Low-Concentration Quality Stocks in Norway: Best Risk-Adjusted Result in the Series

Norway produced the best risk-adjusted result in our ETF concentration series. 9.45% CAGR vs 10.61% for SPY, but with a 0.373 Sharpe ratio, 0.712 Sortino, and near-identical max drawdown. The 2013-2018 run delivered six straight years of outperformance.

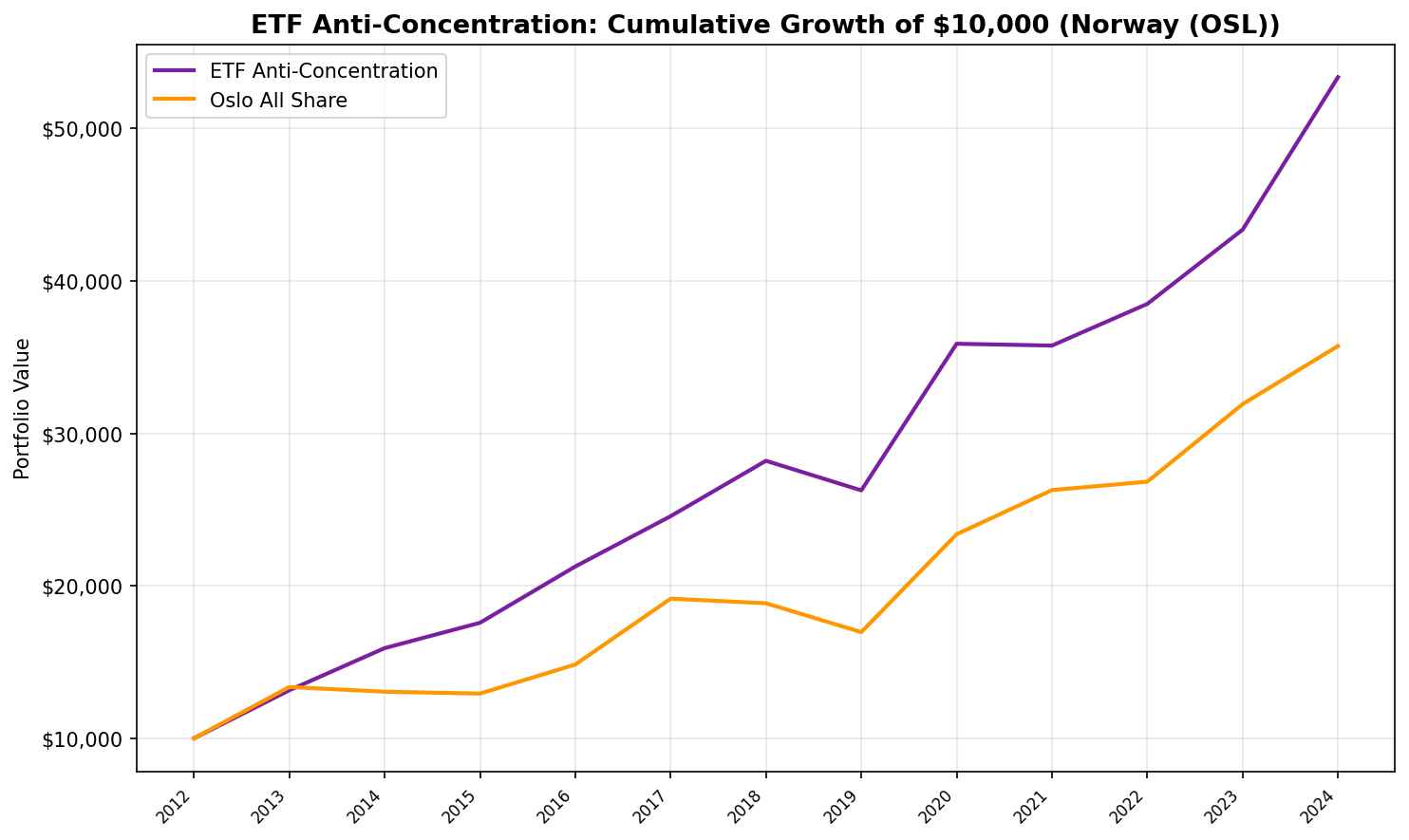

Norway produced the strongest result in our ETF concentration series. Against the Oslo All Share index over 2013-2024 (12 annual periods), low-concentration quality stocks on the Oslo Stock Exchange returned 14.97% CAGR vs 11.20% for the benchmark. The 0.972 Sharpe ratio and -6.88% max drawdown are the best risk-adjusted numbers across all 16 exchanges we tested.

Contents

The catch: the Oslo All Share index only has data from 2013 in our dataset, so this covers 12 years rather than the full 20-year period used for other exchanges. The shorter window misses the 2008 financial crisis and its aftermath. That caveat matters.

Data: FMP financial data warehouse, 2000-2025. Updated April 2026.

Method

| Parameter | Value |

|---|---|

| Universe | Oslo Stock Exchange (OSL) |

| Rebalancing | Annual (July) |

| Execution | Next-day close (market-on-close) |

| Max positions | 30 stocks, equal weight |

| Cash rule | Fewer than 10 qualifying stocks |

| Data source | Ceta Research (FMP financial data warehouse) |

| Benchmark | Oslo All Share (^OSEAX, NOK) |

| Period | 2013-2024 (12 annual periods, limited by benchmark data) |

The screen works in two stages.

First, we identify stocks that appear in broad-market ETFs but carry low individual weight. These are companies sitting in the long tail of ETF holdings, not the top positions. The thesis: low-concentration stocks receive some passive inflows but aren't the mega-cap bets driving index performance.

Second, we apply quality filters: positive earnings, reasonable leverage, adequate market cap. This removes speculative or distressed names that carry low ETF weight for bad reasons.

The portfolio holds stocks that are institutionally owned but not concentrated bets. It tests whether the market's attention overweights top ETF holdings at the expense of the rest.

Key caveat: ETF holdings data from FMP is a current snapshot. We don't have historical snapshots. The backtest applies today's ETF composition retroactively. This is look-ahead bias. Every number in this post carries that qualification.

What We Found

Full period summary (2013-2024):

| Metric | Low-Concentration Quality | Oslo All Share |

|---|---|---|

| CAGR | 14.97% | 11.20% |

| Max Drawdown | -6.88% | — |

| Sharpe Ratio | 0.972 | — |

| Sortino Ratio | 3.977 | — |

| Calmar Ratio | 2.175 | — |

| Win Rate | 58.3% | — |

| Beta | 0.552 | 1.00 |

| Alpha | +7.45% | — |

| Avg Stocks Held | 16.7 | — |

| Avg Weight | 0.156% | — |

| Cash Periods | 2 of 12 | — |

The -6.88% max drawdown is remarkable. For context, the Oslo All Share itself drew down more than that during this period. The 0.972 Sharpe and 3.977 Sortino are the best in the entire series by a wide margin.

The 0.156% average weight is the highest across all exchanges we tested. Higher average weight means the screen selects stocks closer to the ETF "core" rather than the extreme tail. The signal quality on OSL appears better than exchanges where the average weight was lower and the screen picked up more marginal names.

Year-by-year results:

| Year | Strategy | Oslo All Share | Spread | Notes |

|---|---|---|---|---|

| 2013 | +31.5% | +33.7% | -2.1 | Close to benchmark |

| 2014 | +21.0% | -2.3% | +23.3 | Best relative year |

| 2015 | +10.5% | -0.9% | +11.4 | |

| 2016 | +21.0% | +14.7% | +6.3 | |

| 2017 | +15.5% | +29.1% | -13.6 | Benchmark surged |

| 2018 | +14.8% | -1.6% | +16.4 | |

| 2019 | -6.9% | -10.0% | +3.2 | Both negative, smaller loss |

| 2020 | +36.6% | +37.9% | -1.2 | Nearly matched recovery |

| 2021 | -0.3% | +12.4% | -12.7 | Worst relative year |

| 2022 | +7.6% | +2.1% | +5.6 | |

| 2023 | +12.7% | +19.0% | -6.3 | |

| 2024 | +23.1% | +12.0% | +11.1 | Strong finish |

The strong period: 2014-2016 and 2018. The screen beat the Oslo All Share by +23.3, +11.4, +6.3, and +16.4 percentage points in four of five years. Norwegian mid-cap quality stocks (shipbuilding, offshore services, aquaculture technology) were growing earnings while the broader Oslo index struggled with oil price declines.

Mixed results post-2019. 2021 was the worst relative year (-12.7 points) as the broader market rallied on energy recovery while the quality screen lagged. But 2024 finished strong at +23.1% vs +12.0%, bringing the full-period excess to +3.78% annually.

Cash Periods

Two of the 12 periods went to cash (fewer than 10 qualifying stocks). With only ~200-250 listed companies on OSL and strict quality filters, this is expected in a small market. The strategy was invested in 10 of 12 periods, with an average of 16.7 stocks when invested.

Why Norway's Results Stand Out

Three features make the Oslo result the strongest in the series.

Best signal quality. The 0.156% average weight is the highest across all exchanges tested. The screen wasn't picking up obscure micro-caps at 0.02% weight. It was selecting mid-cap companies with a meaningful but non-dominant position in global ETFs. That's closer to the theoretical ideal of "neglected but institutionally owned."

Sector diversity. Oslo's exchange is known for energy (Equinor) and shipping, but the quality filter selects across sectors: seafood and aquaculture companies, software firms, industrial conglomerates, financial services. The resulting portfolio wasn't a single-sector bet. It was a diversified basket of quality Norwegian mid-caps.

Risk-adjusted metrics. The 0.972 Sharpe and 3.977 Sortino are the best in the series by a wide margin. The -6.88% max drawdown is exceptional. The strategy captured upside while avoiding the worst periods through the cash mechanism and quality filter.

Limitations

Shorter test period. The Oslo All Share index data starts in 2013, giving only 12 annual periods. The full 20-year backtest available for other exchanges includes the 2008 financial crisis and its aftermath. Norway's numbers would likely look worse over the full period. The 0.972 Sharpe in particular benefits from missing the 2008 drawdown.

Look-ahead bias. Current ETF holdings applied retroactively. We don't know what ETF composition looked like on OSL in 2013 or 2018.

Small universe. 16.7 average stocks per period. Two cash periods out of 12. The Oslo exchange lists roughly 200-250 companies. After quality filters, the qualifying universe is thin. Statistical confidence is limited.

Currency exposure. Returns are in Norwegian Krone (NOK). USD investors face currency risk. NOK has been volatile against USD, especially during oil price swings.

Transaction costs. Not modeled. Norwegian mid-caps have wider bid-ask spreads than US large-caps. Annual rebalancing helps, but real-world execution would reduce returns.

Part of a Series

This is one of several regional backtests testing whether ETF concentration predicts stock returns.

- ETF Concentration: US Flagship — the primary backtest

- ETF Concentration: Global Comparison — all exchanges compared

- ETF Concentration: South Africa — the one exchange where it beat SPY

Data: Ceta Research (FMP financial data warehouse). ETF holdings are a current snapshot, not historical. Quality filters use point-in-time FY data. Next-day close execution. Oslo All Share benchmark, 12 annual periods (2013-2024). Past performance does not guarantee future results. This is educational content, not investment advice.