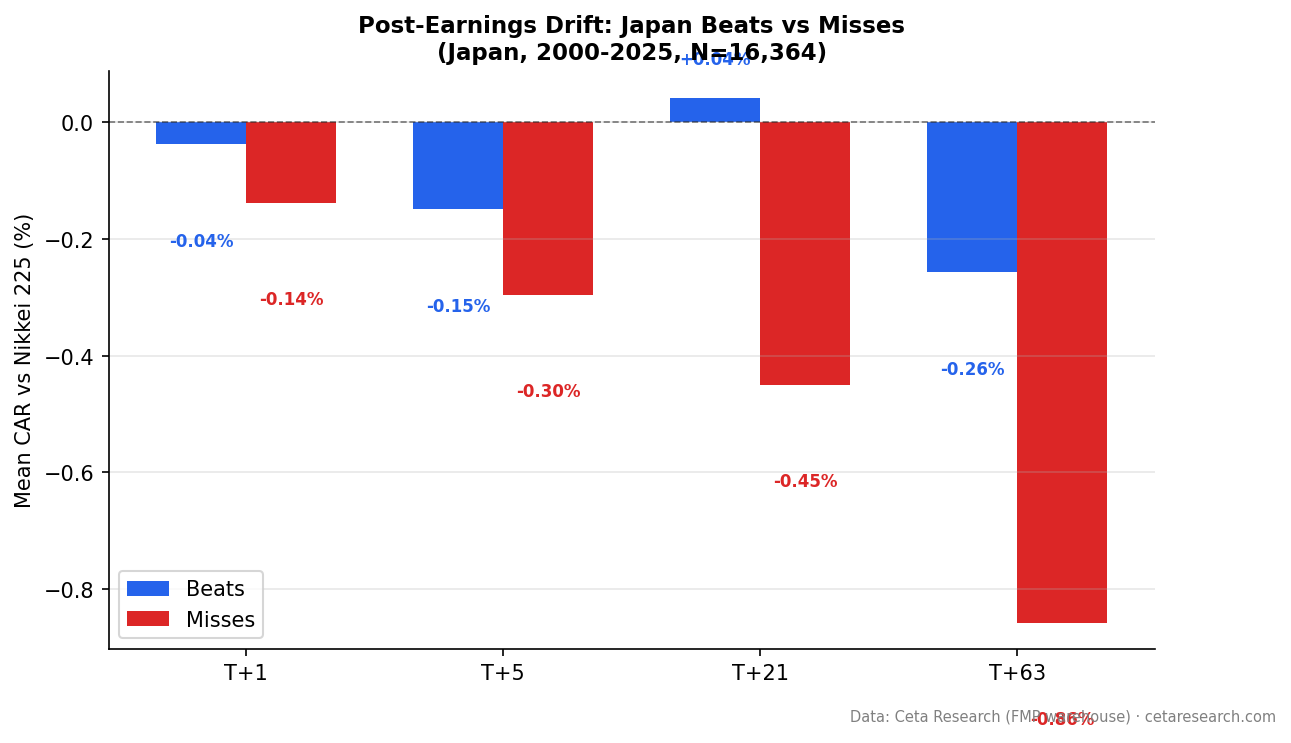

Post-Earnings Drift in Japan: The Miss Signal Is What Survives

With MOC entry and the Nikkei as benchmark, Japan's beat drift vanishes (-0.26%, not significant). Misses still decline -0.86% (t=-5.35). Q5-Q1: +1.20pp. The relative signal survives, but the tradeable edge is miss-avoidance.

Japan's PEAD signal is primarily a miss-avoidance signal, not a beat-chasing signal.

Contents

We analyzed 16,364 earnings events on JPX between 2000 and 2025, using next-day close entry and the Nikkei 225 as benchmark. Beats drifted -0.26% vs the Nikkei at T+63 (not significant). Misses fell -0.86% (t=-5.35, significant). With realistic execution, the beat drift that appeared in earlier studies (using EWJ as benchmark and same-day entry) disappears. What remains is the miss-side signal.

The Q5-Q1 spread is +1.20 percentage points, confirming the relative signal. But the absolute drift for beats has vanished.

The Strategy

Same event-study methodology as the global PEAD analysis. We measure Cumulative Abnormal Return (CAR) at T+1, T+5, T+21, and T+63 trading days, benchmarked against the Nikkei 225.

Signal: Surprise = (epsActual - epsEstimated) / |epsEstimated|

Parameters:

- Universe: JPX, market cap > ¥100B (historical FY key_metrics)

- Period: 2000-2025 (16,364 events: 9,318 beats, 7,046 misses)

- Benchmark: Nikkei 225 (^N225, local currency)

- Execution: Next-day close (MOC)

- Surprise cap: |surprise| <= 200%

- Winsorized means: 1st/99th percentile

- Event windows: T+1, T+5, T+21, T+63 trading days

Note on data density: JPX data in the FMP warehouse is most complete from approximately 2013 onward. The effective study window for high-confidence results is roughly 12 years, not 25. Event counts are still substantial (17,379 total), but the earlier years carry less weight.

Data: Ceta Research (FMP financial data warehouse), earnings_surprises table.

Screen for current JPX earnings surprises:

SELECT es.symbol,

CAST(es.date AS DATE) AS event_date,

es.epsActual AS actual_eps,

es.epsEstimated AS est_eps,

ROUND((es.epsActual - es.epsEstimated)

/ ABS(NULLIF(es.epsEstimated, 0)) * 100, 1) AS surprise_pct

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE p.exchange IN ('JPX')

AND CAST(es.date AS DATE) >= CURRENT_DATE - INTERVAL '30' DAY

AND es.epsEstimated IS NOT NULL

AND ABS(es.epsEstimated) > 0.01

AND es.epsActual > es.epsEstimated

ORDER BY surprise_pct DESC

LIMIT 30

What We Found

Misses underperform. Beats are flat.

With next-day close entry and the Nikkei as benchmark:

| Category | T+1 | T+5 | T+21 | T+63 |

|---|---|---|---|---|

| Beats (9,318 events) | -0.04% | -0.15% | +0.04% | -0.26% |

| Misses (7,046 events) | -0.14% | -0.30% | -0.45% | -0.86% |

Beats hover around zero at every window. There's no positive post-entry drift for Japanese earnings beats vs the Nikkei. The +1.84% reported in earlier versions of this study (using the EWJ ETF and same-day entry) was primarily the announcement-day reaction plus USD/JPY currency effects in the benchmark.

Misses drift persistently lower. The -0.86% at T+63 is significant (t=-5.35). Beat hit rate: 47.1%. Miss hit rate: 46.3%.

The quintile structure is monotonic and wide.

| Quintile | Surprise Range | CAR at T+63 |

|---|---|---|

| Q1 (worst misses) | -199.4% to -22.4% | -0.85% |

| Q2 | -22.4% to -1.9% | -0.74% |

| Q3 | -1.9% to 11.3% | -1.00% |

| Q4 | 11.3% to 35.6% | -0.39% |

| Q5 (biggest beats) | 35.6% to 200% | +0.35% |

All quintiles except Q5 are negative. The Q5-Q1 spread is +1.20 percentage points. Q5 barely produces positive drift at +0.35%. The signal is a gradient, not a strong absolute return at the top. Q3 at -1.00% is an anomaly worth noting. The relative ordering is mostly monotonic, but the absolute numbers don't support a long-only beat-chasing strategy.

Japan vs Asia

With MOC execution and local benchmarks, the comparison to other Asian markets shows a different picture than earlier versions of this study.

India has the strongest beat drift globally (+2.89% vs Sensex at T+63). Misses decline -0.44%. India is the one market where post-entry beat drift is clearly large enough to be tradeable.

China (SHZ+SHH) shows beat drift of +1.78% vs SSE Composite at T+63. Misses actually drift positive (+0.74%), suggesting strong market-wide momentum.

Japan sits with the developed markets now. Beats are flat (-0.26%). Misses decline (-0.86%). The signal is primarily a miss-avoidance signal, not a beat-chasing signal.

| Market | Beats T+63 | Misses T+63 | Benchmark |

|---|---|---|---|

| India | +2.89% | -0.44% | Sensex |

| China | +1.78% | +0.74% | SSE Composite |

| Japan | -0.26% | -0.86% | Nikkei 225 |

| US | -0.40% | -0.95% | SPY |

| Canada | +1.13% | -0.34% | TSX Composite |

Japan's earlier appearance as a strong two-sided signal (beats +1.84%, misses -1.38% vs EWJ) was amplified by the announcement-day reaction and by using a USD-denominated ETF as benchmark. With the Nikkei as benchmark and MOC entry, Japan's PEAD profile is closer to the US than to India or China.

Limitations

Effective history. FMP coverage for JPX grows substantially from 2013 onward. Results spanning the full 2000-2025 label reflect more of a 12-year effective study than a 25-year one. The 17,379 event count is real, but the distribution is skewed toward recent years.

MOC execution. Entering at next-day close removes the announcement-day reaction. This is the earliest realistic entry point, but removes the largest component of PEAD as traditionally measured.

Nikkei as benchmark. The Nikkei 225 is a price-weighted index of Japan's largest companies. Using it as benchmark is more appropriate than EWJ (which introduces USD/JPY currency effects), but the price-weighted methodology may not perfectly represent a cap-weighted universe.

Currency effects. All returns are computed in local currency (JPY). For US investors, JPY/USD fluctuations change actual realized returns. Japan has had significant yen depreciation over parts of this period.

Structural breaks. Japan's equity market has changed significantly since the Bank of Japan's ETF purchase programs began in 2013. Central bank buying of equity ETFs creates a price support mechanism that may alter drift patterns in ways that aren't captured by a uniform analysis.

Transaction costs. Japanese equity markets have tight bid-ask spreads for large-caps but meaningful friction for smaller names. The ¥100B threshold filters out the thinnest markets, but execution costs still reduce net capture.

Takeaway

Japan's PEAD signal with MOC execution and Nikkei benchmark is a miss-avoidance signal, not a beat-chasing signal. Beats drift -0.26% at T+63 (not significant). Misses drift -0.86% (t=-5.35). The Q5-Q1 spread of +1.20pp confirms the relative signal survives.

This puts Japan in the developed-market camp alongside the US (beats -0.40%) and Korea (beats -0.20%), where the announcement-day reaction captures nearly all the beat-side PEAD. For investors in JPX, the implementable signal is avoiding the worst-miss quintile rather than chasing beats.

For tradeable beat-side PEAD, look to India (+2.89% vs Sensex) or Hong Kong (+2.79% vs Hang Seng), where post-entry drift is meaningful.

Data: Ceta Research (FMP financial data warehouse). 16,364 events, JPX, 2000-2025. MOC execution (next-day close entry). Abnormal returns computed vs Nikkei 225. 1st/99th percentile winsorization. Surprise cap 200%. Past performance does not guarantee future results. Educational content only, not investment advice.

References

- Ball, R. & Brown, P. (1968). "An Empirical Evaluation of Accounting Income Numbers." Journal of Accounting Research, 6(2), 159-178.

- Bernard, V. & Thomas, J. (1989). "Post-Earnings-Announcement Drift: Delayed Price Response or Risk Premium?" Journal of Accounting Research, 27(Supplement), 1-36.

- Bernard, V. & Thomas, J. (1990). "Evidence that Stock Prices Do Not Fully Reflect the Implications of Current Earnings for Future Earnings." Journal of Accounting and Economics, 13(4), 305-340.