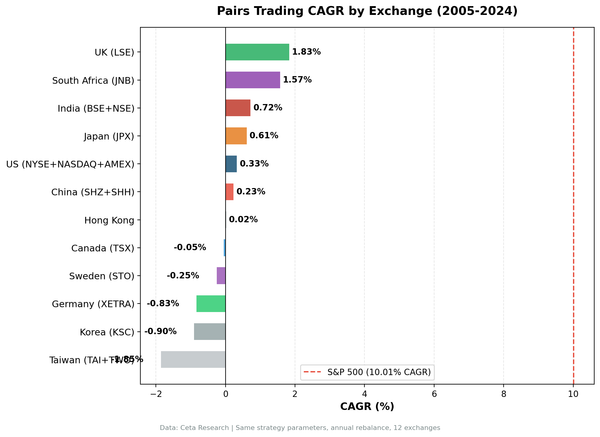

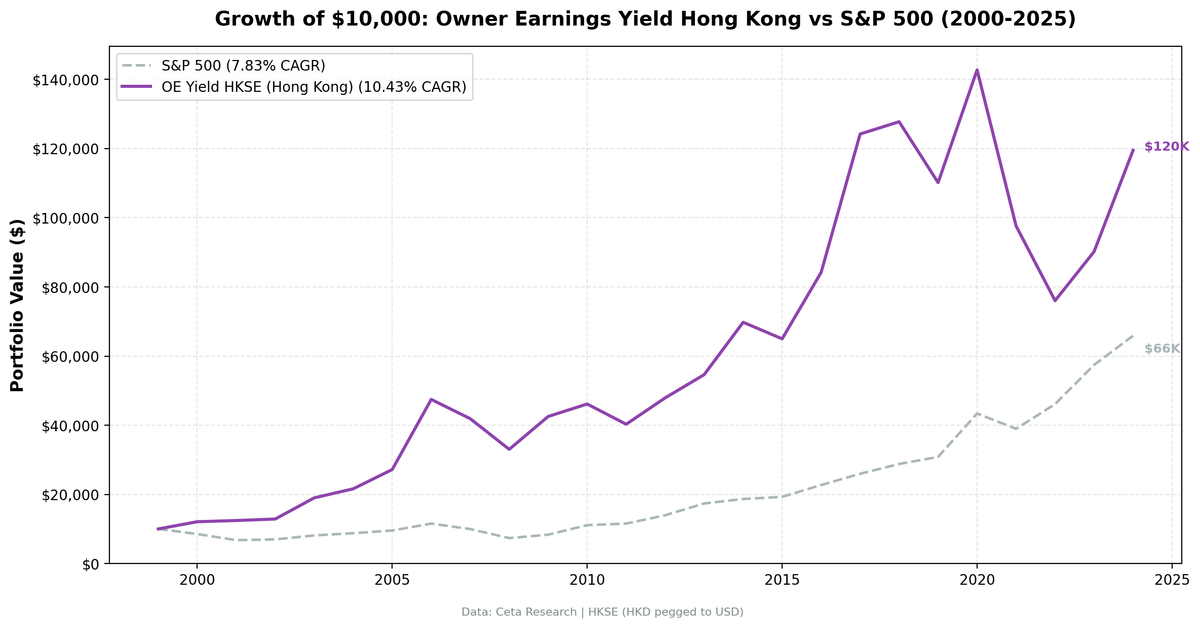

Owner Earnings Yield on Hong Kong Stocks: 10.4% CAGR With Zero Cash Periods

Owner Earnings Yield returned 10.44% annually on HKSE-listed stocks from 2000 to 2025. That's +8.8% excess CAGR over the Hang Seng Index, which managed only 1.64% annually over the same period. Zero cash periods across all 25 years. The screen always found at least 26 qualifying stocks. Hong Kong is one of the few markets where this strategy was fully invested every single rebalance.

Contents

- Method

- The Screen (SQL)

- What We Found

- 25 years of data. +8.8% annual excess over the Hang Seng.

- Year-by-Year Returns

- Key Observations

- Zero cash periods. Always fully invested.

- 2000-2006: The golden stretch

- The HKD-USD peg: Clean currency, clean benchmark

- 2021-2022: The structural break

- Pre-2018 vs post-2018

- 2024: Signs of recovery

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- Run This Screen Yourself

Method

Signal: OE Yield 5-50%, ROE > 10%, Operating Margin > 10%, Market Cap > HK$2B (~$256M USD) Portfolio: Top 30 by OE Yield, equal weight. Annual rebalance (July). Cash rule: Hold cash if fewer than 10 stocks qualify. Period: 2000-2025 (25 annual periods) Benchmark: Hang Seng Index (^HSI) Execution: Next-day close (market-on-close after signal date)

Owner Earnings = Net Income + D&A - min(|Capex|, D&A). The min() function proxies maintenance capex. For full methodology and the rationale behind this metric, see the US flagship post.

The Screen (SQL)

WITH income_latest AS (

SELECT symbol, netIncome, depreciationAndAmortization,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) AS rn

FROM income_statement

WHERE period = 'FY'

AND netIncome IS NOT NULL

AND depreciationAndAmortization IS NOT NULL

),

cashflow_latest AS (

SELECT symbol, capitalExpenditure,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) AS rn

FROM cash_flow_statement

WHERE period = 'FY'

AND capitalExpenditure IS NOT NULL

),

calculated AS (

SELECT

i.symbol,

i.netIncome + i.depreciationAndAmortization

- LEAST(ABS(c.capitalExpenditure), i.depreciationAndAmortization)

AS owner_earnings

FROM income_latest i

JOIN cashflow_latest c ON i.symbol = c.symbol AND c.rn = 1

WHERE i.rn = 1

)

SELECT

calc.symbol,

p.companyName,

ROUND(calc.owner_earnings / k.marketCap * 100, 2) AS oe_yield_pct,

ROUND(k.freeCashFlowYieldTTM * 100, 2) AS fcf_yield_pct,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(f.operatingProfitMarginTTM * 100, 1) AS op_margin_pct,

ROUND(k.marketCap / 1e9, 1) AS market_cap_billions

FROM calculated calc

JOIN key_metrics_ttm k ON calc.symbol = k.symbol

JOIN financial_ratios_ttm f ON calc.symbol = f.symbol

JOIN profile p ON calc.symbol = p.symbol

WHERE calc.owner_earnings > 0

AND calc.owner_earnings / k.marketCap > 0.05

AND calc.owner_earnings / k.marketCap < 0.50

AND k.returnOnEquityTTM > 0.10

AND f.operatingProfitMarginTTM > 0.10

AND k.marketCap > 2e9

AND p.exchange = 'HKSE'

ORDER BY calc.owner_earnings / k.marketCap DESC

LIMIT 30

Run this query on Ceta Research

What We Found

25 years of data. +8.8% annual excess over the Hang Seng.

| Metric | OE Yield (HKSE) | Hang Seng |

|---|---|---|

| CAGR | 10.44% | 1.64% |

| Max Drawdown | -46.75% | - |

| Sharpe Ratio | 0.299 | -0.077 |

| Sortino Ratio | 0.650 | -0.114 |

| Win Rate (annual) | 68% | - |

| Alpha | 8.96% | - |

| Beta | 1.115 | - |

| Up Capture | 172.9% | - |

| Down Capture | 47.3% | - |

| Avg Stocks per Period | 26.6 | - |

| Cash Periods | 0 of 25 | - |

The Hang Seng returned just 1.64% annually over 25 years. OE Yield returned 10.44%. That's not a marginal edge. The strategy never sat in cash. Every single year, at least 26 stocks passed the screen. Hong Kong's deep market of profitable, capital-light businesses keeps the pipeline full.

Up capture of 172.9% means the portfolio captured nearly twice the benchmark's gains in rising years. Down capture of 47.3% means it absorbed less than half the losses. That asymmetry, compounded over 25 years, produced +8.8% annual excess.

One caveat: the Sharpe ratio (0.299) is lower than the US version (0.436). Higher volatility pulls the risk-adjusted number down even though the raw CAGR is strong. But compared to the Hang Seng's Sharpe of -0.077, this is a different league.

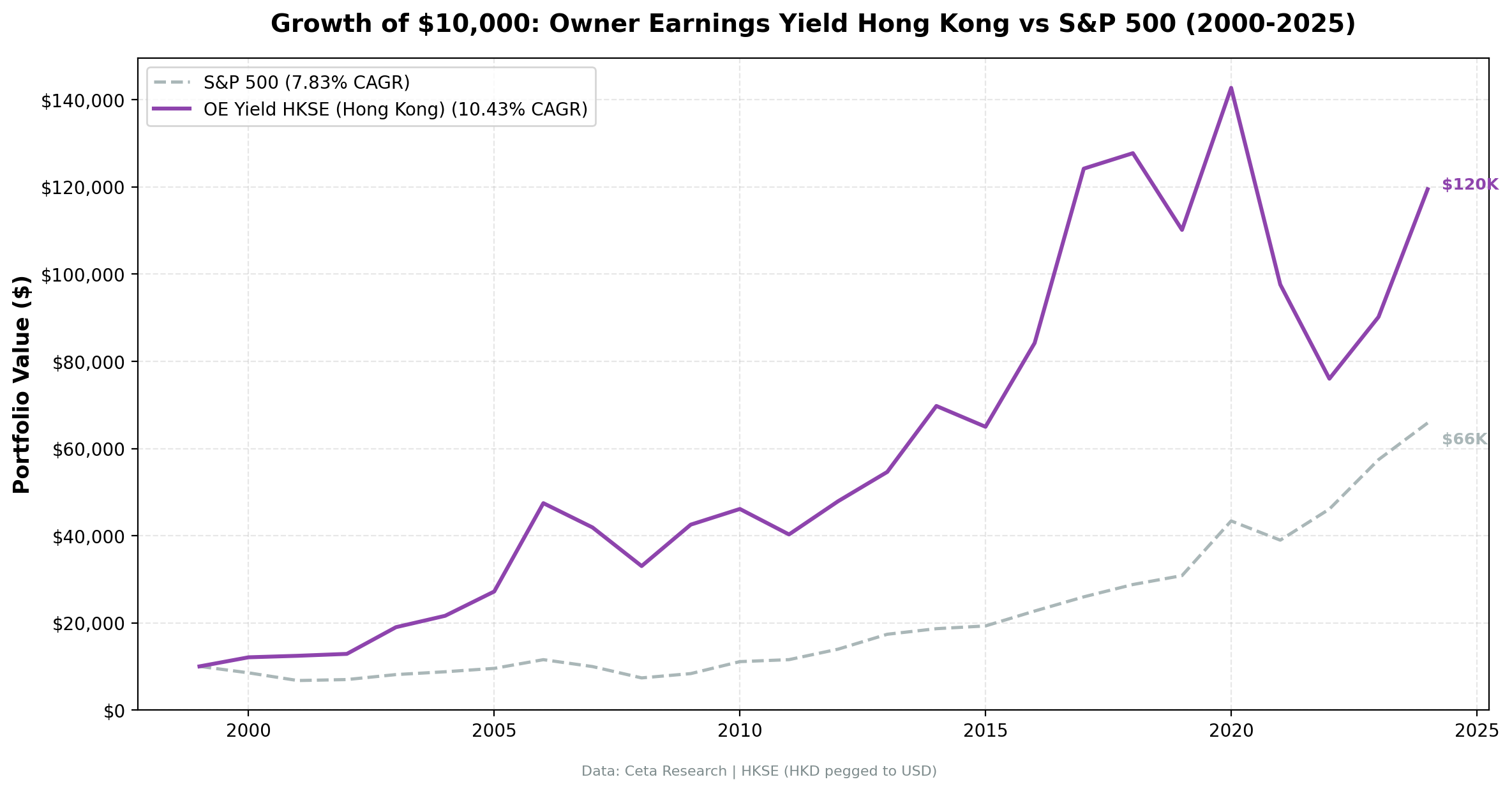

Year-by-Year Returns

| Year | OE Yield (HKSE) | Hang Seng | Excess |

|---|---|---|---|

| 2000 | +20.8% | -18.2% | +39.1% |

| 2001 | +4.8% | -20.4% | +25.2% |

| 2002 | +3.5% | -8.5% | +12.0% |

| 2003 | +46.7% | +27.3% | +19.4% |

| 2004 | +13.8% | +16.0% | -2.2% |

| 2005 | +25.8% | +15.2% | +10.7% |

| 2006 | +74.6% | +35.7% | +38.9% |

| 2007 | -12.6% | -2.0% | -10.6% |

| 2008 | -21.2% | -16.2% | -4.9% |

| 2009 | +28.8% | +9.5% | +19.3% |

| 2010 | +8.5% | +14.4% | -5.9% |

| 2011 | -12.7% | -13.3% | +0.6% |

| 2012 | +18.6% | +4.7% | +13.9% |

| 2013 | +14.0% | +14.0% | +0.0% |

| 2014 | +27.8% | +11.6% | +16.2% |

| 2015 | -6.4% | -19.9% | +13.5% |

| 2016 | +29.6% | +22.4% | +7.1% |

| 2017 | +47.5% | +10.7% | +36.8% |

| 2018 | +2.7% | +1.2% | +1.6% |

| 2019 | -13.8% | -13.0% | -0.8% |

| 2020 | +29.6% | +12.7% | +16.9% |

| 2021 | -31.6% | -22.9% | -8.7% |

| 2022 | -22.1% | -11.6% | -10.6% |

| 2023 | +18.4% | -8.0% | +26.3% |

| 2024 | +32.5% | +36.3% | -3.8% |

Key Observations

Zero cash periods. Always fully invested.

The screen found 26+ qualifying stocks in every single rebalance across 25 years. Hong Kong's exchange is packed with profitable, modestly-valued businesses. Property developers, industrial conglomerates, consumer companies, shipping firms. Many of them carry low debt relative to earnings and generate strong owner earnings. The pipeline never ran dry.

This matters because cash periods are a hidden performance drag. In India, QARP sat in cash for six straight years. In Hong Kong, OE Yield was putting money to work from day one.

2000-2006: The golden stretch

| Year | OE Yield | Hang Seng | Excess |

|---|---|---|---|

| 2000 | +20.8% | -18.2% | +39.1% |

| 2001 | +4.8% | -20.4% | +25.2% |

| 2003 | +46.7% | +27.3% | +19.4% |

| 2006 | +74.6% | +35.7% | +38.9% |

The strategy crushed it during the dot-com bust and kept running through the mid-2000s. 2006 was the best single year at +74.6%, riding China's pre-Olympic investment boom. Capital flooded into Hong Kong as the gateway to mainland China's rapid industrialization. Owner Earnings Yield picked up the cheapest beneficiaries of that flow.

The HKD-USD peg: Clean currency, clean benchmark

Hong Kong pegs its dollar to the US dollar within a narrow band (7.75-7.85 HKD per USD). That peg has held since 1983. Unlike our India or China blogs, there's no currency mismatch to worry about. The strategy's real alpha is measured against the local Hang Seng, which returned just 1.64% CAGR over 25 years. The peg also means these returns translate directly into USD for international investors.

2021-2022: The structural break

| Year | OE Yield | Hang Seng | Excess |

|---|---|---|---|

| 2021 | -31.6% | -22.9% | -8.7% |

| 2022 | -22.1% | -11.6% | -10.6% |

The worst two-year stretch in the backtest. The portfolio lost roughly 47% peak-to-trough across both years. Three forces converged. China's regulatory crackdown on tech and property companies tanked Hong Kong-listed stocks. Political uncertainty after the 2020 National Security Law reduced foreign investor confidence. And capital rotated out of the region entirely.

Even against the Hang Seng, the strategy underperformed in both years. This wasn't just a market-level issue. The OE Yield screen overweighted the sectors hit hardest by regulation and property deleveraging.

Pre-2018 vs post-2018

Splitting the record at 2018 shows the strategy's edge was concentrated early, but still present throughout. Even post-2018, OE Yield beat the Hang Seng in most years. The local index was negative in 4 of the last 7 years. The 25-year CAGR of 10.44% blends a dominant first half with a weaker recent stretch, but the +8.8% annual excess over the Hang Seng held up because the index itself was so poor.

2024: Signs of recovery

The most recent year returned +32.5%, though the Hang Seng actually edged it out at +36.3%. Chinese policy shifted toward economic stimulus in late 2023, and Hong Kong stocks rallied broadly. The Hang Seng's strong 2024 was a rare bright spot for the index. The strategy kept pace but didn't lead, suggesting the rally was market-wide rather than value-driven.

Backtest Methodology

| Parameter | Choice |

|---|---|

| Universe | HKSE, Market Cap > HK$2B (~$256M USD) |

| Signal | OE Yield 5-50%, ROE > 10%, OPM > 10% |

| Portfolio | Top 30 by OE Yield, equal weight |

| Rebalancing | Annual (July) |

| Execution | Next-day close (market-on-close after signal date) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | Hang Seng Index (^HSI) |

| Period | 2000-2025 (25 annual periods) |

| Data | Point-in-time (45-day lag for FY filings) |

| Transaction costs | Size-tiered (0.1-0.5% one-way by market cap) |

Full methodology details: backtests/METHODOLOGY.md

Limitations

Deeper drawdowns than the US. Max drawdown was -46.75% vs -37.2% for the US version. Hong Kong equities are more volatile than US equities during global sell-offs and China-specific events. The 2021-2022 drawdown was driven by political and regulatory risk that no financial screen can filter out.

Post-2018 structural weakness. The strategy underperformed the Hang Seng in 2021 and 2022. Capital outflows from Hong Kong, China regulatory risk, and property deleveraging created extended headwinds. The 25-year record is strong, but the recent stretch includes the worst consecutive losses in the backtest.

Survivorship bias. Exchange membership uses current company profiles. Delisted companies, companies that moved their primary listing away from HKSE, and bankruptcies aren't fully captured in the historical universe.

Concentrated portfolio. 26.6 stocks on average, but all drawn from a single exchange heavily influenced by mainland China policy. Stock-specific and geographic concentration risk is higher than the US version.

Annual rebalancing only. We test July-to-July periods using the most recent FY filing. Quarterly rebalancing with TTM data might produce different results, particularly given Hong Kong's volatile market structure.

Takeaway

OE Yield works on Hong Kong stocks. 10.44% CAGR over 25 years, +8.8% excess over the Hang Seng, with zero cash periods. The screen always found enough qualifying companies.

The asymmetry is clear: 173% up capture, 47% down capture. The portfolio captures nearly twice the benchmark's gains and absorbs less than half its losses. That pattern held for 25 years despite vastly different market regimes. The 68% win rate confirms it: the strategy beat the Hang Seng in 17 of 25 years.

The cost is equally clear. The 2021-2022 drawdown was brutal, and the strategy couldn't avoid it. OE Yield doesn't protect against regime-level risks like regulatory crackdowns or political instability. It selects cheap, profitable businesses. When the entire market reprices downward, cheap profitable businesses go down too.

The broader context matters: the Hang Seng returned just 1.64% CAGR over 25 years. Hong Kong's index has been one of the worst-performing major markets in the world. OE Yield's 10.44% CAGR shows that stock selection can overcome a poor market environment. For investors who believe Hong Kong will remain a viable financial center, this is a strong baseline. For those worried about structural decline, the strategy still beat the local index by a wide margin even in the worst stretch.

Part of a Series

This analysis is part of our Owner Earnings Yield global exchange comparison. We tested the same screen on 13 exchanges worldwide: - OE Yield on US Stocks (NYSE + NASDAQ + AMEX) - 12.3% CAGR, the flagship analysis - OE Yield on Indian Stocks (BSE + NSE) - 17.2% CAGR, +5.1% vs Sensex - OE Yield on Swedish Stocks (STO) - 9.6% CAGR, +7.0% vs OMX Stockholm 30 - OE Yield on Chinese Stocks (SHZ + SHH) - 9.6% CAGR, +7.2% vs SSE Composite - OE Yield: 13-Exchange Global Comparison - full comparison table

Run This Screen Yourself

All metrics used in this analysis (Owner Earnings, ROE, operating margin, market cap) are queryable via SQL on Ceta Research. Filter by exchange (HKSE) and see what passes today.

The full backtest code (Python + DuckDB) is available in our GitHub repository.

Data: Ceta Research, FMP financial data warehouse. Universe: HKSE. Benchmark: Hang Seng Index. Annual rebalance (July), equal weight top 30, 2000-2025. Next-day close execution. Transaction costs included.