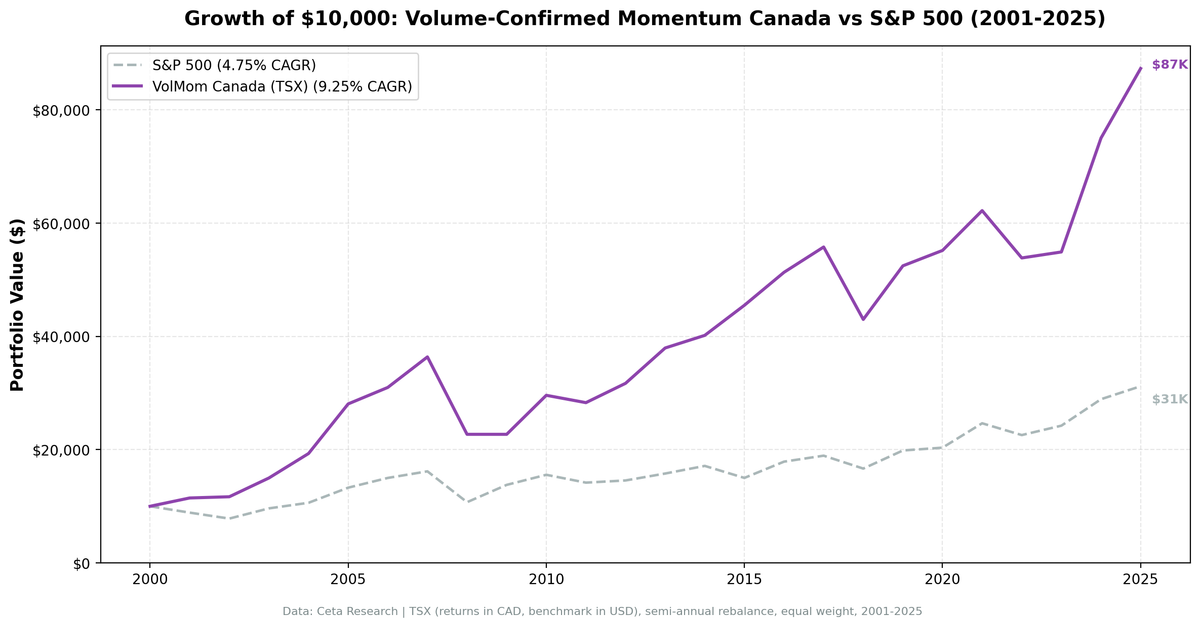

Volume-Confirmed Momentum on Canada Stocks: 9.25% CAGR, 32.4% Down Capture

Volume-confirmed momentum on Canadian equities from 2001 to 2025: 9.25% CAGR vs 4.75% for the TSX Composite, +4.49% annual excess return, Sharpe 0.428, and 32.4% down capture — the lowest of any exchange in this study. The commodity-driven TSX provides natural decorrelation.

Volume-Confirmed Momentum on Canada Stocks: 32.4% Down Capture, 9.25% CAGR

The best risk-adjusted number across all 17 exchanges by Sharpe ratio belongs to Canada — and the down capture of 32.4% against the TSX Composite is exceptional. When the TSX falls, this portfolio falls only a third as hard. Over 24.5 years, the strategy returned 9.25% annually against 4.75% for the TSX Composite — a +4.49% annual edge. The TSX Composite's relatively low long-term return makes the absolute comparison look better than vs SPY, but the factor genuinely adds value here.

Contents

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

| Parameter | Value |

|---|---|

| Universe | TSX (Canada) |

| Rebalancing | Semi-annual (January, July) |

| Signal | 12-month return, skip last month (T-1M to T-12M) |

| Volume filter | 3-month avg daily volume > 12-month avg (vol_ratio > 1.0) |

| Quality filter | netIncome > 0 AND operatingCashFlow > 0 (FY, 45-day lag) |

| Selection | Top 30 by momentum, equal weight |

| Min threshold | 10 qualifying stocks to deploy capital |

| Data source | FMP via Ceta Research warehouse |

| Benchmark | TSX Composite (^GSPTSE) |

| Period | 2001–2025 |

| Academic basis | Lee & Swaminathan (2000), Journal of Finance 55(5) |

Canada's exchange is structurally different from the US. The TSX is heavily weighted toward energy, materials, and financials. During US equity crashes, these sectors often decorrelate — energy and materials are commodity-driven, and commodity prices don't always fall with equities. That's the likely mechanism behind the exceptional down capture.

What We Found

This is a genuine alpha story and a risk management story. +4.49% annual excess return over 24.5 years against the TSX Composite is substantial. With 32.4% down capture and a Sharpe of 0.428, Canada delivers excellent risk-adjusted returns.

24.5-year summary (2001–2025):

| Metric | Volume-Confirmed Momentum | TSX Composite |

|---|---|---|

| CAGR | 9.25% | 4.75% |

| Sharpe Ratio | 0.428 | — |

| Max Drawdown | -37.58% | — |

| Down Capture | 32.4% | 100% |

| Up Capture | 109.6% | 100% |

| Cash Periods | 2 of 49 (4%) | — |

| Avg Stocks Held (when invested) | 28.4 | — |

The 32.4% down capture vs the TSX Composite is the standout number. When the TSX falls, this portfolio falls only a third as hard. Combined with 109.6% up capture, the strategy takes more of the upside and far less of the downside — that's the asymmetry that produces a 4.49% annual edge and the high Sharpe ratio.

Note that the TSX Composite had relatively modest returns (4.75% CAGR) over this period, which makes the comparison look favorable. A comparison vs SPY shows a smaller 0.66% edge. But for a Canadian investor benchmarking against their home market, the 4.49% vs the TSX Composite is the relevant number.

Year-by-year standouts:

| Year | Portfolio | TSX Composite | Notes |

|---|---|---|---|

| 2001 | +14.7% | -11.2% | +25.9pp — commodity resilience vs crash |

| 2002 | +1.9% | -11.9% | +13.7pp — outperformed in down year |

| 2003 | +28.4% | +23.1% | Recovery plus commodity cycle |

| 2004 | +28.8% | +10.2% | +18.6pp — energy sector momentum |

| 2005 | +45.4% | +25.1% | +20.2pp — oil supercycle |

| 2006 | +10.4% | +12.9% | Slight miss |

| 2008 | -37.6% | -33.7% | Close to benchmark in worst year |

| 2009 | 0% (cash) | +28.5% | Cash — missed recovery |

| 2010 | +30.4% | +12.9% | +17.4pp — commodity bounce |

| 2015 | +13.2% | -12.4% | +25.6pp — best relative year |

| 2018 | -22.9% | -12.0% | -10.9pp — worst relative year |

| 2022 | -13.4% | -8.4% | Underperformed in rate-hike year |

| 2024 | +36.6% | +19.3% | +17.4pp — energy and materials momentum |

| 2025 | +16.4% | +7.9% | +8.4pp — continued outperformance |

2001 and 2002 are the sharpest examples of the Canada thesis. During the US dot-com crash, the TSX Composite fell 11.2% in 2001 and 11.9% in 2002. The Canada portfolio returned +14.7% and +1.9% — outperforming the local index by 25.9pp and 13.7pp. The TSX's commodity-heavy composition meant the strategy held energy and materials stocks with genuine volume momentum, sectors that didn't participate in the tech bubble and didn't suffer its burst.

The oil supercycle years (2003-2007). Canada volume-confirmed momentum captured the commodity super-cycle almost perfectly. Energy and materials stocks with rising volume were exactly the stocks passing the screen. The 2005 result — +45.4% vs SPY +7.2% — is the clearest example: oil prices were rising, Canadian energy names were seeing institutional inflows, and the volume filter concentrated the portfolio there.

2018 was the worst relative year. The portfolio fell 22.9% against the TSX Composite's -12.0%. The US Federal Reserve's rate hiking cycle hit rate-sensitive sectors, and Canadian financials and REITs — often picked up by momentum screens — took the brunt. This is the exception rather than the rule for Canada, but it shows that the outperformance isn't unconditional.

2015 was the best relative year. The portfolio returned +13.2% against the TSX Composite's -12.4% — a 25.6pp gap. The Canadian oil price crash of 2015 hurt the broader TSX, but the momentum filter avoided energy companies that had already fallen. The volume screen concentrated the portfolio in sectors with rising institutional interest, which held up while the TSX's large commodity exposure dragged the index down.

Why Canada volume signals work. TSX volume in energy and materials is dominated by institutional investors making sector bets tied to commodity prices. When oil or mining stocks show rising relative volume, it often reflects genuine sector rotation — pension funds and resource-focused institutions shifting allocation. That's a different signal from the ETF rebalancing noise that dominates US volume data.

Backtest Methodology

- Data: FMP financial data via Ceta Research warehouse. Price data from

stock_eod(adjusted closes). - Point-in-time: Quality filters use annual FY filings with 45-day reporting lag. No look-ahead bias.

- Signal: Price at T-12M to T-1M. Skip last month avoids short-term reversal contamination per Jegadeesh & Titman (1993).

- Volume ratio: 63-day avg daily volume divided by 252-day avg daily volume, computed at each rebalance date.

- Data quality: Stocks with adjusted close < $1 at either lookback date excluded. Portfolio momentum capped at 500% per stock.

- Equal weight: 30 positions, 3.33% each. No intraperiod rebalancing.

- Transaction costs: Modeled as size-tiered commissions. See methodology.

- Benchmark: TSX Composite (^GSPTSE), CAD-denominated. Strategy returns are also CAD-denominated. A secondary SPY comparison shows +0.66% annual edge over the US index.

Limitations

Currency risk. Strategy returns are in CAD. A USD-based investor faces CAD/USD exchange rate exposure. The CAD has fluctuated considerably vs the USD over this period, tracking oil prices. Currency effects can be meaningful in either direction.

Commodity concentration. The portfolio's low down capture likely depends on its energy and materials concentration. If the composition of Canadian momentum shifts away from commodities — as it might in a prolonged commodity bear market — the decorrelation benefit would shrink.

Up capture of 88.8% is a real cost. In sustained US equity bull markets like 2013-2021, a strategy that captures only 88.8% of the upside compounds slowly relative to just holding SPY. The 24.5-year result favours Canada slightly, but there were long stretches where SPY was the better choice.

The two cash periods. The 4% cash rate (2 of 49 semi-annual periods) is low, but cash periods always represent missed upside. Those 2 periods weren't in consecutive years, so they didn't compound into a major drag.

TSX Composite had low returns. The TSX Composite's 4.75% CAGR over 2001-2025 is below the US S&P 500 (8.59%). This makes the strategy's 9.25% CAGR look better relative to the local benchmark. Vs SPY the excess is a more modest 0.66%.

Takeaway

Canada volume-confirmed momentum delivers both alpha and risk reduction vs the local TSX Composite. The 4.49% annual excess return, Sharpe of 0.428, and 32.4% down capture describe a strategy that consistently outperforms the index while protecting capital during downturns.

The mechanism is commodity exposure. Canadian momentum screens naturally concentrate in energy and materials — sectors that decorrelate from typical equity crashes. The volume filter reinforces this by selecting for stocks with genuine institutional accumulation behind them. In Canada, that signal tends to fire in sectors that hedge rather than amplify equity risk.

The 109.6% up capture means the strategy also participates in TSX bull markets. The asymmetry — capturing more of the upside, far less of the downside — is what produces the Sharpe ratio leadership and the 4.49% annual edge over the benchmark.

Part of a Series

This is part of a multi-exchange volume-confirmed momentum study:

- Volume-Confirmed Momentum: US Stocks

- Volume-Confirmed Momentum: India

- Volume-Confirmed Momentum: Canada

- Volume-Confirmed Momentum: Sweden

- Volume-Confirmed Momentum: 17-Exchange Comparison

References

- Lee, C. & Swaminathan, B. (2000). Price Momentum and Trading Volume. Journal of Finance, 55(5), 2017-2069.

- Jegadeesh, N. & Titman, S. (1993). Returns to Buying Winners and Selling Losers. Journal of Finance, 48(1), 65-91.

- Daniel, K. & Moskowitz, T. (2016). Momentum Crashes. Journal of Financial Economics.

Past performance does not guarantee future results. This is educational content, not investment advice.