Revenue Surprise Momentum Across 9 Exchanges: Only the US Has the Data

We ran revenue surprise momentum, buying stocks that beat quarterly analyst revenue estimates, on 9 stock exchanges worldwide from 2000 to 2025. The result was stark: the US outperformed by 2.1% annually. Every other exchange either underperformed or spent most of the backtest holding cash because the signal couldn't fire.

Contents

- Method

- What We Found

- US only.

- Max Drawdowns

- The Data Availability Problem

- Why is the US different?

- India: 45% Cash but Positive Excess

- Germany: 0% Cash, Severe Drawdown

- What This Means

- Individual Exchange Posts

- References

The reason isn't that revenue surprise doesn't work internationally. It's that the data doesn't exist.

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Period: 2000–2025 (25 years, 103 quarterly periods)

- Rebalancing: Quarterly (January, April, July, October), equal weight

- Benchmark: S&P 500 Total Return (SPY, in USD)

- Transaction costs: Size-tiered model (0.1–0.5% one-way based on market cap)

- Cash rule: Hold cash if fewer than 10 stocks qualify at a rebalance date

Revenue surprise signal (all filters must pass):

| Filter | Threshold |

|---|---|

| Revenue surprise | 0% < surprise < 50% (beat estimates, exclude outliers) |

| ROE | > 8% |

| Debt/Equity | < 2.5 |

| Market cap | Exchange-specific threshold (local currency) |

The strategy requires two data sources joined together: quarterly revenue actuals from income_statement (periods Q1/Q2/Q3/Q4) and quarterly analyst consensus estimates from analyst_estimates (period='quarter'). This join is where most international markets fall apart.

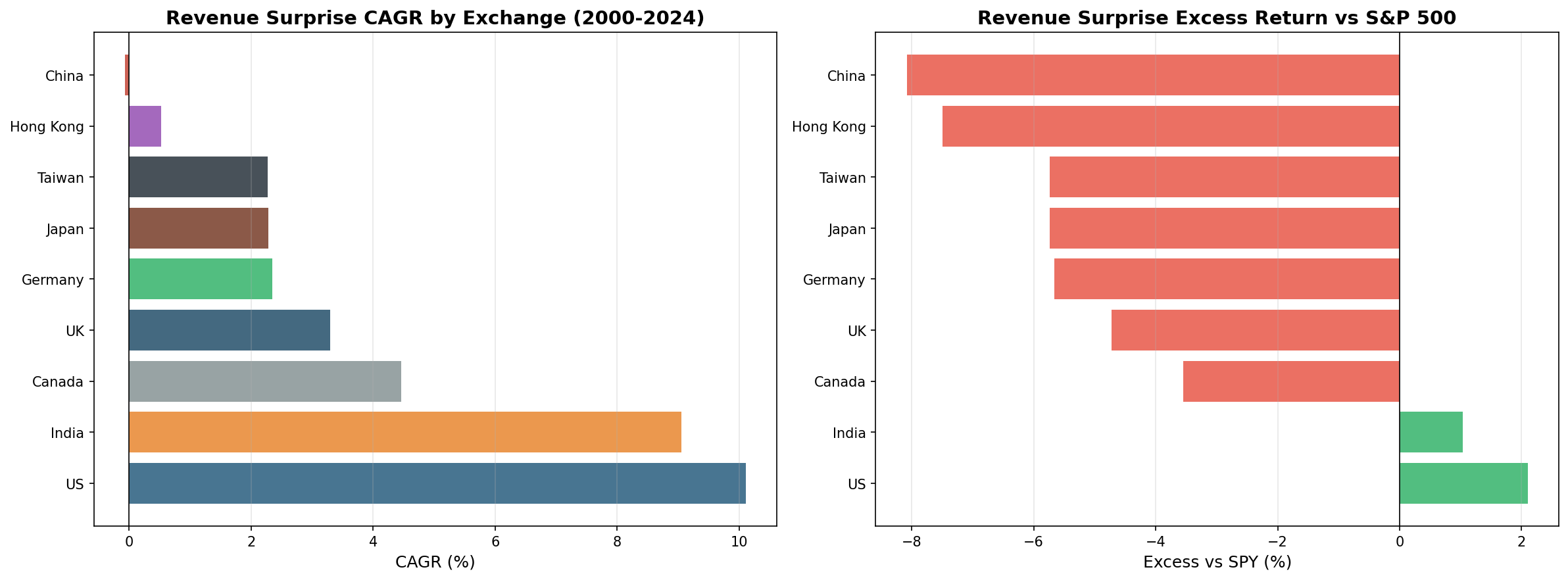

What We Found

US only.

| Exchange | CAGR | vs SPY | Sharpe | Cash % | Avg Stocks |

|---|---|---|---|---|---|

| US (NYSE+NASDAQ+AMEX) | 10.11% | +2.10% | 0.376 | 0% | 29.3 |

| India (BSE+NSE) | 9.05% | +1.03% | 0.133 | 45% | 29.4 |

| Canada (TSX) | 4.46% | -3.55% | 0.110 | 12% | 29.2 |

| UK (LSE) | 3.29% | -4.72% | -0.012 | 45% | 16.1 |

| Germany (XETRA) | 2.35% | -5.66% | 0.018 | 0% | 22.2 |

| Japan (JPX) | 2.28% | -5.74% | 0.246 | 75% | 25.9 |

| Taiwan (TAI+TWO) | 2.27% | -5.74% | 0.128 | 75% | 30.0 |

| Hong Kong (HKSE) | 0.52% | -7.49% | -0.137 | 42% | 27.1 |

| China (SHZ+SHH) | -0.07% | -8.08% | -0.256 | 75% | 30.0 |

SPY benchmark: 8.01% CAGR, Sharpe 0.354

Every exchange except the US underperforms SPY. Many of those underperformances are misleading, they come with 40–75% cash periods, meaning the strategy wasn't really running for most of the test.

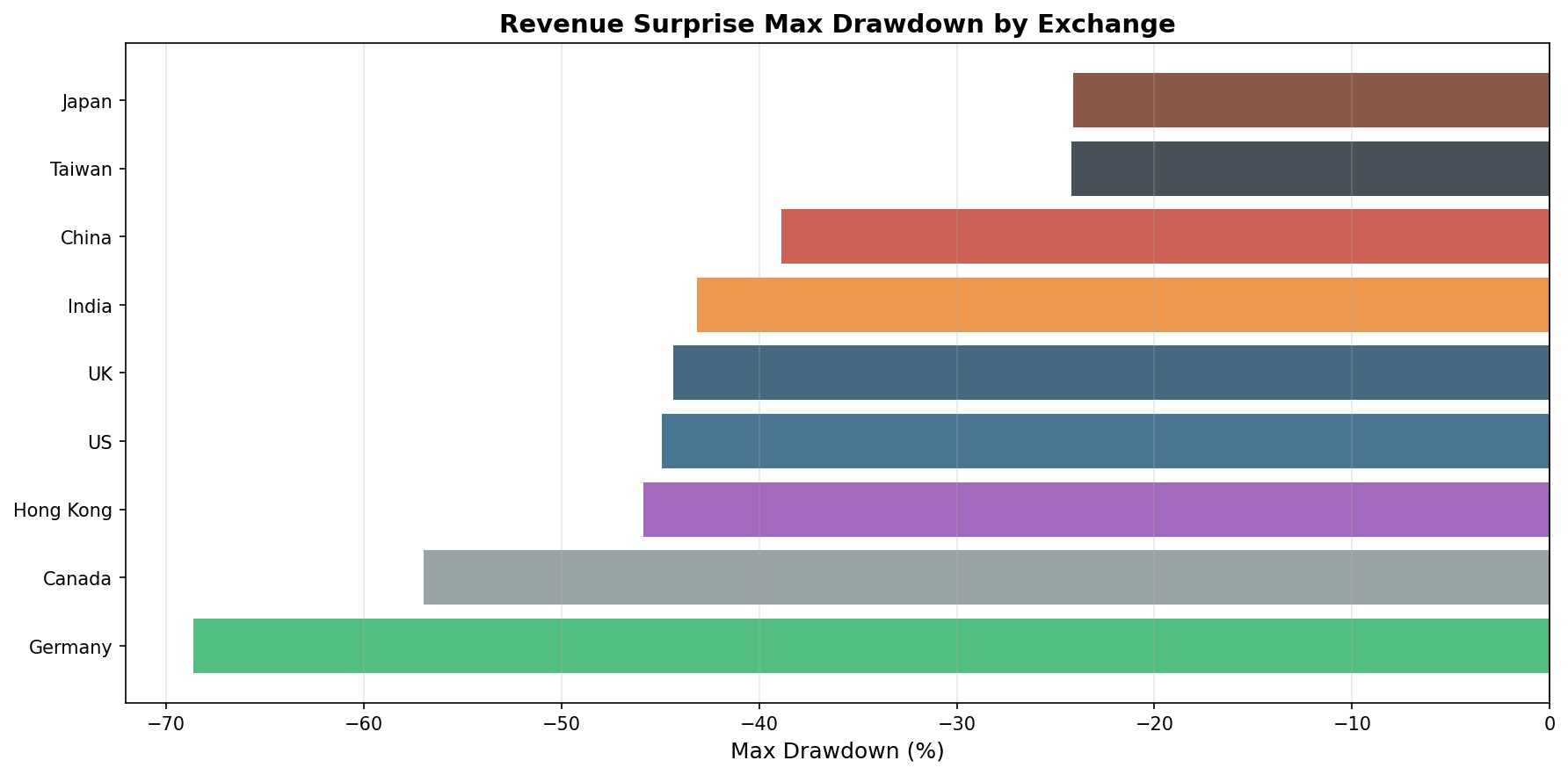

Max Drawdowns

| Exchange | Max Drawdown | Invested % |

|---|---|---|

| Germany (XETRA) | -68.62% | 100% |

| Canada (TSX) | -56.96% | 88% |

| Hong Kong (HKSE) | -45.87% | 58% |

| US (NYSE+NASDAQ+AMEX) | -44.90% | 100% |

| UK (LSE) | -44.36% | 55% |

| India (BSE+NSE) | -43.15% | 55% |

| China (SHZ+SHH) | -38.89% | 25% |

| Taiwan (TAI+TWO) | -24.22% | 25% |

| Japan (JPX) | -24.11% | 25% |

Japan and Taiwan show shallow max drawdowns (-24%) but that's because the portfolio held cash for 75% of the period. When the signal did fire, those positions lost money, but not often enough to produce a large drawdown number.

Germany's -68.62% is the most concerning result for a fully-invested exchange. With 0% cash and an average of 22 stocks, bad quarters in 2001-2003 and 2008-2009 on a concentrated portfolio drove severe losses. The signal fired, but the selected stocks were mid-cap names that fell harder than broad indices in bear markets.

The Data Availability Problem

The core issue for non-US exchanges isn't strategy design. It's the data pipeline.

Revenue surprise requires quarterly analyst consensus revenue estimates, not annual estimates, not forward guidance, but backward-looking consensus estimates for each fiscal quarter. In the US, this data exists comprehensively from the early 1990s onward. Thousands of US-listed companies have quarterly revenue estimates on record from Wall Street consensus databases.

For international markets, this coverage is thin at best, absent at worst:

| Exchange | Coverage Start | Cash % | Root Cause |

|---|---|---|---|

| US (NYSE+NASDAQ+AMEX) | 1992+ | 0% | Full historical quarterly estimates |

| Canada (TSX) | ~2000 | 12% | Partial quarterly coverage, gaps early years |

| India (BSE+NSE) | ~2005 (patchy) | 45% | Quarterly estimates sparse before 2015 |

| UK (LSE) | ~2005 | 45% | Annual estimates dominant, quarterly patchy |

| Hong Kong (HKSE) | ~2005 | 42% | Limited mid-cap coverage |

| Germany (XETRA) | ~2000 | 0% | Coverage exists but mid-cap gaps |

| Japan (JPX) | ~2011 | 75% | Semi-annual reporting, limited quarterly coverage |

| Taiwan (TAI+TWO) | ~2011 | 75% | Same as Japan |

| China (SHZ+SHH) | ~2010 | 75% | Forward-looking estimates only, limited backfill |

Japan, Taiwan, and China spend 75% of the test in cash. This means the signal, matching quarterly actuals against quarterly consensus, simply couldn't fire in most quarters. There weren't enough matching records to build a 10-stock minimum portfolio.

The 25% of invested periods for these exchanges aren't random. They cluster in recent years (2015–2025) as analyst coverage expanded. So the backtest results for Japan, Taiwan, and China reflect roughly 6 years of invested strategy performance, not 25.

Why is the US different?

Wall Street's analyst industry has tracked quarterly revenue consensus for US-listed companies for decades. Bloomberg, I/B/E/S (now Refinitiv), FactSet, and similar services collected and standardized this data as a core product. By 2000, thousands of US stocks had consistent quarterly revenue estimates on record.

International analysts traditionally published annual earnings models, a single year-end EPS estimate, rather than quarter-by-quarter revenue breakdowns. This was a cultural and workflow artifact of how international equity research developed. The shift to quarterly consensus coverage for international stocks happened gradually through the 2010s and is still incomplete for many mid-cap and small-cap names.

India: 45% Cash but Positive Excess

India is the one market outside the US where the signal shows potential. The excess CAGR was +1.03% (9.05% vs 8.01% SPY benchmark). But with 45% cash periods, the strategy was only invested in 57 of 103 quarters, roughly from 2005 onward as analyst estimate coverage improved.

The invested periods show meaningful outperformance, suggesting the revenue surprise mechanism works when the data is there. India's large domestic retail investor base and historically thinner institutional coverage may allow the signal to persist longer than in the US before being arbitraged away.

Interpreting India's result requires honesty: 45% cash means roughly half the backtest isn't testing the strategy. The data isn't sufficient for a robust conclusion.

Germany: 0% Cash, Severe Drawdown

Germany (XETRA) is the other fully-invested exchange. It shows 0% cash periods, enough qualifying stocks every quarter. But the results were weak (2.35% CAGR, -5.66% vs SPY) with a severe maximum drawdown of -68.62%.

This drawdown is plausible given the portfolio characteristics: 22 average stocks, mid-cap bias, concentrated in companies with positive revenue surprises that still declined in the 2001-2003 and 2008-2009 bear markets. German mid-caps are more volatile than the German index (DAX is large-cap weighted). But -68.62% over 25 years vs -45.5% for SPY is a significant risk premium for no return premium.

Germany's result falls in the "signal exists but no edge" category. The revenue surprise criterion fires consistently, but German mid-caps beating their quarterly revenue estimates don't systematically outperform over the subsequent quarter.

What This Means

Revenue surprise momentum is a US-specific strategy. The reason to run it globally isn't to generate alpha internationally, it's to check whether the signal is universal. It's not, and the data availability gap explains most of why.

For investors operating in US equities: the signal works. 2.1% excess CAGR over 25 years with favorable up/down capture asymmetry is real.

For investors in other markets: the more relevant question is whether quarterly analyst consensus revenue estimates exist in sufficient depth for your target market. If your broker or data provider doesn't have comprehensive quarterly revenue estimates going back 10+ years, the signal won't work, not because the behavior doesn't exist, but because you can't measure it.

The strategy won't improve meaningfully for international markets until analyst estimate coverage improves. This is a data infrastructure problem, not a strategy design problem.

Run the US revenue surprise screen on Ceta Research

Individual Exchange Posts

- Revenue Surprise Momentum: US Results, 10.11% CAGR, +2.1% excess, 25 years fully invested

References

- Jegadeesh, N. & Livnat, J. (2006). "Revenue Surprises and Stock Returns." Journal of Accounting and Economics, 41(1–2), 147–166.

- Bushee, B. & Raedy, J. (2006). "Factors Affecting the Implementability of Stock Market Trading Strategies." Working Paper, University of Pennsylvania. (Context: data availability constraints on implementability)

- Griffin, J., Ji, X. & Martin, S. (2003). "Momentum Investing and Business Cycle Risk: Evidence from Pole to Pole." Journal of Finance, 58(6), 2515–2547. (Cross-market momentum analysis)

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse. 9 exchanges, quarterly rebalance, equal weight, transaction costs included, 2000–2025. Returns in local currency vs SPY USD benchmark.