP terms, creating extreme tangible-book discounts. The portfolio entered a period of genuine undervaluation and recovered sharply within months.

The weak spots are 2011 and 2021. Both years coincided with UK-specific political uncertainty, the Eurozone crisis dragging on UK financials in 2011 and post-COVID inflation expectations in 2021. In both cases, stocks exposed to real-asset intensive sectors (which describes most of the LSE portfolio) underperformed as rate expectations shifted. These aren't random noise. They're the same sector exposure that drives outperformance working against the strategy when rate environments flip.

The low maximum drawdown of -31.25% versus the US strategy's -38.73% means that in any given crisis, UK tangible-book investors recover from a shallower hole. Compounded over 25 years, that preservation advantage adds up.

Annual Returns

| Year | Strategy | SPY |

|---|---|---|

| 2000 | +19.01% | -14.78% |

| 2001 | -1.83% | -20.77% |

| 2002 | -4.56% | +3.29% |

| 2003 | +31.10% | +16.44% |

| 2004 | +25.01% | +7.94% |

| 2005 | +33.16% | +8.86% |

| 2006 | +19.13% | +20.95% |

| 2007 | -6.62% | -13.71% |

| 2008 | -26.38% | -26.14% |

| 2009 | +26.13% | +13.42% |

| 2010 | +33.33% | +32.94% |

| 2011 | -15.78% | +4.10% |

| 2012 | +16.15% | +20.85% |

| 2013 | +30.59% | +24.50% |

| 2014 | -19.58% | +7.38% |

| 2015 | +7.60% | +3.36% |

| 2016 | +31.23% | +17.73% |

| 2017 | +10.62% | +14.34% |

| 2018 | +6.67% | +10.91% |

| 2019 | -11.27% | +7.12% |

| 2020 | +47.73% | +40.68% |

| 2021 | -15.39% | -10.17% |

| 2022 | +19.08% | +18.31% |

| 2023 | +4.01% | +24.60% |

| 2024 | +25.74% | +14.67% |

The Current Screen

The US screen is available at cetaresearch.com/data-explorer?q=z9gpaUlNfi. Exchange-specific queries including LSE can be run directly on the data explorer at cetaresearch.com.

Limitations

Currency effects are real. These returns are calculated in local currency (GBP). A US-based investor would also take on GBP/USD exposure, which adds variance in both directions. Post-Brexit sterling weakness has been a persistent headwind for unhedged foreign investors.

The LSE universe is concentrated in financials and industrials. When those sectors face systemic stress, as in 2008 and 2011, the strategy has no refuge. The quality filters help but don't fully insulate against sector-level crises.

The market cap threshold of £500M cuts out small caps entirely. There's evidence that the P/TBV premium is stronger in smaller stocks, so this threshold may be leaving some of the factor's historical return on the table in exchange for liquidity and tradability.

Part of a Series

This post is part of a multi-exchange series on the Price-to-Tangible-Book strategy. The US flagship backtest, including full methodology and the complete global results summary, is at ptbv-strategy-us-backtest.

Part of a Series: Global | US | Sweden | India | Germany | China | Canada

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Full methodology: backtests/METHODOLOGY.md