Low Debt Quality Stocks: Sweden (STO) — 25-Year Backtest

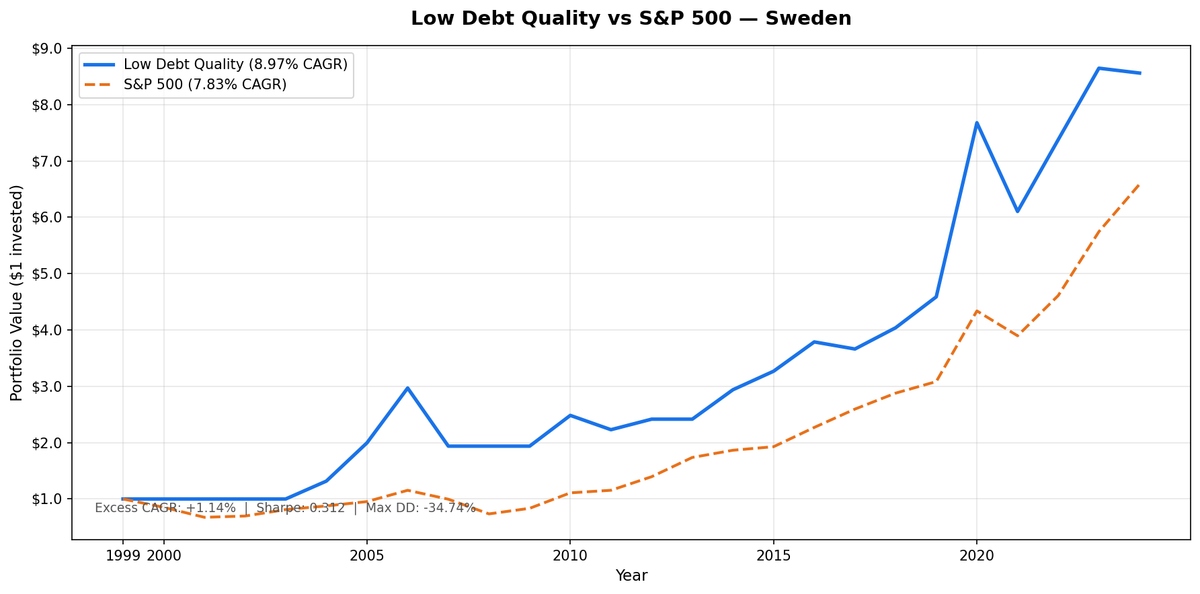

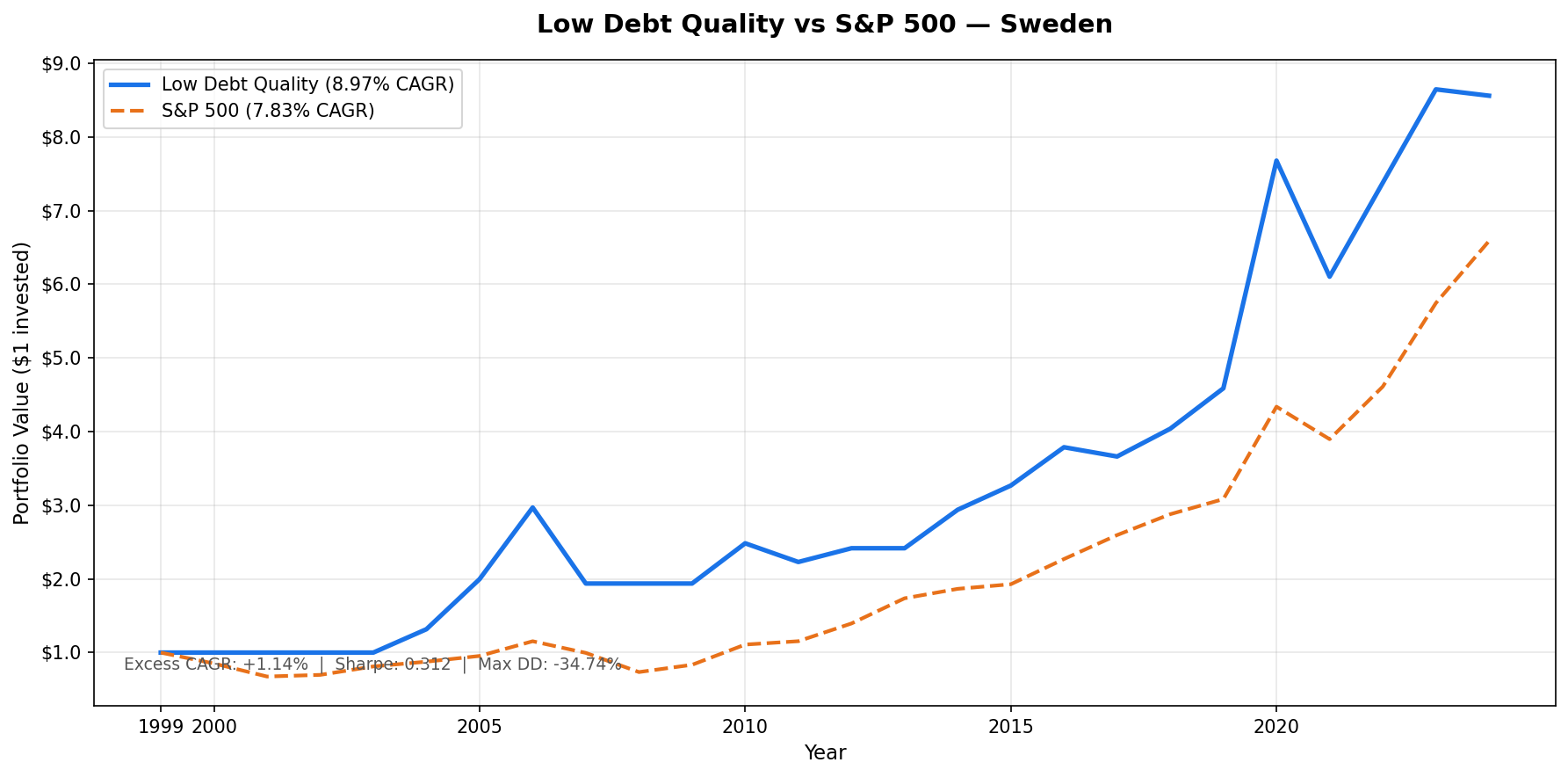

Sweden's low-debt, high-quality portfolio returned 8.97% CAGR over 25 years vs 7.83% for SPY. Total return: 755.80% vs 558.69%. The universe is thin: 22 stocks on average, with 7 cash periods where fewer than 10 qualified. Still, the strategy outperformed. The up-capture of 106.29% tells part of the story. In good years, Sweden's best companies outperformed the S&P 500 outright.

Contents

- Method

- The Signal

- The Screen (SQL)

- What We Found

- Annual Returns (July to July)

- The GFC Cash Shelter

- The Burst Years: 2004–2006

- 2007: The Drawdown Risk

- 2020: +67.4%

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- Run This Screen Yourself

Method

- Universe: Stockholm Stock Exchange (STO) stocks with market cap above SEK 5B, actively trading.

- Period: July 2000 to July 2025 (25 annual holding periods).

- Rebalance: Annual, each July. Equal weight across all qualifying stocks.

- Benchmark: S&P 500 Total Return (SPY), in USD. Portfolio returns in SEK.

- Cash rule: Hold cash if fewer than 10 stocks qualify. Sweden had 7 cash periods (2000, 2001, 2002, 2003, 2008, 2009, 2013).

- Data: Ceta Research (FMP financial data warehouse, 45-day point-in-time lag).

The Signal

Two filters define the portfolio.

D/E < 0.5 (Debt/Equity from annual financial statements). Swedish large-caps include heavy industrials: Volvo, Atlas Copco, Sandvik. These are good businesses, but capital-intensive. The leverage filter screens out companies that rely on debt to operate. What's left tends toward software, specialty retail, pharmaceuticals, and asset-light industrials. AstraZeneca, Evolution, Hexagon types.

Piotroski F-Score >= 7 (out of 9). The score flags companies that are financially improving across nine dimensions:

- F1: Net income > 0

- F2: Operating cash flow > 0

- F3: Return on assets improved year-over-year

- F4: Operating cash flow > net income (earnings quality check)

- F5: Long-term debt ratio decreased

- F6: Current ratio improved

- F7: No dilution (shares outstanding didn't increase)

- F8: Asset turnover improved

- F9: Gross margin improved

A company scoring 7 or above is profitable, generating real cash, and improving most operating metrics. The D/E filter ensures that improvement isn't funded by leverage.

On the STO, 22 stocks average per year is a concentrated result. The strict filter works well in large liquid markets. For a smaller exchange like Stockholm, it creates genuine concentration risk. Seven years where the strategy sat entirely in cash also compress the compounding effect.

The Screen (SQL)

Run this on current data to see today's qualifying Swedish stocks:

SELECT p.exchange, r.symbol, p.companyName, p.sector,

ROUND(r.debtToEquityRatioTTM, 3) AS de_ratio,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(r.operatingProfitMarginTTM * 100, 1) AS opm_pct,

ROUND(r.interestCoverageRatioTTM, 1) AS interest_coverage,

ROUND(k.freeCashFlowYieldTTM * 100, 2) AS fcf_yield_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM financial_ratios_ttm r

JOIN key_metrics_ttm k ON r.symbol = k.symbol

JOIN profile p ON r.symbol = p.symbol

WHERE r.debtToEquityRatioTTM >= 0

AND r.debtToEquityRatioTTM < 0.50

AND k.returnOnEquityTTM > 0.08

AND r.operatingProfitMarginTTM > 0.08

AND r.interestCoverageRatioTTM > 5.0

AND p.isActivelyTrading = true

AND k.marketCap > 5000000000

AND p.exchange IN ('STO')

ORDER BY de_ratio ASC

LIMIT 30

What We Found

| Metric | Portfolio | SPY |

|---|---|---|

| CAGR | 8.97% | 7.83% |

| Total Return | 755.80% | 558.69% |

| Max Drawdown | -34.74% | -36.27% |

| Sharpe Ratio | 0.312 | — |

| Volatility | 22.35% | — |

| Down Capture | 64.57% | — |

| Up Capture | 106.29% | — |

| Win Rate | 44% | — |

| Cash Periods | 7/25 | — |

| Avg Stocks | 22 | — |

Annual Returns (July to July)

| Year | Portfolio (SEK) | SPY (USD) | Excess |

|---|---|---|---|

| 2000 | 0.0% (cash) | -14.8% | +14.8% |

| 2001 | 0.0% (cash) | -20.8% | +20.8% |

| 2002 | 0.0% (cash) | +3.3% | -3.3% |

| 2003 | 0.0% (cash) | +16.4% | -16.4% |

| 2004 | +31.7% | +7.9% | +23.8% |

| 2005 | +51.6% | +8.9% | +42.7% |

| 2006 | +48.7% | +20.9% | +27.8% |

| 2007 | -34.7% | -13.7% | -21.0% |

| 2008 | 0.0% (cash) | -26.1% | +26.1% |

| 2009 | 0.0% (cash) | +13.4% | -13.4% |

| 2010 | +28.2% | +32.9% | -4.8% |

| 2011 | -10.2% | +4.1% | -14.3% |

| 2012 | +8.4% | +20.9% | -12.5% |

| 2013 | 0.0% (cash) | +24.5% | -24.5% |

| 2014 | +21.6% | +7.4% | +14.2% |

| 2015 | +11.2% | +3.4% | +7.8% |

| 2016 | +15.9% | +17.7% | -1.8% |

| 2017 | -3.3% | +14.3% | -17.7% |

| 2018 | +10.3% | +10.9% | -0.6% |

| 2019 | +13.6% | +7.1% | +6.5% |

| 2020 | +67.4% | +40.7% | +26.7% |

| 2021 | -20.5% | -10.2% | -10.3% |

| 2022 | +20.9% | +18.3% | +2.6% |

| 2023 | +17.2% | +24.6% | -7.4% |

| 2024 | -1.0% | +14.7% | -15.7% |

The GFC Cash Shelter

Cash in 2008 produced 0.0% return. SPY fell 26.1%. That +26.1 percentage point gap is one of the widest in the table. Sweden's strict quality filter found fewer than 10 acceptable stocks going into the GFC period. The strategy sat out. From the portfolio's perspective, not losing money is the same as gaining relative to a falling benchmark.

The same happened in 2000 and 2001 during the dot-com bust. Three consecutive cash years (2000, 2001, 2002) meant missing both the crash and the partial recovery. The net effect over those three years: the cash portfolio gained +32.3% relative to SPY's combined loss of -30.3%. That's a 62.6 percentage point swing across three years, all from holding cash.

The Burst Years: 2004–2006

When the universe opened up post-2003 (2004 was the first invested year), Sweden exploded. +31.7% in 2004, +51.6% in 2005, +48.7% in 2006. Three consecutive years of returns that crushed the S&P 500 by 23.8, 42.7, and 27.8 percentage points respectively.

This was partly a post-bust recovery for quality European companies. But it also reflects the concentration effect: 22 stocks, equal-weighted, means individual winners carry significant weight. When the quality filter correctly identifies a cohort of outperformers, the concentrated portfolio amplifies the result.

2007: The Drawdown Risk

The inverse is also true. 2007 was -34.7% for the portfolio vs -13.7% for SPY. A concentrated portfolio of 22 stocks in a single market with above-average volatility (22.35% annualized) will have bad years. 2021 was another: -20.5% vs -10.2%. These drawdown periods are the real cost of concentration.

The 64.57% down capture shows that overall, Sweden doesn't fall as hard as SPY in negative years. But the worst single-year drawdowns can exceed SPY substantially when the concentrated portfolio happens to have the wrong names.

2020: +67.4%

The COVID recovery year stands out. Sweden's portfolio returned 67.4% (July 2020 to July 2021), beating SPY by 26.7 points. The SEK strengthened against USD during this period, which added to the comparison. The underlying businesses also recovered faster: quality companies with low debt don't face refinancing risk in a crisis, and they can invest while leveraged competitors are constrained.

Backtest Methodology

| Parameter | Value |

|---|---|

| Universe | STO, market cap > SEK 5B |

| Period | July 2000 – July 2025 |

| Rebalance | Annual, July |

| Weighting | Equal weight |

| D/E threshold | < 0.5 (annual FY statements) |

| Piotroski minimum | F-Score >= 7 |

| Cash rule | < 10 qualifying stocks → hold cash |

| Benchmark | SPY (S&P 500 Total Return) |

| Returns | Portfolio in SEK, SPY in USD |

| Data lag | 45-day point-in-time |

| Data source | Ceta Research / FMP warehouse |

Limitations

Thin universe. 22 stocks average is a small portfolio. Each stock carries roughly 4.5% weight. A single company blowing up or surging dramatically shifts the annual return. This amplifies both gains and losses relative to a diversified index.

Cash periods as selection bias. Seven years in cash means the strategy was only active for 18 of 25 years. Cash years happen when the filter finds fewer than 10 qualifying stocks. That's often during or after market dislocations when quality companies are scarce. The strategy may appear to benefit from cash timing, but this is mechanical: strict filters exclude most stocks when conditions deteriorate.

Currency mismatch. Portfolio in SEK vs SPY in USD means SEK/USD fluctuations affect the comparison. Years when SEK weakened hurt the relative comparison. Years when SEK strengthened helped. This isn't hedged in the backtest.

No transaction costs. Annual rebalancing of 22 stocks on the STO has friction. Spreads on smaller Swedish names can be meaningful. Real-world returns would be somewhat lower.

Short effective history. The portfolio wasn't invested until 2004. Meaningful comparisons only cover 21 invested years. The cash years at the start and during the GFC mean the compounding base is different from a strategy that was always invested.

Takeaway

Sweden shows that a strict quality filter can outperform even when the universe is thin and cash periods are frequent. The +1.14% CAGR excess over 25 years came from a portfolio that averaged 22 stocks, sat in cash 7 times, but captured 106.29% of SPY's upside in the years it was invested.

The concentrated nature of the portfolio creates volatility (22.35% annualized). That's the trade-off: more upside capture than SPY in good years, but drawdowns that can exceed SPY's in concentrated bad years. Investors who can tolerate the swings and understand the mechanics have seen the math work out over a full cycle.

Part of a Series

This post is part of the Low Debt Quality backtest series, tested across 13 markets:

Run This Screen Yourself

The SQL above runs on live TTM data. It surfaces today's qualifying Swedish companies using the same balance sheet logic. The live screen won't compute a full Piotroski score (that requires multi-year FY data), but the D/E and profitability filters give a reasonable first pass at the universe.

Part of a Series: Global | US | UK | Thailand | Taiwan | Switzerland | Japan | India

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse. Returns in SEK. Annual rebalance July, equal weight, 2000–2025.