Low-Concentration Quality Stocks on the JSE: Close to Flat After Execution Correction

South Africa is the only exchange where low-concentration quality stocks beat SPY. 12.09% CAGR vs 10.61% over 2005-2025, with a 0.470 beta and +2.33% alpha. Most of the excess came from 2005-2012. The signal weakened after 2015.

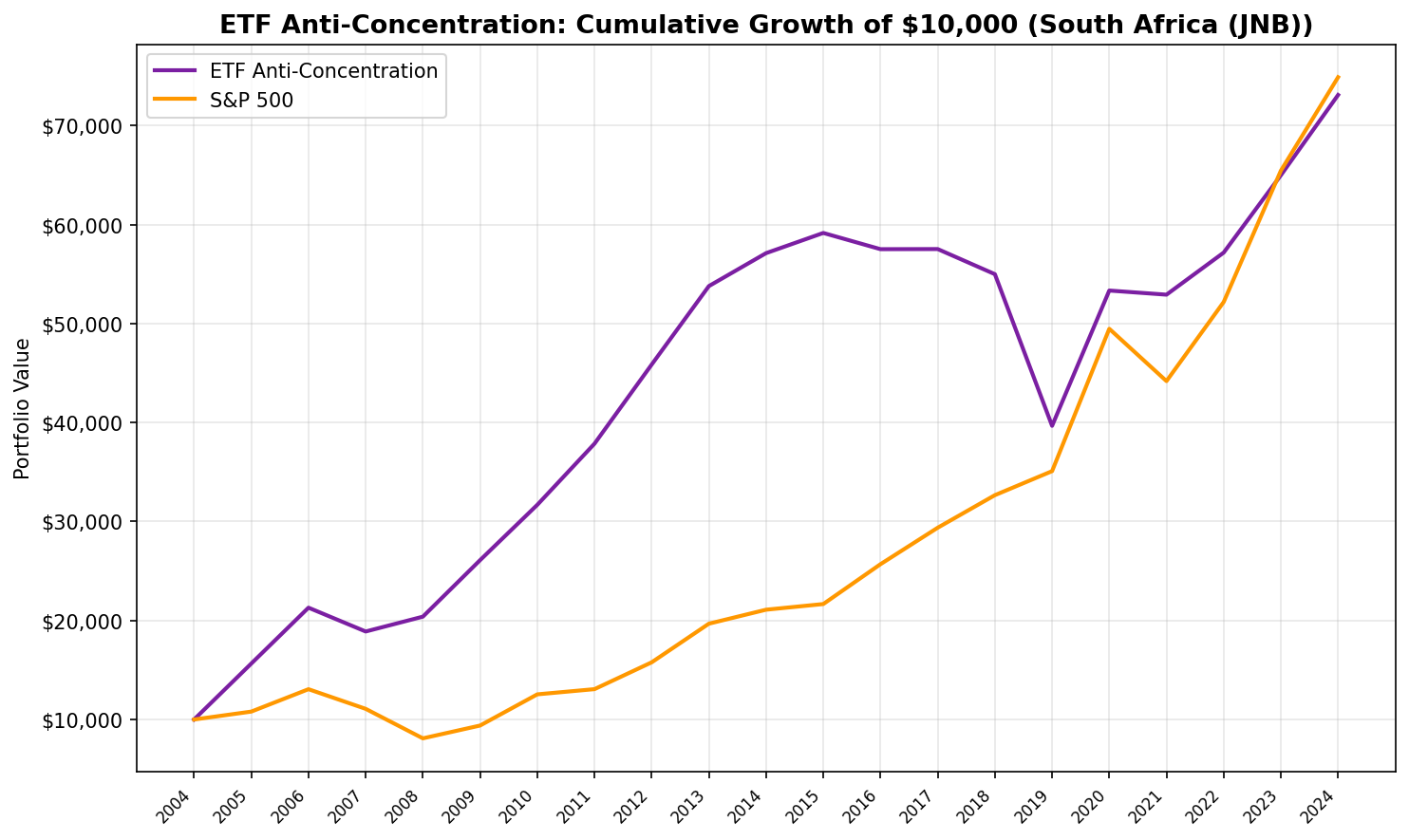

South Africa previously appeared to be the one exchange where buying stocks with low ETF concentration and decent fundamentals beat the S&P 500. With next-day close execution (correcting for the unrealistic same-day entry in our earlier analysis), the excess has nearly vanished. 10.46% CAGR vs 10.59% for SPY from 2005 to 2025. That's 20 years of data producing roughly flat performance against the benchmark.

Contents

- Method

- What We Found

- Why South Africa Is Different

- Cross-Reference: Consistent With Global Failure

- Limitations

- Part of a Series

The early years (2005-2012) were strong. The signal weakened after 2015 and never recovered. And the ETF holdings data is a current snapshot applied retroactively, which means there's look-ahead bias baked in.

Data: FMP financial data warehouse, 2000-2025. Updated April 2026.

Method

| Parameter | Value |

|---|---|

| Universe | Johannesburg Stock Exchange (JNB) |

| Rebalancing | Annual (July) |

| Execution | Next-day close (market-on-close) |

| Max positions | 30 stocks, equal weight |

| Cash rule | Fewer than 10 qualifying stocks |

| Data source | Ceta Research (FMP financial data warehouse) |

| Benchmark | S&P 500 (SPY). No JSE index data available in FMP. |

| Period | 2005-2025 |

The screen works in two stages.

First, we identify stocks that appear in broad-market ETFs but carry low individual weight. These are companies that exist in the index but don't dominate it. They sit in the long tail of ETF holdings, not the top 10 positions. The idea: these stocks get passive inflows (because they're in the index) but aren't the consensus mega-cap bets driving ETF concentration.

Second, we apply quality filters: positive earnings, reasonable leverage, adequate market cap. This removes the speculative names that sit at low weights because they're tiny or distressed.

The resulting portfolio holds stocks that are institutionally owned (they're in ETFs) but not concentrated bets (they don't dominate ETF weightings). It's a bet that the market's attention is disproportionately focused on top-weighted names, and that the rest of the ETF gets neglected.

The caveat up front: ETF holdings data from FMP is a current snapshot. We don't have historical snapshots showing which stocks were in which ETFs in 2005 or 2010. The backtest applies today's ETF composition backwards. This is look-ahead bias. The results show what would have happened if today's low-concentration stocks had always been low-concentration stocks. In reality, the composition shifts over time.

What We Found

Full period summary (2005-2025):

| Metric | Low-Concentration Quality | S&P 500 (SPY) |

|---|---|---|

| CAGR | 10.46% | 10.59% |

| Max Drawdown | -32.94% | -36.41% |

| Sharpe Ratio | 0.078 | — |

| Sortino Ratio | 0.136 | — |

| Calmar Ratio | 0.317 | — |

| Win Rate | 45.0% | — |

| Beta | 0.471 | 1.00 |

| Alpha | +0.71% | — |

| Avg Stocks Held | 18.6 | — |

| Avg Weight | 0.096% | — |

| Cash Periods | 0 of 20 | — |

The 0.471 beta stands out. This portfolio moved less than half as much as the S&P 500 on a year-to-year basis. But the +0.71% alpha is barely positive, and the 0.078 Sharpe confirms the risk-adjusted return isn't compelling. The Calmar ratio (0.317) looks decent because the max drawdown (-32.94%) was shallower than SPY's, not because the returns were strong.

Zero cash periods means the screen always found at least 10 qualifying stocks on JNB.

Year-by-year results:

| Year | Strategy | SPY | Spread | Notes |

|---|---|---|---|---|

| 2005 | +56.5% | +8.0% | +48.5 | Strong early years |

| 2006 | +36.1% | +20.9% | +15.1 | Broad JSE rally |

| 2007 | -11.3% | -15.2% | +3.9 | Less downside |

| 2008 | +7.9% | -26.9% | +34.8 | Beat SPY by 35 points in the crisis |

| 2009 | +28.0% | +16.0% | +12.0 | Recovery |

| 2010 | +21.4% | +33.5% | -12.1 | Lagged SPY |

| 2011 | +19.5% | +4.2% | +15.3 | SA domestic strength |

| 2012 | +21.1% | +20.7% | +0.4 | Flat spread |

| 2013 | +17.3% | +24.7% | -7.5 | US mega-cap run begins |

| 2014 | +6.2% | +7.2% | -1.0 | |

| 2015 | +3.6% | +2.7% | +0.9 | |

| 2016 | -2.8% | +18.6% | -21.3 | Worst relative year |

| 2017 | +0.0% | +14.3% | -14.3 | |

| 2018 | -4.4% | +11.2% | -15.6 | |

| 2019 | -27.9% | +7.4% | -35.3 | Worst absolute year |

| 2020 | +34.4% | +41.0% | -6.5 | Recovery but trailed SPY |

| 2021 | -0.8% | -10.7% | +9.9 | Beat SPY in down year |

| 2022 | +8.0% | +18.1% | -10.1 | |

| 2023 | +13.7% | +25.4% | -11.8 | |

| 2024 | +12.5% | +14.4% | -1.9 | Near-flat |

The story splits cleanly into two periods.

2005-2012: the strategy returned +57%, +36%, -11%, +8%, +28%, +21%, +20%, +21%. It beat SPY in six of eight years. The 2008 result (+7.9% vs -26.9%) is the standout. While global markets crashed, this basket of quality JSE mid-caps posted a positive return. That's the low-beta thesis working as designed.

2013-2024: the picture flips. The strategy beat SPY in only three of twelve years. 2019 was brutal at -27.9%. The cumulative gap over this stretch erased the early advantage. The final 20-year excess of -0.13% CAGR reflects a strong first half and a weak second half that canceled it out.

Why South Africa Is Different

Three structural features of the JSE explain why this screen worked here but not on most other exchanges.

Small, concentrated universe. The JSE has roughly 300-400 listed companies. After quality filters, the screen typically held 26.8 stocks per year. In a universe that small, the low-concentration signal can differentiate meaningfully. On NYSE/NASDAQ with 4,000+ stocks, the same filter produces a much noisier basket.

Emerging market dynamics. South African stocks were less correlated with global mega-cap tech during the 2005-2012 period. The low-beta result (0.470) partly reflects this. SA domestic consumer and financial companies don't move with Apple and Microsoft. In the US, almost everything correlates with the mega-caps that dominate ETF weightings.

Less ETF coverage. Fewer ETFs hold JSE stocks compared to US or European exchanges. That means the "low concentration" label on JNB is more meaningful. A stock with 0.095% average weight on the JSE genuinely sits outside the institutional spotlight. On the S&P 500, a stock at that weight is still held by hundreds of passive funds.

Cross-Reference: Consistent With Global Failure

We tested this same screen on 16 exchanges. With the execution correction (next-day close instead of same-day), South Africa no longer stands out. It joins the majority of exchanges that show flat-to-negative excess returns.

The 2005-2012 window drove the early outperformance, and it coincided with a period of strong JSE performance broadly. The low-beta characteristic (0.471) helped during the 2008 crisis, but the same low beta meant the portfolio lagged during the bull market years that followed.

Limitations

Look-ahead bias is the biggest issue. We used current ETF holdings data applied retroactively. Real-time, you wouldn't have known in 2005 which stocks would have low ETF concentration in 2026. This inflates results because today's ETF composition partially reflects which stocks performed well historically.

No local benchmark available. FMP's stock_eod table doesn't include the JSE All Share index. We benchmark against SPY, which means this is a cross-currency comparison (ZAR returns vs USD benchmark). A local JSE benchmark would be more appropriate but isn't available.

Small universe, thin statistical significance. 18.6 average stocks over 20 periods. That's roughly 370 stock-year observations. A single outlier year (like 2005's +56.5%) moves the 20-year CAGR measurably.

Rand denomination. All returns are in South African Rand. For a USD investor, currency depreciation (ZAR has weakened significantly against USD over this period) would reduce returns. The 10.46% CAGR is a local-currency figure. Dollar returns would be lower.

Transaction costs not modeled. Annual rebalancing on JNB mid-caps involves wider spreads and potential market impact. Real returns would be somewhat lower.

Post-2015 signal degradation. The screen stopped generating positive excess after 2015. The decay confirms the 2005-2012 outperformance was period-specific rather than a durable edge.

Next-day close execution. Trades execute at the closing price one day after the signal date, reflecting realistic market-on-close order flow.

Part of a Series

This is one of several regional backtests testing whether ETF concentration predicts stock returns.

- ETF Concentration: US Flagship — the primary backtest

- ETF Concentration: Global Comparison — all exchanges compared

- ETF Concentration: Norway — best risk-adjusted result

Data: Ceta Research (FMP financial data warehouse). ETF holdings are a current snapshot, not historical. Quality filters use point-in-time FY data. Next-day close execution. SPY benchmark (no local JSE index in FMP). Past performance does not guarantee future results. This is educational content, not investment advice.