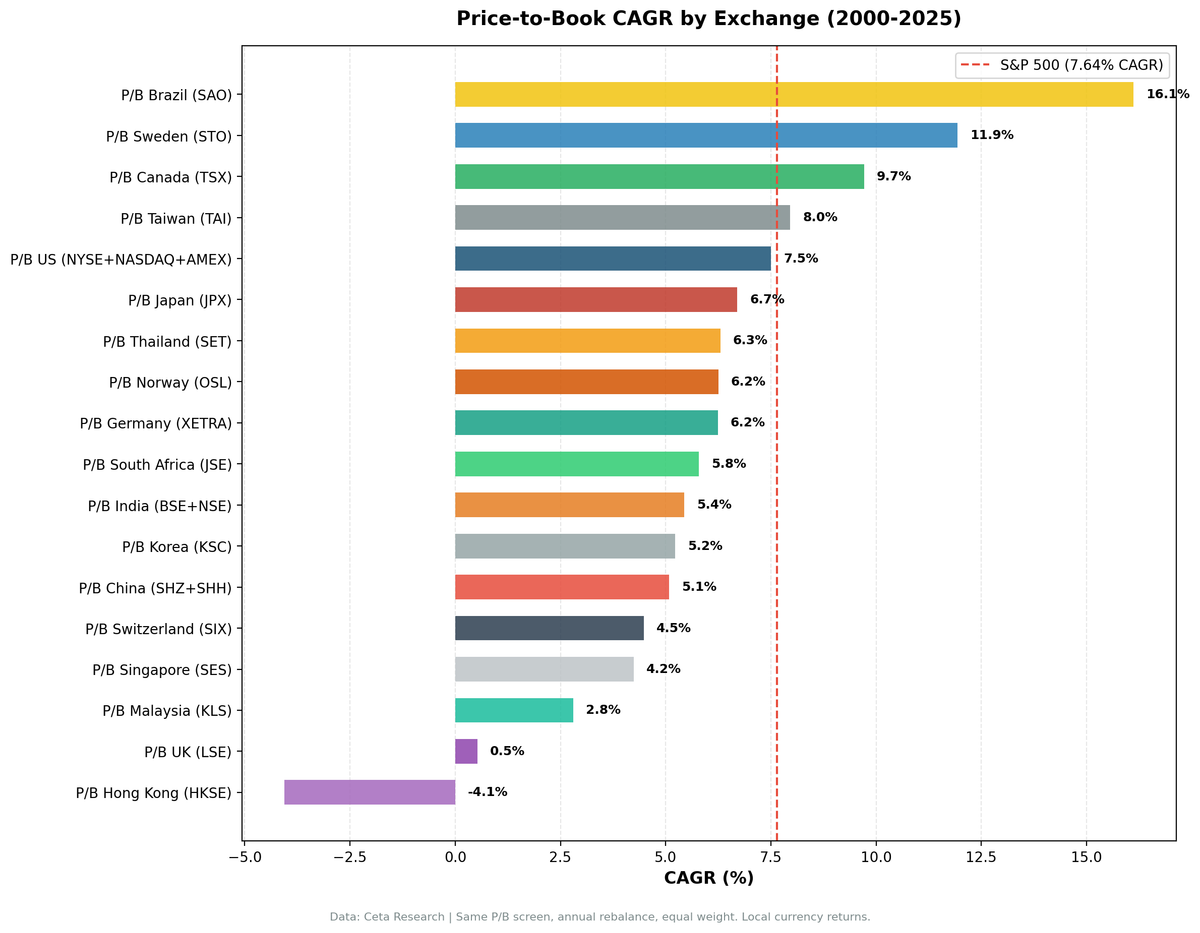

Price-to-Book Across 18 Exchanges: Only 4 Beat SPY

We ran the same P/B screen across 18 stock exchanges, 25 years of data, and compared every result to the S&P 500 benchmark. Four exchanges beat SPY. Fourteen didn't. That's the honest result, and it's worth understanding exactly where the value premium survived and where it didn't.

Contents

- Method

- The Full Results

- Finding 1: Where the Premium Survived

- Finding 2: The Emerging Market Divide

- Finding 3: Why the UK Failed

- Finding 4: The Hong Kong Catastrophe

- Finding 5: The Currency Caveat

- Data Quality and Exclusions

- Takeaway

- Related Analysis

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Period: 2000–2025 (25 annual periods)

- Strategy: Top 30 stocks by lowest P/B ratio, annual rebalance, equal weight

- Quality filters: ROE > 10%, interest coverage > 3, operating margin > 10%

- Market cap filter: Per-exchange minimum (not a uniform $1B USD)

- Returns: Local currency (not converted to USD)

- Benchmark: SPY (7.64% CAGR, -34.9% max drawdown over the same period)

The same screen ran on each exchange. Same filters, same position count, same rebalance frequency. Differences in outcomes reflect genuine differences in how the P/B premium behaves across markets, not methodological inconsistency.

Norway (OSL) is excluded from the "beat SPY" ranking because it had 32% cash periods, meaning the screen regularly found fewer than 30 qualifying stocks. A portfolio that's one-third cash nearly a third of the time isn't a clean P/B test.

The Full Results

| Exchange | CAGR | Excess vs SPY | Sharpe | Max DD | Cash% | Avg Stocks |

|---|---|---|---|---|---|---|

| Brazil (SAO) | 16.12% | +8.47% | 0.168 | -39.1% | 8% | 22.9 |

| Sweden (STO) | 11.93% | +4.29% | 0.447 | -39.8% | 8% | 26.8 |

| Canada (TSX) | 9.72% | +2.08% | 0.308 | -46.3% | 0% | 23.0 |

| Taiwan (TAI) | 7.96% | +0.32% | 0.291 | -45.8% | 24% | 27.9 |

| US (NYSE+NASDAQ+AMEX) | 7.50% | -0.15% | 0.225 | -52.3% | 0% | 21.2 |

| Japan (JPX) | 6.70% | -0.95% | 0.290 | -44.7% | 4% | 27.7 |

| Thailand (SET) | 6.30% | -1.34% | 0.158 | -51.9% | 20% | 24.8 |

| Norway (OSL) | 6.25% | -1.40% | 0.149 | -54.1% | 32% | 22.1 |

| Germany (XETRA) | 6.24% | -1.40% | 0.193 | -48.0% | 0% | 18.5 |

| South Africa (JNB) | 5.79% | -1.85% | -0.169 | -31.2% | 24% | 23.7 |

| India (BSE+NSE) | 5.44% | -2.21% | -0.028 | -64.8% | 20% | 23.6 |

| Korea (KSC) | 5.22% | -2.42% | 0.113 | -44.1% | 24% | 26.9 |

| China (SHZ+SHH) | 5.08% | -2.57% | 0.053 | -59.7% | 0% | 25.8 |

| Switzerland (SIX) | 4.48% | -3.16% | 0.201 | -53.8% | 0% | 15.7 |

| Singapore (SES) | 4.24% | -3.41% | 0.096 | -47.8% | 16% | 12.7 |

| Malaysia (KLS) | 2.81% | -4.83% | 0.041 | -44.4% | 28% | 15.5 |

| UK (LSE) | 0.53% | -7.12% | -0.090 | -76.9% | 0% | 15.2 |

| Hong Kong (HKSE) | -4.06% | -11.71% | -0.245 | -90.5% | 0% | 17.4 |

Returns in local currency. Norway excluded from analysis due to >30% cash periods.

Finding 1: Where the Premium Survived

The four exchanges that beat SPY share a pattern. Brazil and Canada are resource-heavy markets where physical assets dominate balance sheets. Sweden is an industrial economy with a long tradition of capital-intensive manufacturing. Taiwan is electronics manufacturing, where book value meaningfully reflects the factories and equipment behind the products.

In each case, book value is a real number. Factories, mines, timber tracts, semiconductor fabs. When a company trades below its book value on these exchanges, it's actually cheap relative to the hard assets backing it.

Sweden stands out even within this group. Its Sharpe ratio of 0.447 is the best of all 18 exchanges, better than Japan (0.290), Canada (0.308), and well above the US (0.225). A 0.447 Sharpe means Sweden generated strong returns with relatively low volatility, not just raw gains. The down capture was 51.56%. When SPY fell 10%, the Swedish P/B portfolio fell only about 5%. That asymmetry, strong up capture and modest down capture, explains why it compounds so well over time.

Canada's 9.72% CAGR on zero cash periods is clean. The screen found qualifying stocks in every period, energy and materials companies with depressed valuations that eventually recovered. The commodity super-cycle from 2000 to 2008 was particularly good to this portfolio.

Brazil's 16.12% CAGR leads the table by a wide margin, but comes with the important caveat that these are BRL returns. Brazilian inflation and interest rates mean the nominal CAGR looks different from a USD-converted perspective. Still, the strategy generated substantial excess returns even relative to local benchmarks. The BRL environment is also one where banks and resource companies genuinely trade below tangible book, for reasons that are more identifiable than in developed markets.

Finding 2: The Emerging Market Divide

The gap between Brazil (16.12%) and India (5.44%) or China (5.08%) is striking, given that all three are often grouped as "high-growth EM" markets.

Brazil had a specific combination that worked: large commodity and banking sectors, where P/B is a meaningful valuation anchor; genuine book value accountability (banks have to mark their loans, miners have real assets); and a market that regularly produces deep value situations as political and currency crises cause indiscriminate selling. Each crisis created fresh P/B opportunities that eventually resolved.

India and China didn't behave the same way. India's -64.8% max drawdown tells the story. The Indian market had violent drawdowns in 2008, 2011, and 2020, and the P/B portfolio wasn't spared. In fact it was often worse than the benchmark during these episodes because value stocks in India tend to include state-owned enterprises and legacy industrials that trail the growth sectors driving Indian equity performance over this period.

China's 5.08% CAGR with a -59.7% max drawdown reflects a different problem. Chinese book values are often questionable. State-owned enterprises regularly trade below stated book value for rational reasons: the book value is either inflated, not available to minority shareholders, or both. The P/B signal in China is noisy in ways it isn't in, say, Sweden or Canada.

Hong Kong is in a category of its own and gets its own section below.

Finding 3: Why the UK Failed

The UK result is the most academically interesting failure. The LSE produced 0.53% CAGR, a -7.12% gap versus SPY, and a negative Sharpe ratio of -0.090 over 25 years. This is the market where Fama and French's value premium was most extensively replicated internationally.

The explanation is structural, not random. The UK economy shifted decisively toward services over this period. Banking, insurance, professional services, and consumer brands. In a service-heavy economy, book value is increasingly a poor measure of corporate worth. Brands, customer relationships, technology platforms, and intellectual property don't appear on the balance sheet. A bank trading at 0.8x book after a credit event genuinely is cheap. A media company trading at 0.9x book might just have no assets worth measuring.

The UK P/B screen in 2000 would have found financial companies, retailers, and manufacturers. The financial companies were crushed in 2008 and never fully recovered the period's losses. The retailers ran into structural decline from Amazon and digital commerce. The manufacturers competed against cheaper European and Asian producers.

There's also the Brexit effect. From 2016 onward, UK equities traded at persistent discounts to European peers, and that discount didn't resolve into recoveries the way historical P/B logic would predict. UK companies went from cheap to cheaper, with the P/B portfolio consistently behind the benchmark.

Finding 4: The Hong Kong Catastrophe

HKSE produced -4.06% CAGR and a -90.5% max drawdown. No other exchange in this study came close to that drawdown figure.

This isn't just a bad run. It's a compounding failure across multiple distinct phases. The P/B portfolio was heavy in property developers and financial companies, both sectors with high book values and volatile earnings. Hong Kong property stocks peaked around 2007, crashed through 2008, partially recovered, then entered a second prolonged decline from 2019 onward driven by the political situation and regulatory changes affecting cross-border business.

A -90.5% max drawdown means the portfolio, at its worst point, was down 90.5% from peak. That's near-total capital destruction from peak to trough. The strategy didn't just fail in the 2008 financial crisis. It accumulated losses through multiple distinct downturns without adequate recovery periods between them.

The underlying problem is similar to China but more severe: HKSE book values were heavily concentrated in property and finance, sectors where book value matters but where book value itself was inflated during the bubble years. Buying "cheap" property developers at 0.7x book in 2007 meant buying companies whose book values were about to be written down substantially.

The currency is also relevant. HKD is pegged to USD, so there's no currency caveat here. These are effectively USD-equivalent returns. The negative 4.06% CAGR is the real story.

Finding 5: The Currency Caveat

All returns in this study are in local currency. This matters more for some exchanges than others.

For markets like Japan (JPY) and Switzerland (CHF), local currency returns are a reasonable proxy for what a local investor would experience. Currency effects over a 25-year period can be large, but they average out more than short-term comparisons suggest.

For Brazil (BRL), the 16.12% CAGR should be treated with particular care. Brazil experienced significant inflation across this period, and BRL weakened substantially against USD. An international investor converting BRL returns to USD would show a materially different result. The alpha vs. the Brazilian benchmark remains meaningful; the absolute number less so for a non-Brazilian investor.

For markets like India and Thailand, local currency returns overstate what a USD-denominated investor would experience, as both INR and THB weakened against USD over the period.

The comparison benchmark (SPY) is in USD. So the excess return figures need this caveat: for most non-US exchanges, the "excess return vs SPY" comparison isn't apples-to-apples on a currency-adjusted basis.

Data Quality and Exclusions

Norway excluded: 32% cash periods. The screen couldn't find enough qualifying stocks in many periods, meaning the strategy wasn't being tested cleanly.

Australia (ASX) excluded from analysis: Adjusted close data quality issues with split handling.

Taiwan (24% cash, 27.9 avg stocks): Included but with limited qualifying periods. The 24% cash rate means roughly 6 out of 25 periods had fewer than 30 stocks.

Singapore (16% cash, 12.7 avg stocks): Included. The low average stock count (12.7) indicates thin qualification. Concentrated portfolio by design.

All other exchanges had clean data and full qualification periods.

Takeaway

The P/B premium is real but conditional. It survives in markets where book value measures something. Canada's mines, Sweden's factories, Brazil's banks, Taiwan's fabs. It struggles in markets where intangible value has displaced hard assets, which is most of the developed world's service-heavy economies.

The UK result is the clearest illustration. Fama and French found the value premium there decades ago. The market responded by pricing it away, and then the economy shifted underneath the strategy. By the time our backtest period starts, the premium was gone.

Hong Kong is a cautionary example of how a P/B strategy can compound losses when book values themselves are overstated and recovery cycles are cut short by macroeconomic and political disruption.

If you're going to run a global P/B strategy, the lesson from 18 exchanges is: check what's in the book. In some markets, that's real. In others, it's mostly air.

Related Analysis

- P/B Value Strategy: US Markets Deep Dive

- P/B Value Strategy: Sweden Best Sharpe of 18 exchanges (0.447).

- P/B Value Strategy: Canada Resource stocks, 8% down capture, +48pp in 2022.

- P/B Value Strategy: Brazil Highest alpha (+8.47%). Returns in BRL.

Part of a Series: US | Sweden | Canada | Brazil

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse, 2000–2025) Returns in local currency. All results gross of transaction costs. Past performance doesn't guarantee future results. This is educational content, not investment advice.