Deleveraging Tested on 13 Markets: Only 2 Beat SPY

Contents

- How the Strategy Works

- Full Results: 13 Exchanges (2001-2025)

- The Signal Globally: Works Pre-2013, Breaks After

- The Outperformers: India and Canada

- India: 12.40% CAGR, +4.39% Excess

- Canada: 9.33% CAGR, +1.32% Excess

- The Middle Ground: Sweden, Germany, Japan, Switzerland

- The Signal Failures: US, UK, Thailand, Hong Kong

- United States: 3.78% CAGR, -4.23% Excess

- UK: 3.44% CAGR, -4.57% Excess

- Thailand: 3.16% CAGR, -4.85% Excess

- Hong Kong: -0.84% CAGR, -8.85% Excess

- Exchanges Excluded from This Analysis

- Check Today's Global Count

- Why the Regime Explanation Matters

- Strategy Limitations

- What This Tells You

We ran the same deleveraging screen on 13 global stock exchanges. The signal, companies cutting their debt-to-equity ratio by 10%+ year-over-year while maintaining ROE above 8%, outperformed SPY in exactly two of them.

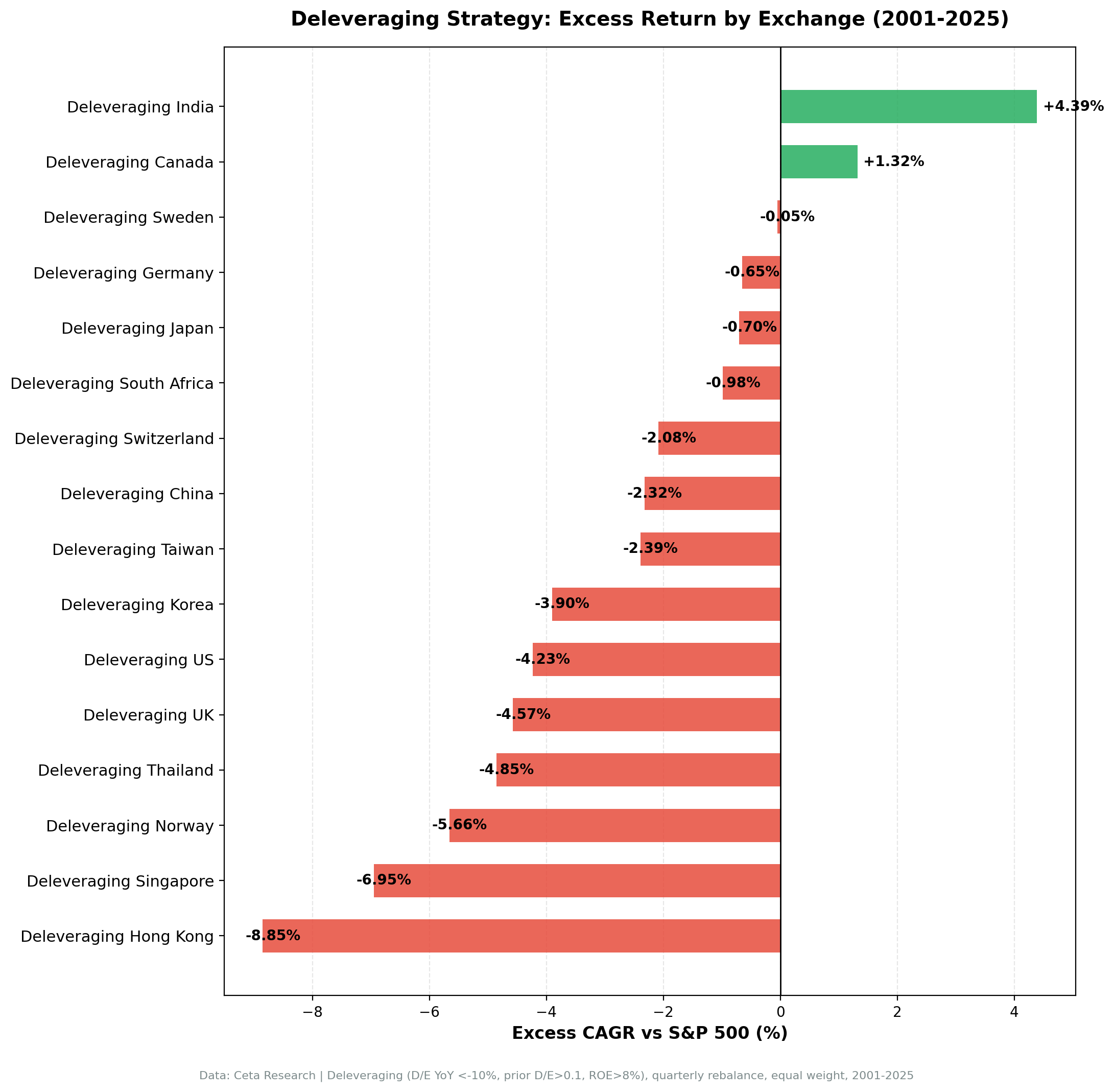

India returned 12.40% CAGR over the 2001-2025 period, beating SPY by 4.39 percentage points. Canada returned 9.33%, a 1.32% annual edge. Everyone else trailed. Hong Kong finished at -0.84% annually, the only market with a negative long-run CAGR, and the worst of the group by every metric including down capture.

This isn't a universal factor. It's a regime-dependent signal that works in specific structural conditions and breaks everywhere else.

How the Strategy Works

The screen is straightforward. Each year, we identify companies where:

- D/E ratio declined 10%+ from the prior fiscal year

- ROE > 8% (profitability filter)

- Market cap above the exchange-appropriate threshold

We select the top 30 qualifying stocks by magnitude of D/E reduction, weight them equally, and rebalance annually each July. Annual filing data with a 45-day lag prevents look-ahead bias. Transaction costs scale by market cap tier: 0.1% for large caps, 0.3% for mid, 0.5% for small.

All returns are in local currency. SPY benchmark is 8.01% CAGR over the same period.

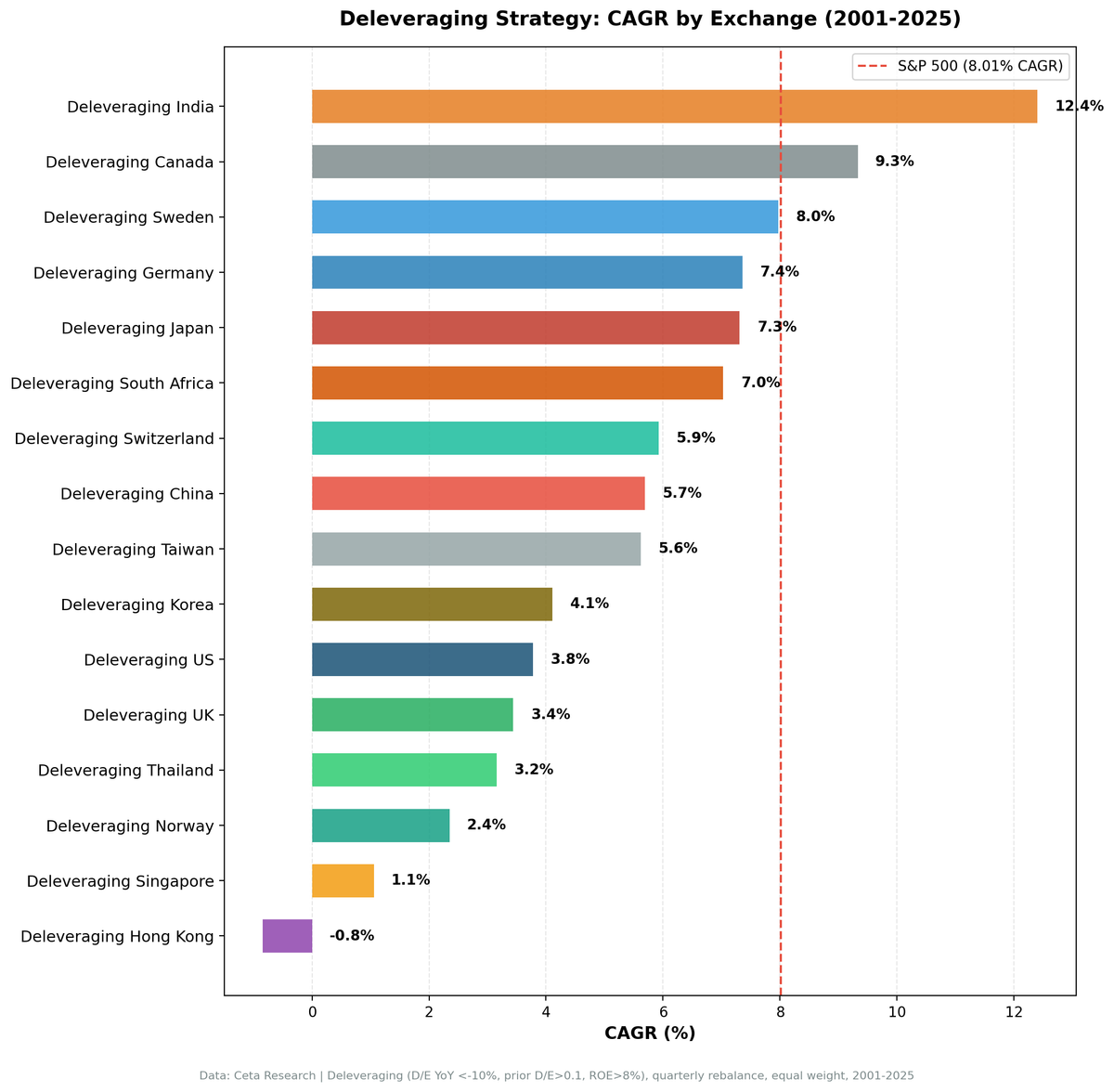

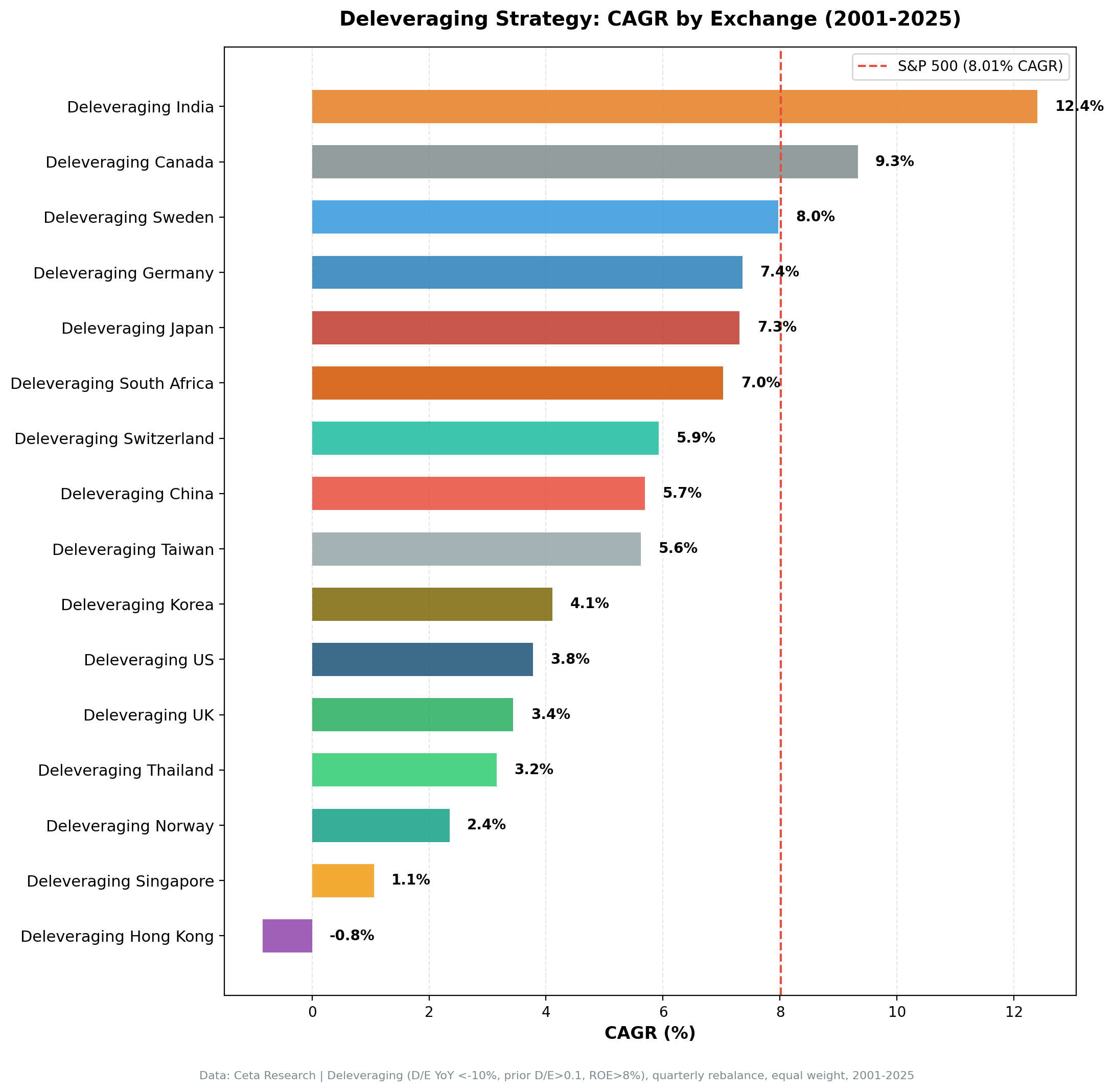

Full Results: 13 Exchanges (2001-2025)

| Exchange | CAGR | Excess vs SPY | Sharpe | MaxDD | Cash% | Avg Stocks |

|---|---|---|---|---|---|---|

| India (BSE+NSE) | 12.40% | +4.39% | 0.192 | -67.5% | 21% | 23.1 |

| Canada (TSX) | 9.33% | +1.32% | 0.383 | -42.5% | 0% | 24.7 |

| Sweden (STO) | 7.97% | -0.05% | 0.291 | -62.9% | 13% | 22.3 |

| Germany (XETRA) | 7.36% | -0.65% | 0.226 | -59.4% | 0% | 19.1 |

| Japan (JPX) | 7.31% | -0.70% | 0.321 | -60.0% | 7% | 26.7 |

| Switzerland (SIX) | 5.93% | -2.08% | 0.326 | -50.3% | 0% | 17.4 |

| China (SHZ+SHH) | 5.69% | -2.32% | 0.102 | -64.6% | 0% | 21.2 |

| Taiwan (TAI+TWO) | 5.62% | -2.39% | 0.247 | -56.8% | 24% | 25.8 |

| Korea (KSC) | 4.11% | -3.90% | 0.058 | -49.4% | 28% | 26.1 |

| US (NYSE+NASDAQ+AMEX) | 3.78% | -4.23% | 0.079 | -57.1% | 0% | 24.4 |

| UK (LSE) | 3.44% | -4.57% | -0.003 | -52.2% | 0% | 14.5 |

| Thailand (SET) | 3.16% | -4.85% | 0.029 | -60.3% | 17% | 24.9 |

| Hong Kong (HKSE) | -0.84% | -8.85% | -0.124 | -73.1% | 1% | 19.6 |

SPY benchmark: 8.01% CAGR (2001-2025).

Part of a Series: US | India | Canada

Data: Ceta Research (FMP financial data warehouse). Transaction costs applied. Local currency returns.

The Signal Globally: Works Pre-2013, Breaks After

The clearest pattern across these 13 markets is temporal, not geographic.

Before 2013, the deleveraging signal performed well almost everywhere. Credit tightening cycles made leverage expensive and rewarded companies that reduced it. A company cutting debt while maintaining profitability was genuinely improving its risk-adjusted earnings power, and markets priced that in over 12-24 months.

After 2013, ZIRP and quantitative easing changed the math. When central banks in the US, Europe, and Japan pushed rates toward zero, debt became cheap. Companies that kept leverage high, or even added it, benefited from lower financing costs and could deploy capital into buybacks and acquisitions that inflated returns. Companies that deleveraged were, in many cases, leaving money on the table. The signal flipped from predictive to counter-productive in developed markets.

Two exceptions survived that regime shift: India and Canada. Both for structural reasons that didn't change with ZIRP.

The Outperformers: India and Canada

India: 12.40% CAGR, +4.39% Excess

India's excess return comes with a down capture of 40.7%. When SPY fell in a given quarter, the Indian deleveraging portfolio lost roughly 41 cents for every dollar SPY lost. That asymmetry, strong upside capture, low downside capture, is what you want from a strategy built on financial discipline.

Why does the signal work here? Indian capital markets are less informationally efficient than the US or UK. When an Indian company publishes results showing 10%+ D/E reduction alongside maintained profitability, that information takes time to price fully. The stock continues re-rating for quarters after the filing. In New York or London, the same information is absorbed within days.

Indian companies also carry higher baseline leverage than Western peers, and debt access is more constrained by banking structure and credit availability. A company that cuts its D/E ratio while maintaining ROE above 8% is demonstrating real operational discipline, not just riding a rate cycle. Markets there reward that discipline with a slower, more durable re-rating.

The 21% cash rate (roughly 5 years in cash over the 25-year period) reflects periods where the qualifying universe was too thin. The long-run CAGR holds up despite those gaps. For a dedicated analysis of the India results, see our India Deleveraging backtest post.

Canada: 9.33% CAGR, +1.32% Excess

Canada's outperformance is more modest but structurally different. The TSX is heavily weighted toward resource companies and financials, sectors where balance sheet health gets close scrutiny from both equity and debt investors. A resource company that reduces its D/E ratio during a commodity downturn is signaling operational resilience that the market prices in over time.

Canada's 0% cash rate means the strategy stayed fully invested for the entire period. 24.7 average stocks gives decent diversification. The Sharpe ratio of 0.383 is the best of any market in this analysis, including India. The strategy returned more per unit of volatility in Canada than anywhere else.

The down capture of 48.8% shows capital protection working as intended, the portfolio held up better than SPY during drawdowns, which is the whole premise of a deleveraging strategy.

For a full breakdown of the Canada results, see our Canada Deleveraging backtest post.

The Middle Ground: Sweden, Germany, Japan, Switzerland

These four markets sit within 2.1 percentage points of SPY on an annual basis. The excess returns are negative but not dramatically so.

Sweden (-0.05%): The closest to neutral. 7.97% CAGR, Sharpe 0.291. Technically underperforming, but effectively a draw over 25 years. Sweden has a well-developed corporate governance culture and relatively transparent reporting, the signal captures genuine balance sheet improvement, it just doesn't generate much edge against a liquid domestic benchmark.

Germany (-0.65%): XETRA returned 7.36% with 0% cash and 19.1 average stocks. The Sharpe of 0.226 is acceptable. German industrial companies operate in a culture where conservative financing is standard, so the signal selects from a pool of already-disciplined firms. Some edge, not dramatic.

Japan (-0.70%): JPX returned 7.31% with the best Sharpe of this middle group at 0.321. Japan is interesting because corporate deleveraging has been a structural theme since the early 2000s, companies actively cleaned up post-bubble balance sheets for decades. The signal works partially here, but post-2013 monetary easing (Japan's QE predates and exceeds the US in scale) compressed the edge.

Switzerland (-2.08%): SIX returned 5.93%, the weakest of this subgroup. 17.4 average stocks is thin for a developed market. Switzerland's highly concentrated market, dominated by a handful of mega-caps, means the strategy often runs in a limited universe. The Sharpe of 0.326 is the second-best in this analysis, however, suggesting returns per unit of risk are reasonable even if absolute excess is negative.

The Signal Failures: US, UK, Thailand, Hong Kong

United States: 3.78% CAGR, -4.23% Excess

The US result is the most important failure because it's the most counterintuitive. The world's most liquid market should, in theory, price financial improvement efficiently. It does, but what the screen selects in the US isn't primarily financial improvement.

US companies that deleverage by 10%+ year-over-year are often doing so from distress. Asset sales, equity issuances, forced debt paydowns, these all show up as D/E reduction and all signal a company under pressure, not one gaining strength. The ROE filter catches some of this, but a company can post 10% ROE while still being in a precarious financial position if its equity base is thin.

The down capture of 125.8% confirms the selection problem: the portfolio amplified SPY losses during downturns rather than protecting against them. That's the opposite of what a deleveraging strategy is supposed to do.

UK: 3.44% CAGR, -4.57% Excess

The UK mirrors the US failure almost exactly. The LSE is highly liquid and well-covered, so the signal captures distressed names rather than quality compounders. The Sharpe ratio is -0.003, functionally zero, and the down capture of 81.1% shows partial amplification of losses.

The 14.5 average stocks is also thin for a large developed market, which means idiosyncratic risk is higher and the results less reliable.

Thailand: 3.16% CAGR, -4.85% Excess

Thailand had 17% cash periods and 24.9 average stocks when invested. The -4.85% excess is among the worst in the analysis. Thailand's market structure, many family-controlled conglomerates with opaque financing, means the signal isn't capturing what it intends to capture. A Thai company that reduces its D/E ratio may simply be reclassifying debt or shifting it off-balance-sheet rather than genuinely improving its financial position.

Hong Kong: -0.84% CAGR, -8.85% Excess

Hong Kong is the worst result in the analysis and requires a specific explanation. The -0.84% CAGR over 25 years means the portfolio destroyed value in absolute terms. The down capture of 138.4% means it amplified every major selloff, 2003 SARS, 2008, 2015 China slowdown, 2019-2022 political-COVID-regulatory shocks, more than the benchmark.

The HKSE has unique structural characteristics that break fundamental screens: high concentration of state-linked Chinese enterprises, capital flow dynamics that respond to mainland policy rather than company fundamentals, and liquidity crises that don't correlate with balance sheet quality. A company that looks financially disciplined by annual filing metrics can still blow up on political risk, regulatory intervention, or capital flight.

1% cash despite the terrible results means the universe was always technically qualifying, the problem isn't thin data, it's that the signal picks the wrong names in this market structure.

Exchanges Excluded from This Analysis

Norway (OSL): 53% cash over the full period. A strategy that's uninvested more than half the time isn't generating signal, it's generating noise with occasional data. The Norwegian exchange doesn't produce enough qualifying names consistently for this screen to be valid.

Singapore (SES): Average 9.1 stocks. Below the minimum threshold for diversification and statistical reliability. Results at this universe size are dominated by a handful of individual companies rather than the underlying signal.

South Africa (JNB): 37% cash plus a negative Sharpe. The CAGR of roughly 7% looks fine on paper until you account for South Africa's 9% local risk-free rate. The strategy didn't earn its cost of capital. The resource-heavy JSE universe means qualifying names cluster in commodity companies whose debt cycles are commodity-driven, not operationally driven.

Australia (ASX) and Brazil (SAO): Pre-excluded due to known adjClose split artifacts in the FMP price data warehouse. Return calculations for these exchanges contain errors that make backtest results unreliable.

Check Today's Global Count

How many stocks currently qualify across exchanges? Run the query:

WITH current_fy AS (

SELECT symbol, debtToEquityRatio AS de_current

FROM financial_ratios

WHERE period = 'FY'

AND debtToEquityRatio IS NOT NULL

AND date >= CURRENT_DATE - INTERVAL 18 MONTH

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) = 1

),

prior_fy AS (

SELECT symbol, debtToEquityRatio AS de_prior

FROM financial_ratios

WHERE period = 'FY'

AND debtToEquityRatio IS NOT NULL

AND date >= CURRENT_DATE - INTERVAL 30 MONTH

AND date < CURRENT_DATE - INTERVAL 12 MONTH

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) = 1

),

km AS (

SELECT symbol, returnOnEquityTTM AS roe, marketCap

FROM key_metrics_ttm

)

SELECT

p.exchange,

COUNT(*) AS qualifying_stocks

FROM current_fy c

JOIN prior_fy pr ON c.symbol = pr.symbol

JOIN km k ON c.symbol = k.symbol

JOIN profile p ON c.symbol = p.symbol

WHERE pr.de_prior > 0.1

AND c.de_current >= 0

AND (c.de_current - pr.de_prior) / pr.de_prior < -0.10

AND k.roe > 0.08

GROUP BY p.exchange

ORDER BY qualifying_stocks DESC

Run this query live: cetaresearch.com/data-explorer?q=9X6rtMVU-M

For the current US qualifying stock list: cetaresearch.com/data-explorer?q=jc1D3eHgRx

Why the Regime Explanation Matters

The split between markets that work and markets that don't isn't random. It follows a consistent pattern:

Works where leverage discipline is scarce or structurally meaningful. India: debt is harder to access, and companies that earn the right to reduce it are demonstrating genuine financial progress. Canada: resource sector balance sheets are closely watched by credit markets, and operational improvement is genuinely informative.

Fails where ZIRP made leverage cheap. US, UK, Germany, Japan, Sweden, all benefited from a decade-plus of near-zero rates. In these markets, keeping leverage high wasn't a weakness after 2013, it was a rational response to cheap capital. Companies that aggressively deleveraged often did so defensively, and the strategy selected for defensive posture in a bull market.

Fails where market structure overrides fundamentals. Hong Kong, Thailand, market behavior is driven by factors that annual financial filings don't capture.

This is also a forward-looking consideration. If the interest rate regime shifts back toward tighter credit, rates staying elevated, credit spreads widening, the deleveraging signal could regain predictive power in developed markets. The post-2013 breakdown may not be permanent. But over the full 25-year backtest, the evidence is clear: this isn't a universal factor.

Strategy Limitations

Currency differences. All returns are local currency. India's 12.40% in rupees includes the historical rupee depreciation of 2-4% per year against the dollar. Canada's 9.33% is in CAD. Cross-currency comparisons require adjusting for expected exchange rate trends.

Data availability varies by exchange. Earlier years (2001-2004) have thinner FMP coverage on several exchanges, particularly India. The effective backtest start date with robust data is closer to 2005-2006 for some markets. Returns in the early period may reflect a thinner qualifying universe.

Annual filing frequency. The strategy uses annual fiscal year data with a 45-day lag. For companies that report quarterly, the signal can be 12 months stale by the time the next annual filing arrives. A company can deleverage in one year and re-lever in the next before the screen captures the reversal.

Korea and Taiwan are comparison-only. Korea's 28% cash rate reflects chaebols, the structurally leveraged conglomerates that dominate the KSC, consistently failing the D/E reduction filter. Taiwan's 24% cash reflects a similar dynamic in its semiconductor supply chain firms. Both markets have enough invested periods to include in the comparison, but neither meets the threshold for a dedicated strategy recommendation.

China context. China's 5.69% CAGR includes extraordinary years: +155% in 2007 (Shanghai bubble), +104% in 2009. The long-run underperformance (-2.32% vs SPY) is despite those outlier years. This is comparison data, the signal's behavior in Chinese markets is volatile and regime-dependent in ways the simple annual backtest doesn't capture.

What This Tells You

Use the deleveraging signal selectively. It's not a factor that works everywhere, and the markets where it fails don't fail marginally, they fail by 4-9 percentage points annually over 25 years.

If you're building a strategy for India or Canadian equities, D/E reduction combined with an ROE filter is worth including. If you're focused on US, UK, or Hong Kong markets, this signal as defined, without significant additional filters, has consistently selected the wrong names.

The regime dependency also matters for timing. Rates staying higher for longer into the 2025-2030 period could partially restore the signal's power in developed markets. That would need to show up in rolling 5-year performance before it's worth acting on.

Data: Ceta Research (FMP financial data warehouse). Backtest period: 2001-2025. Transaction costs applied. Full methodology at cetaresearch.com.