Small-Cap Growth in China: +7.76% Excess vs Local Benchmark

Chinese small-cap growth stocks generated +7.76%/yr excess over the SSE Composite, turning $10K into $129,070. The alpha is real, but so is the -72% max drawdown and two A-share bubble years that drove most of the outperformance.

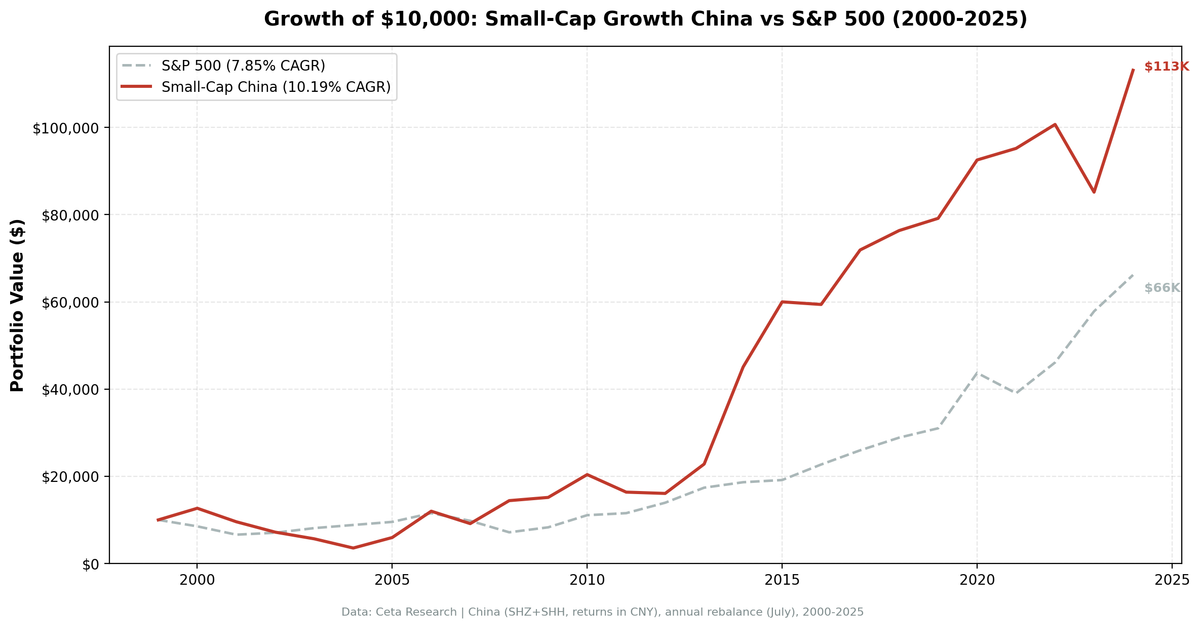

China produced the highest absolute return of any market we tested. $10,000 invested in Chinese small-cap growth stocks in 2000 became $129,070 by end of 2024. That's 10.19% CAGR and +2.34%/yr excess over SPY across 25 years.

Contents

- What We Tested

- What We Found

- The Low Down Capture Explained

- Annual Returns: 25 Years

- The MaxDD Reality

- 68% Win Rate Against SSE, Variable vs SPY

- Why the Premium Exists

- What This Means for Practical Allocation

- Limitations

- Takeaway

- References

Before you build a portfolio around that number, read this carefully.

The local market context matters. The SSE Composite Index returned just 2.43% CAGR over the same 25 years. Against that baseline, the small-cap growth strategy generated +7.76%/yr local excess return, more than triple the SPY excess. This tells you the premium is real in China's A-share market, but much of it is capturing systematic outperformance of Chinese equities rather than just size/growth factors.

The alpha is concentrated. Two years, 2006 (+101.3%) and 2014 (+97.7%), account for a disproportionate share of the total return. Both were documented A-share market manias where valuations disconnected from fundamentals. The maximum drawdown is -72.01%. The win rate against SPY is 68% (17 of 25 years).

The data is telling you something nuanced: the small-cap growth premium exists in China, but it's extracted through bubble participation and exposure to a market that systematically underperformed global equities over this period.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

What We Tested

The strategy selects small-cap A-share stocks across SHZ (Shenzhen) and SHH (Shanghai) with revenue momentum:

- Market cap: 5%-200% of the exchange threshold (small-cap range)

- Revenue growth: >15% year-over-year (fiscal year)

- Profitability: Net income > 0

- Leverage: Debt-to-equity < 2.0

- Selection: Top 30 by revenue growth, equal-weighted

- Rebalancing: Annual in July, 45-day filing lag

Data from the FMP financial data warehouse, 2000-2024. Average portfolio size: 20.4 stocks. Full methodology: METHODOLOGY.md.

What We Found

The aggregate numbers look strong. +2.34%/yr excess over SPY, +7.76%/yr excess over the SSE Composite, 128.75% up capture vs SPY, Sharpe of 0.208. But the distribution of returns is extreme.

The SSE Composite benchmark context is critical. The local market returned just 2.43% CAGR over 25 years, dramatically underperforming global equities. The small-cap growth strategy's 10.19% CAGR isn't just a size premium, it's capturing the structural advantage of growth-focused small caps over state-dominated large caps in China's economy.

2006: +101.3%. The Shanghai Composite rose over 130% that year. A-share markets were in the middle of a multi-year speculative rally driven by domestic retail investor enthusiasm and limited investment alternatives for Chinese savers. Small-cap stocks amplified the move. This was a real market event, fully documented, and the returns here reflect genuine prices. But capturing them required holding through the year. Nobody rang a bell.

2014: +97.7%. Another A-share mania, this time driven by margin lending expansion, government signals of support, and retail speculation. The rally began in Q3 2014 and went vertical by year-end. Small-cap growth stocks were at the center of it.

These aren't data artifacts. They happened. But they also represent the kind of extreme event that's very difficult to systematically exploit in real portfolios. Position sizing, liquidity, and emotional discipline all become acute issues when markets double in a year.

The Low Down Capture Explained

Down capture of 49.85% vs SPY means the portfolio averaged half the losses in years when SPY fell. This is the A-share low-correlation effect combined with Chinese government stimulus patterns.

2008 is the clearest example: +57.6% for this portfolio while SPY fell 26.1%. Global financial crisis. US markets in freefall. Chinese A-shares rallied on a massive government stimulus package (4 trillion yuan) that was injected directly into domestic infrastructure and consumption. Foreign investors couldn't easily access A-shares at scale in 2008. The market moved on domestic flows.

This decorrelation isn't unique to 2008. Chinese monetary and fiscal policy doesn't coordinate with the US cycle. When the Fed is tightening and SPY is falling, Chinese authorities may be easing. The strategies of the two economies diverge, and so do the markets.

For a global portfolio, that uncorrelated behavior has real diversification value. But it cuts both ways: China can also sell off hard when the rest of the world is rising (2001: -24.5%, 2002: -24.9%, 2004: -37.4%).

Annual Returns: 25 Years

| Year | Strategy | SSE Composite | Excess |

|---|---|---|---|

| 2000 | +26.7% | +16.4% | +10.3% |

| 2001 | -24.5% | -21.8% | -2.6% |

| 2002 | -24.9% | -13.1% | -11.8% |

| 2003 | -21.3% | -3.9% | -17.3% |

| 2004 | -37.4% | -27.3% | -10.0% |

| 2005 | +68.1% | +62.1% | +6.0% |

| 2006 | +101.3% | +126.0% | -24.7% |

| 2007 | -23.8% | -30.9% | +7.1% |

| 2008 | +57.6% | +15.4% | +42.2% |

| 2009 | +5.1% | -22.1% | +27.3% |

| 2010 | +34.5% | +18.0% | +16.5% |

| 2011 | -19.7% | -20.9% | +1.1% |

| 2012 | -1.8% | -9.9% | +8.0% |

| 2013 | +41.9% | +2.6% | +39.3% |

| 2014 | +97.7% | +90.0% | +7.7% |

| 2015 | +33.1% | -23.6% | +56.7% |

| 2016 | -1.0% | +6.9% | -7.9% |

| 2017 | +21.0% | -13.2% | +34.2% |

| 2018 | +6.2% | +9.7% | -3.5% |

| 2019 | +3.7% | +1.5% | +2.1% |

| 2020 | +16.9% | +13.9% | +3.1% |

| 2021 | +2.9% | -3.2% | +6.1% |

| 2022 | +5.8% | -4.7% | +10.5% |

| 2023 | -15.4% | -7.6% | -7.8% |

| 2024 | +32.8% | +15.3% | +17.6% |

The return distribution is bimodal. Enormous gains in bubble years, sideways to negative returns in most other years. 2001-2004 was a brutal four-year drawdown: -24.5%, -24.9%, -21.3%, -37.4%. That's four consecutive years of significant losses. Staying invested through that period would have tested any investor's conviction.

Against the SSE Composite, the pattern is clearer: the strategy consistently outperformed the local market across most years, with notable exceptions in 2006 (when the SSE itself rose 126%) and periodic years when large-cap state enterprises drove the index.

The MaxDD Reality

-72.01% maximum drawdown. This is the number that should anchor your position sizing.

A drawdown of that magnitude is compounded across multiple years of losses. The 2001-2004 period produced most of it. Peak-to-trough, the portfolio lost nearly three-quarters of its value before recovering. The recovery required the 2005 (+68.1%) and 2006 (+101.3%) years to come, which they did, but you had no way of knowing that at the trough.

For comparison: SPY's worst drawdown in the same period is -36.27%. The China strategy drawdown is nearly double. The SSE Composite itself had a -65% drawdown, so the small-cap strategy's additional -7pp reflects the leverage effect of smaller companies.

A position size of 5-10% of a global portfolio is supportable if you understand the drawdown profile. 30%+ of a portfolio in this strategy, given the MaxDD, would create intolerable volatility for most investors.

68% Win Rate Against SSE, Variable vs SPY

The strategy beats the SSE Composite in 17 of 25 years (68% win rate), demonstrating consistent outperformance of the local market. Against SPY, the comparison is more complex because you're measuring exposure to Chinese equities (which systematically underperformed global markets) plus the size/growth premium.

Against the SSE Composite, the wins are both frequent and large. Years like 2008 (+42.2% excess), 2013 (+39.3%), 2015 (+56.7%), and 2017 (+34.2%) show the small-cap growth premium operating clearly within the Chinese market context.

The rare losing years against the SSE (2002, 2003, 2004, 2006, 2016, 2018, 2023) typically occurred during periods when state-owned large caps were policy beneficiaries or when the SSE itself was rallying on index-heavy names that small caps couldn't match.

This is a right-skewed return distribution relative to both benchmarks. But the 68% local win rate is much stronger than the story against SPY suggests.

Why the Premium Exists

China's A-share market has structural features that preserve inefficiency:

Limited foreign access. Historically, foreign investors had restricted access to A-shares through QFII quotas. This limited the arbitrage capital available to price away obvious inefficiencies. The market moved primarily on domestic flows.

Retail dominance. Chinese equity markets have a very high proportion of retail investors relative to most developed markets. Retail participation amplifies momentum, creates bubble dynamics, and generates mispricings that systematic strategies can exploit.

Thin coverage at the small-cap end. Even large domestic Chinese sell-side firms concentrate coverage on large-caps and state-owned enterprises. The small-cap growth universe is followed lightly.

Information environment. Financial reporting quality and disclosure norms differ from developed markets. Investors who do rigorous fundamental screening may find opportunities that passive observers miss.

These factors create genuine opportunity, but they also create the extreme drawdowns. The same retail dominance that drives 100% rally years also drives 35% crash years on sentiment shifts.

What This Means for Practical Allocation

China's numbers should be read as: high return potential, concentrated in rare events, with extreme drawdown risk and low global correlation.

For a global factor portfolio, the low correlation to US equities (-44.7% down capture) provides real diversification. A small allocation to Chinese small-cap growth adds return potential while reducing portfolio-level drawdown correlation.

For a concentrated bet, the drawdown profile is too severe for most investors without genuine risk tolerance and a multi-decade horizon.

The strategy doesn't generate consistent year-by-year alpha. It generates occasional enormous alpha and requires surviving the years when it doesn't.

Limitations

- A-share access: Foreign investors historically faced restrictions on A-share investment. Execution at the historical returns would not have been straightforward for international investors.

- Currency: Returns are in CNY. USD investors face RMB/USD exchange rate exposure.

- Bubble year concentration: Remove 2006 and 2014, and the return profile looks much weaker. The overall CAGR is heavily dependent on those two years.

- Liquidity and market impact: Chinese small-caps can trade with wide spreads. Annual rebalancing in a 20-30 stock portfolio would face meaningful transaction costs.

- Regulatory risk: Chinese securities regulation can change rapidly. Sector crackdowns (2021 education, tech) demonstrate that regulatory risk is real and can materially affect returns.

Takeaway

The Chinese small-cap growth premium is real across 25 years. The +7.76%/yr excess return vs the SSE Composite and $129,070 terminal value aren't statistical noise. But the mechanism is different from what most investors expect from a systematic factor strategy.

This isn't steady compounding. It's participation in rare market dislocations (2006, 2008, 2014) combined with survival through brutal multi-year drawdowns (2001-2004). The low down capture (49.85% vs SPY) gives it portfolio-level diversification value. The -72% MaxDD means position sizing must be disciplined.

The SSE Composite's weak 2.43% CAGR baseline means the strategy's 10.19% CAGR is impressive locally but modest globally. You're betting on Chinese small-cap growth outperforming Chinese large caps, which it has done consistently, but also accepting exposure to a market that lagged global equities.

If you're building a global small-cap factor exposure, China belongs in the conversation. Just size it for the drawdown, not the headline CAGR.

References

- Banz, R. (1981). "The Relationship Between Return and Market Value of Common Stocks." Journal of Financial Economics, 9(1), 3-18.

- Fama, E. & French, K. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427-465.

- Fama, E. & French, K. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56.

- Van Dijk, M. (2011). "Is size dead? A review of the size effect in equity returns." Journal of Banking & Finance, 35(12), 3263-3274.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.