We Tested EV/EBITDA Below 10x on 16 Global Exchanges. 4 Beat SPY.

Same signal. Same methodology. 16 different markets. The results aren't uniform, and the pattern tells you something real about where value screens actually work.

Contents

- Method

- Results

- Where It Works: North America and Northern Europe

- The Middle: Italy and Germany

- Where It Struggles: Asia and Emerging Markets

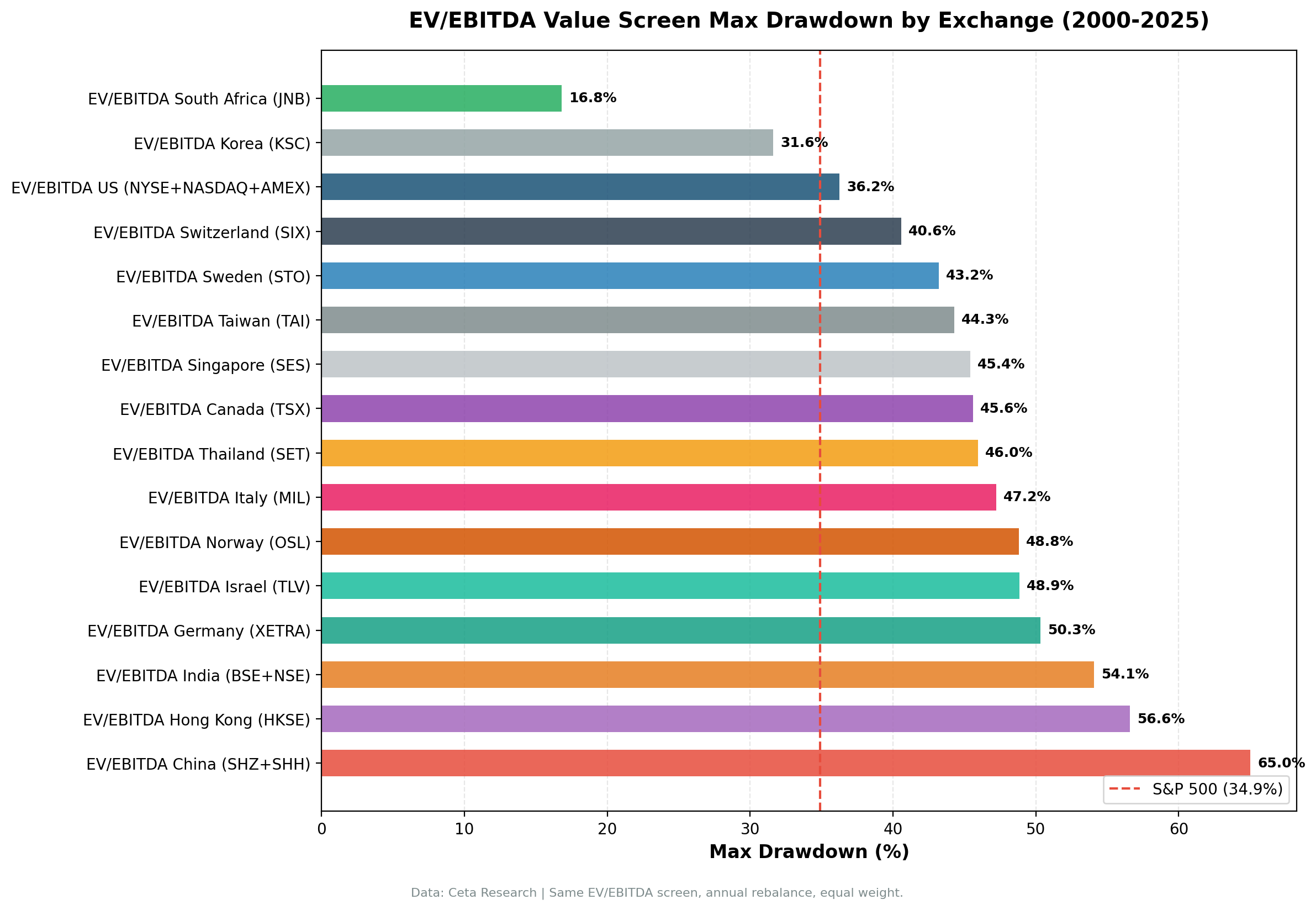

- Max Drawdown Comparison

- Norway: A Special Case

- What Drives the Pattern

- Run It Yourself

- Limitations

The signal is simple: buy companies trading below 10x EV/EBITDA, hold for one year, rebalance annually. We ran this on every major exchange where we have clean FY data going back to 1999. That's 25 years, local currency returns, 25-stock equally-weighted portfolios.

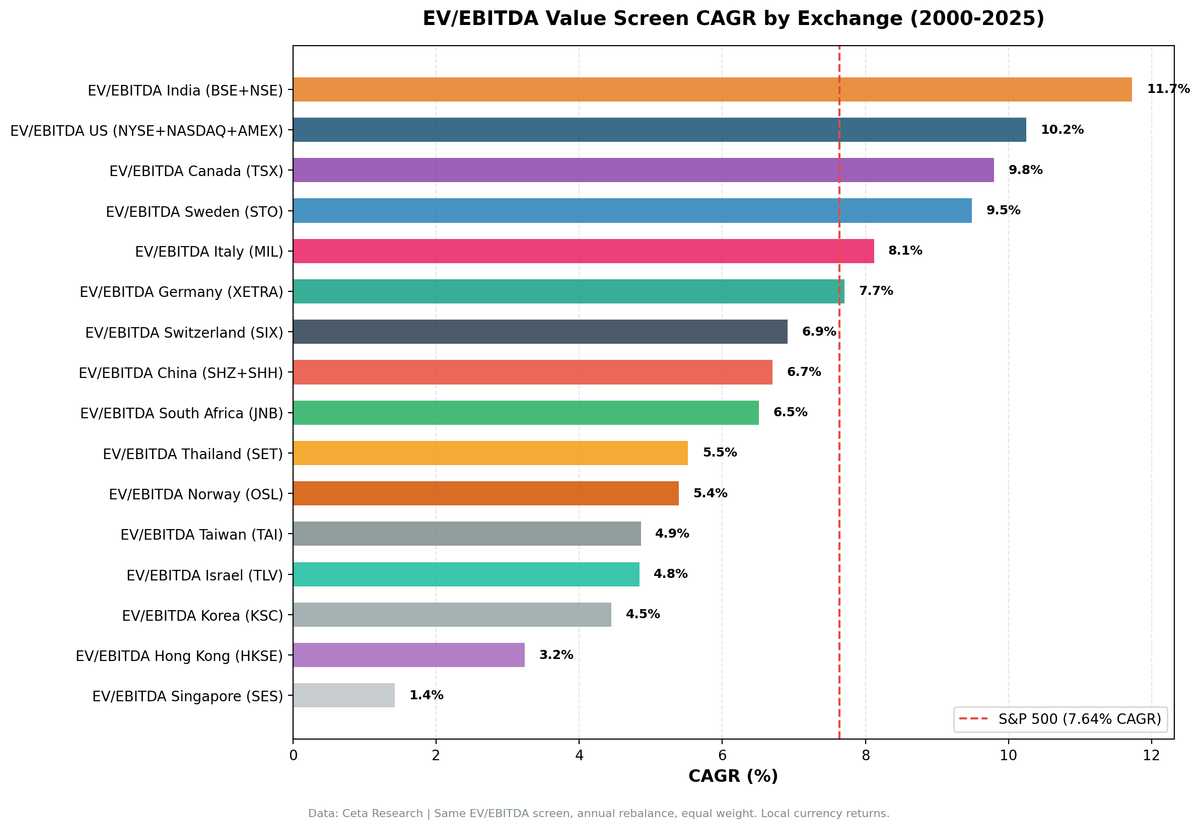

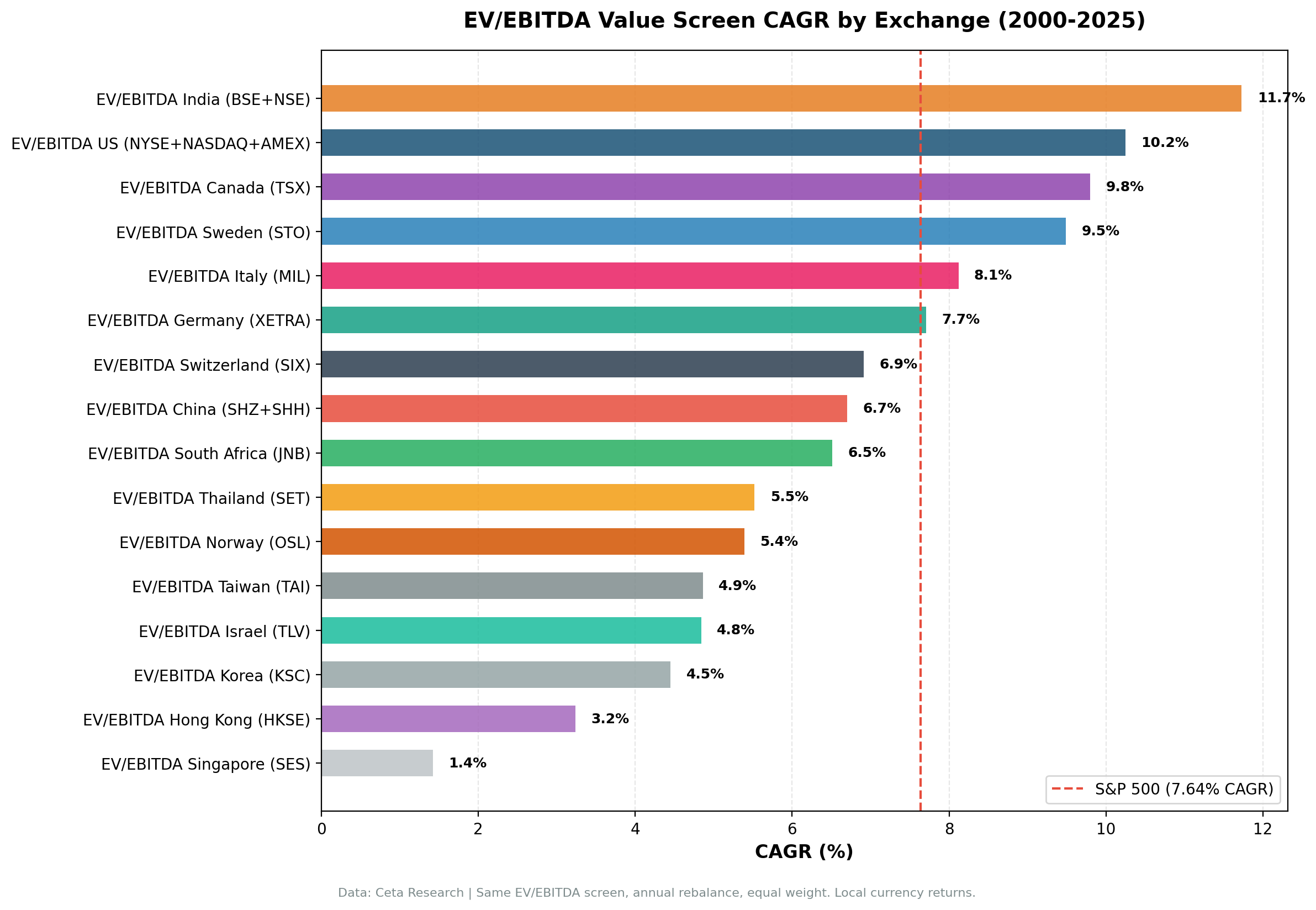

Four exchanges beat SPY's 7.64% CAGR. Twelve don't.

Method

Same screen applied to each exchange independently:

- Signal: EV/EBITDA between 0x and 10x (positive EBITDA required)

- Filter: ROE > 10%, market cap above local threshold (scaled by exchange)

- Portfolio: Top 30 ranked by EV/EBITDA, equal-weight, 25-stock target

- Rebalance: Annual (January)

- Costs: 0.5% round-trip per trade

- Look-ahead bias: 45-day filing lag on all FY data

- Period: 1999-2024 (25 years)

- Benchmark: SPY in USD. Each exchange runs in local currency, so currency effects aren't captured in individual results.

Data source is the FMP fundamental warehouse, same dataset powering the US and individual-exchange analyses.

Results

Full ranked table by CAGR:

| Exchange | CAGR | vs SPY | Sharpe | Max DD | Up-Cap | Dn-Cap | Cash% | Avg Stks | $10k → |

|---|---|---|---|---|---|---|---|---|---|

| India (BSE+NSE) | 11.73% | +4.09% | 0.156 | -54.1% | 143.8% | 57.0% | 20% | 27.2 | $160,122 |

| US (NYSE+NASDAQ+AMEX) | 10.25% | +2.61% | 0.399 | -36.2% | 116.2% | 74.7% | 0% | 21.3 | $114,789 |

| Canada (TSX) | 9.80% | +2.16% | 0.400 | -45.6% | 99.5% | 36.5% | 0% | 26.0 | $103,591 |

| Sweden (STO) | 9.49% | +1.84% | 0.318 | -43.2% | 112.1% | 67.6% | 16% | 26.6 | $96,449 |

| Italy (MIL) | 8.12% | +0.47% | 0.211 | -47.2% | 94.3% | 38.5% | 20% | 18.4 | $70,387 |

| Germany (XETRA) | 7.71% | +0.06% | 0.257 | -50.3% | 107.9% | 95.6% | 0% | 19.2 | $64,009 |

| Switzerland (SIX) | 6.91% | -0.74% | 0.297 | -40.6% | 98.6% | 95.7% | 0% | 14.8 | $53,116 |

| China (SHZ+SHH) | 6.70% | -0.94% | 0.102 | -65.0% | 121.8% | 50.5% | 0% | 21.1 | $50,628 |

| South Africa (JNB) | 6.51% | -1.13% | -0.140 | -16.8% | 66.8% | 24.7% | 24% | 22.7 | $48,422 |

| Thailand (SET) | 5.52% | -2.12% | 0.134 | -46.0% | 85.6% | 84.0% | 20% | 27.4 | $38,348 |

| Norway (OSL) | 5.39% | -2.26% | 0.117 | -48.8% | 58.2% | 5.9% | 52% | 12.2 | $37,110 |

| Taiwan (TAI) | 4.86% | -2.78% | 0.156 | -44.3% | 84.2% | 91.9% | 24% | 27.7 | $32,760 |

| Israel (TLV) | 4.84% | -2.81% | 0.065 | -48.9% | 84.4% | 72.2% | 28% | 21.2 | $32,580 |

| Korea (KSC) | 4.45% | -3.19% | 0.079 | -31.6% | 64.9% | 66.2% | 24% | 26.2 | $29,705 |

| Hong Kong (HKSE) | 3.24% | -4.40% | 0.009 | -56.6% | 82.1% | 107.3% | 4% | 21.0 | $22,197 |

| Singapore (SES) | 1.42% | -6.22% | -0.028 | -45.4% | 50.7% | 82.1% | 24% | 10.9 | $14,237 |

SPY benchmark: 7.64% CAGR, Sharpe 0.322, MaxDD -34.9%, $63,071

Where It Works: North America and Northern Europe

India leads with 11.73% CAGR and +4.09% excess return. The up-capture is 143.8%. when the market rises, this screen captures more of the upside. Down-capture is 57.0%, meaning it loses less in drawdowns. That's an asymmetric profile you rarely see this cleanly. The catch: India's universe is noisy. Some cash periods (5/25 years) suggest the screen gets selective, and small-cap liquidity can be patchy on BSE names.

US is the most reliable result. 10.25% CAGR, Sharpe 0.399 (best in the table), zero cash periods across 25 years. The up-capture of 116.2% with down-capture of 74.7% is consistent with what you'd expect from a value screen: modest participation in bull runs, meaningful protection in bear markets. The 25-year result is driven primarily by the 2000-2012 value era. Post-2013, the screen still beats SPY but by less.

Canada at 9.80% has the best risk-adjusted story after the US. Its down-capture is 36.5%. the screen loses substantially less than the TSX in down years. This is partly explained by market composition: the TSX is heavily weighted toward energy, materials, and financials. Companies in those sectors are naturally valued on EBITDA multiples, so a low EV/EBITDA screen is essentially selecting for cheap commodity and industrial businesses when they're out of favour. That trade works on the TSX.

Sweden at 9.49% shows similar up-capture (112.1%) with reasonable drawdowns. Northern European markets have strong accounting standards and relatively transparent EBITDA reporting, which helps the signal stay clean.

The Middle: Italy and Germany

Italy's 8.12% beats SPY by 0.47 percentage points. Germany's 7.71% beats by 0.06. Both are statistically meaningful 25-year runs but not wide margins.

Italy's down-capture of 38.5% is genuinely good. It's one of the better defensive profiles in the table. The universe is smaller (18.4 avg stocks), which means concentration risk, and cash periods (5/25) indicate the screen gets selective during market stress. Still a real result.

Germany tells a different story. Down-capture of 95.6% means the screen tracks the DAX almost perfectly in bad years. It captures more on the upside (107.9%) but offers almost no drawdown protection. Over 25 years it barely edges SPY, but a German investor running this screen didn't get the defensive buffer the headline CAGR might suggest.

Both markets are informative. They confirm the signal works in developed European markets, just not as cleanly as North America.

Where It Struggles: Asia and Emerging Markets

Hong Kong (3.24%), Singapore (1.42%), Korea (4.45%), Taiwan (4.86%), Israel (4.84%). all underperform SPY, some by a wide margin.

The common thread is structural, not statistical noise. A few factors:

Accounting standards and EBITDA reliability. EV/EBITDA assumes EBITDA is a useful proxy for operating cash generation. In markets where related-party transactions, non-operating items, or aggressive depreciation accounting are more common, EBITDA becomes a less reliable number. Hong Kong and parts of Southeast Asia have a higher rate of these structural issues than the US or Canada.

Corporate governance. Many cheap-looking companies in Korea and Hong Kong are cheap for a reason: family-controlled conglomerates, cross-holdings, or structures where minority shareholders don't participate in value creation. A stock can stay at 5x EV/EBITDA for a long time if the cash never reaches shareholders.

Market composition. Singapore and Hong Kong's exchange-listed companies skew toward financials, real estate investment trusts, and property developers. EV/EBITDA doesn't map cleanly to those sectors. A REIT's "value" is better measured by funds from operations or asset yield, not EBITDA. Applying a broad EV/EBITDA screen to these markets selects disproportionately for sectors where the signal is weak.

Taiwan is somewhat different. its electronics and semiconductor companies are legitimate businesses with real EBITDA. The issue there is that Taiwan's market is cyclical and closely tied to the global semiconductor cycle, not value characteristics. Cheap EV/EBITDA in Taiwan often means you're catching a cyclical downturn, not a mispriced compounder.

Max Drawdown Comparison

A few numbers that need context:

South Africa at -16.8% MaxDD looks like the safest market in the table. It's not. South Africa reports in ZAR, which has experienced significant inflation over the 25-year period. High nominal inflation compresses percentage drawdowns because asset prices recover in nominal terms faster than in low-inflation currencies. A -16.8% MaxDD in ZAR doesn't mean South African equities are less volatile. it means the inflation floor is higher.

China at -65.0% MaxDD is real. This reflects two distinct crashes: the global financial crisis (2008, -65% from peak), and the 2015-2016 circuit-breaker crash where the Shanghai and Shenzhen markets lost roughly 40% in weeks. Chinese equities are volatile in ways that EV/EBITDA screening doesn't mitigate, partly because retail-driven sentiment dominates price action in ways that are disconnected from fundamentals.

Korea at -31.6% stands out as having the best MaxDD in Asia. The screen provides some downside protection there even though it underperforms SPY on CAGR. which suggests the return problem is in weak upside capture (64.9%), not poor risk management.

Norway: A Special Case

Norway shows 5.39% CAGR but the result isn't reliable enough for a real strategy. The screen holds cash 52% of the time. 13 out of 25 years. because the universe at the market cap threshold doesn't generate enough qualifying stocks to fill a 25-stock portfolio.

Oslo Børs is a small exchange dominated by energy, shipping, and salmon aquaculture. When oil prices are low or the energy sector is out of favour, the screen finds almost nothing. When it does find stocks, they're concentrated in one or two sectors, and the volatility reflects that.

The data is shown for completeness. Norway isn't a viable market for running this screen independently.

What Drives the Pattern

Looking at the full table, two factors explain most of the variation in whether EV/EBITDA works:

1. Market composition favouring asset-heavy industries. The screen performs best in markets with large representations of energy, materials, industrials, and financials. These sectors are naturally valued on EBITDA multiples, so screening for low EV/EBITDA selects for businesses the market understands. The US, Canada, India, and Sweden all have substantial allocations to these sectors. Hong Kong, Singapore, and Taiwan skew toward property, financials, and technology, where EV/EBITDA is a weaker signal.

2. Accounting and governance quality. The screen relies on EBITDA being an honest number. In markets with strong regulatory oversight, IFRS or GAAP reporting, and independent audit culture, EBITDA is a reasonable proxy for operating performance. Where those standards are weaker or where related-party transactions are routine, the screen picks up companies that look cheap because their reported EBITDA is unreliable.

Currency effects add noise when comparing against a USD benchmark, but they don't explain the pattern systematically. India and Canada both beat SPY despite having their own currencies. It's the structural market factors, not currency, that matter.

Part of a Series: Global | US | UK | Switzerland | Japan | India | Hong Kong | Germany

Run It Yourself

This query screens globally across all covered exchanges, ranked by EV/EBITDA. No exchange filter. just the cheapest qualifying companies worldwide.

-- Global EV/EBITDA screen: top 30 cheapest qualifying companies worldwide

SELECT

k.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(k.evToEBITDATTM, 2) AS ev_ebitda,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCapTTM / 1e9, 2) AS mktcap_bn

FROM key_metrics_ttm k

JOIN profile p ON k.symbol = p.symbol

WHERE k.evToEBITDATTM > 0

AND k.evToEBITDATTM < 10

AND k.returnOnEquityTTM > 0.10

AND k.marketCapTTM > 1000000000

QUALIFY ROW_NUMBER() OVER (PARTITION BY k.symbol ORDER BY k.evToEBITDATTM ASC) = 1

ORDER BY k.evToEBITDATTM ASC

LIMIT 30;

Run this at cetaresearch.com/data-explorer.

Limitations

Local currency vs USD. All individual exchange results are in local currency. When you invest from a USD base, you take on currency risk that's not reflected in these CAGRs. India's 11.73% in INR looks different after USD/INR depreciation. Canada and Sweden are less affected because their currencies are more stable against the dollar over long periods.

Data coverage quality. Smaller exchanges have thinner coverage in earlier years. Results for markets like Norway and Israel before 2005 are based on fewer companies than later years, which can amplify early returns in either direction.

Survivorship. The FMP database covers active and delisted companies, which reduces but doesn't eliminate survivorship bias. Exchanges with higher delisting rates (China, India) may have more residual survivorship bias than the developed market results.

Market structure changes. Most of these 25-year results span periods where the markets themselves changed materially. China's circuit breaker introduction, India's market reforms, the expansion of South Korea's KOSPI. A strategy that worked in 2001 may face a structurally different market today.

The pattern is real enough to be informative. Four markets beat SPY, twelve don't, and the reasons hold up to scrutiny. That's worth knowing before running this screen internationally.