We Tested Revenue Acceleration in 12 Markets. Only One Beat the Benchmark.

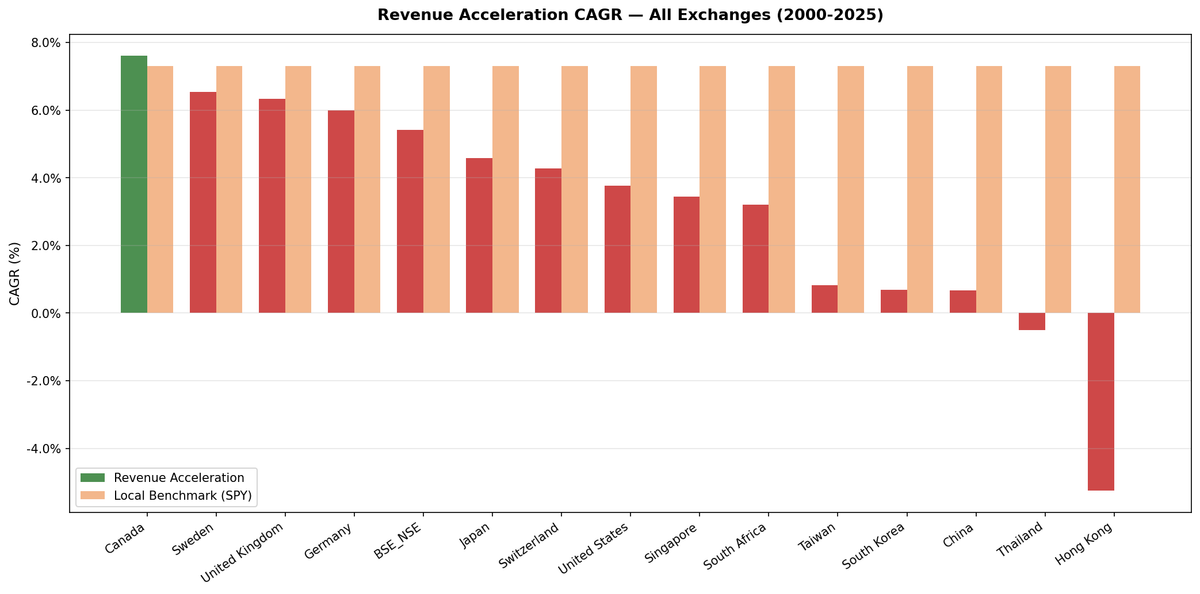

Revenue acceleration backtested in 12 markets over 25 years. Canada is the only positive result at +0.29%. Hong Kong is the worst at -12.55%. The signal fails globally but the how varies enormously by market.

Revenue acceleration sounds like a sensible signal. Buy companies whose revenue growth rate is speeding up, not just growing. The second derivative of revenue, applied to portfolio construction.

Contents

- Method

- The Global Picture

- Twelve markets. One positive result.

- What We Found

- The developed West held up best.

- Developed Asian markets underperformed significantly.

- China's 5.5% down capture is extraordinary.

- Hong Kong is the worst result in the study.

- Why the Signal Fails Broadly

- What Works vs What Doesn't

- Limitations

- Takeaway

- Individual Market Deep Dives

- References

We tested it in 12 markets over 25 years. Canada was the only one with positive excess returns, at +0.29% per year. Hong Kong lost to the benchmark by 12.55% annually. The pattern is clear: this signal doesn't generate alpha globally. But how it fails varies enormously by market.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: 12 exchanges (see table below) Period: 2000–2025 (25 years per exchange) Rebalancing: Annual (April 1), equal weight Benchmark: S&P 500 Total Return (SPY) Cash rule: Hold cash if fewer than 10 stocks qualify Transaction costs: Size-tiered model (0.1–0.5% one-way)

Signal: Revenue growth acceleration computed from 3 consecutive annual FY filings. Filters: growth rate speeding up, current growth > 5%, ROE > 10%, debt/equity < 1.5, exchange-specific minimum market cap. Top 30 stocks by acceleration magnitude.

Three exchanges excluded from results: - Singapore (SES): average 8.8 qualifying stocks — below the 10-stock minimum for investable signals - South Africa (JNB): 36% cash periods — too many years with fewer than 10 qualifying stocks - South Korea (KSC): 36% cash periods — same issue

All 12 exchanges below have consistent FY data coverage across the full period.

Note on benchmark: All portfolios are compared against SPY in local currency terms. This is a relative comparison, not a currency-adjusted absolute return.

The Global Picture

Twelve markets. One positive result.

| Exchange | CAGR | SPY | Excess | Down Capture | Max Drawdown | Cash % | Avg Stk |

|---|---|---|---|---|---|---|---|

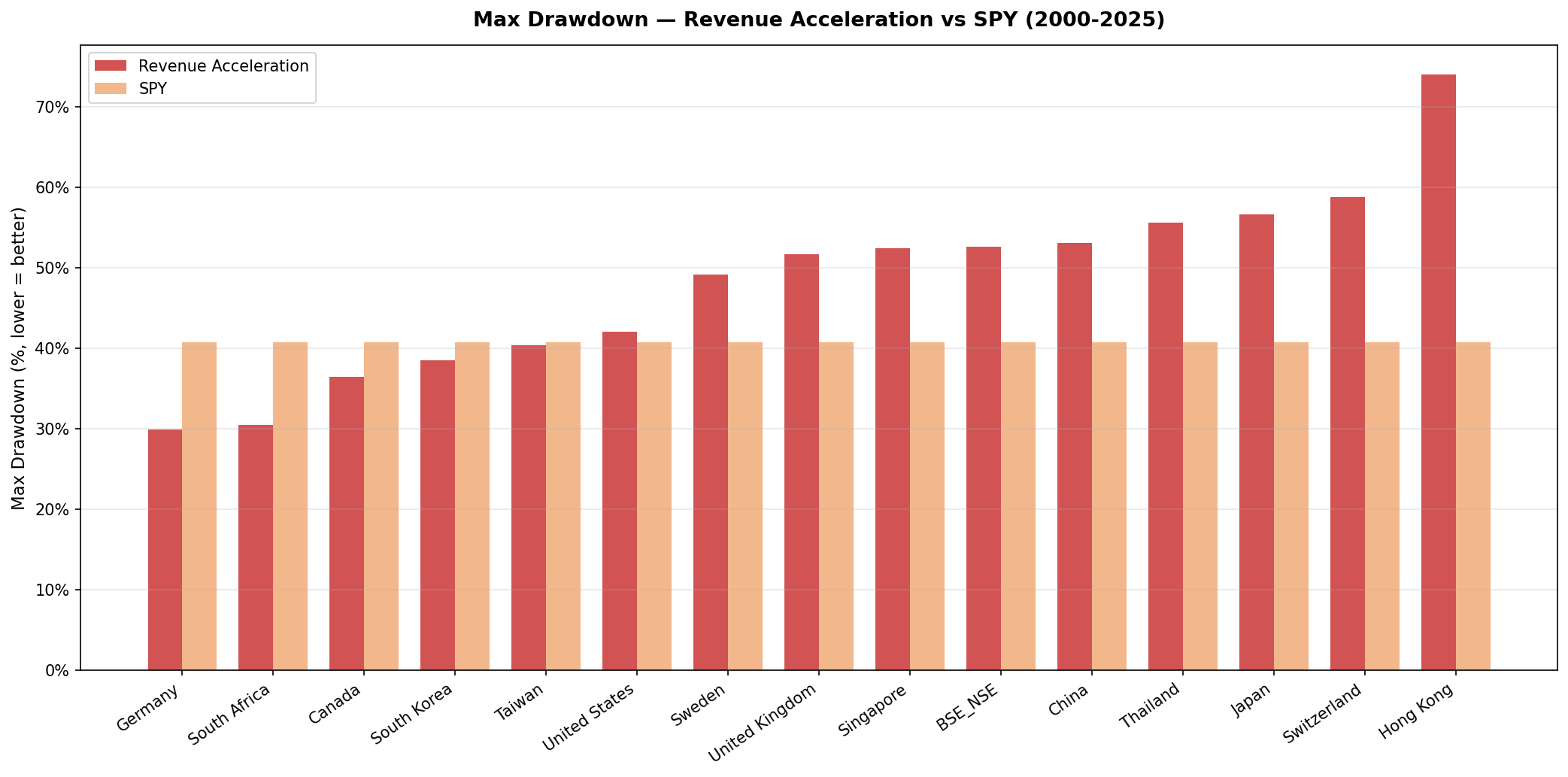

| Canada (TSX) | 7.60% | 7.30% | +0.29% | 44.0% | -36.48% | 0% | 23.2 |

| Sweden (STO) | 6.53% | 7.30% | -0.77% | 77.7% | -49.20% | 24% | 22.8 |

| UK (LSE) | 6.34% | 7.30% | -0.96% | 98.3% | -51.69% | 0% | 20.1 |

| Germany (XETRA) | 6.00% | 7.30% | -1.30% | 58.5% | -29.91% | 0% | 18.4 |

| India (BSE+NSE) | 5.42% | 7.30% | -1.88% | 57.8% | -52.59% | 24% | 23.4 |

| Japan (JPX) | 4.58% | 7.30% | -2.72% | 75.1% | -56.67% | 20% | 25.9 |

| Switzerland (SIX) | 4.27% | 7.30% | -3.03% | 106.9% | -58.80% | 0% | 16.3 |

| US (NYSE+NASDAQ+AMEX) | 3.76% | 7.30% | -3.54% | 109.6% | -42.06% | 0% | 24.7 |

| Taiwan (TAI+TWO) | 0.82% | 7.30% | -6.48% | 56.9% | -40.41% | 28% | 25.7 |

| Korea (KSC) | 0.69% | 7.30% | -6.61% | 59.9% | -38.51% | 36% | 25.4 |

| China (SHZ+SHH) | 0.67% | 7.30% | -6.63% | 5.5% | -53.11% | 0% | 23.0 |

| Thailand (SET) | -0.50% | 7.30% | -7.80% | 83.2% | -55.60% | 20% | 23.7 |

| Hong Kong (HKSE) | -5.25% | 7.30% | -12.55% | 107.6% | -74.00% | 0% | 19.3 |

What We Found

The developed West held up best.

The top four markets by excess return are all developed Western economies: Canada (+0.29%), Sweden (-0.77%), UK (-0.96%), and Germany (-1.30%). None of them produced strong alpha, but the underperformance is modest.

Canada's exceptional down capture (44%) and Germany's low max drawdown (-29.91%) suggest that revenue acceleration in these markets produces portfolios with real defensive characteristics, even without generating positive alpha. The signal selects into different sectors in these economies — industrials, materials, energy — rather than the tech-heavy composition it produces in US screens.

Developed Asian markets underperformed significantly.

Japan (-2.72%), Switzerland (-3.03%), and especially the US (-3.54%) all show meaningful underperformance. Taiwan (-6.48%), Korea (-6.61%), and China (-6.63%) are worse still.

The Asian underperformance has a different structure than the Western underperformance. In Asian markets, early data coverage is thinner — many exchanges had 6-9 qualifying companies in 2000-2006, leading to intermittent cash holding that dampened returns during strong early-cycle years. But even excluding those early years, the signal doesn't work in these markets.

China's 5.5% down capture is extraordinary.

Chinese revenue accelerators produced only 0.67% CAGR over 25 years — terrible absolute performance. But the down capture of 5.5% means that when the S&P 500 fell, this portfolio barely moved. The A-share market has a different structure: domestic retail investors drive price action, and accelerating small/mid-cap companies often don't correlate with the large-cap crashes that dominate the SPY comparison.

This is a curiosity, not a recommendation. 0.67% CAGR is not a portfolio to run.

Hong Kong is the worst result in the study.

-5.25% CAGR and -12.55% annual excess over 25 years, with a max drawdown of -74.00%. Revenue-accelerating Hong Kong companies are heavily exposed to Chinese growth cycles and property sector volatility. The strategy picks exactly the names that captured China's expansion — and then captured every contraction as well, amplified.

Down capture of 107.6% confirms the same dynamic as the US: these portfolios concentrated in late-cycle names that crashed hardest.

Why the Signal Fails Broadly

Revenue acceleration identifies companies at or near peak growth velocity. The academic basis suggests markets should underreact to this data — but the evidence over 25 years says markets have priced it in.

There are three plausible mechanisms:

1. Information is priced. Revenue acceleration from annual filings is widely tracked by analysts and quant funds. By the time a company shows 3 consecutive years of accelerating revenue in its annual filings, that trajectory has already appeared in quarterly earnings, guidance revisions, and analyst models. The annual backtest is acting on stale information.

2. Peak acceleration is late cycle. Companies showing the strongest revenue acceleration in fiscal year filings have often been accelerating for 2-3 years. They're concentrated in whatever sector led the prior cycle. When growth slows or the cycle turns, these are the first names to get hit — which explains the elevated down capture in most markets.

3. Quality filters compound the problem. Adding ROE > 10% and D/E < 1.5 selects for profitable accelerators — but it also selects for companies that are already well-known. The most interesting revenue acceleration opportunities (small companies early in their trajectory) get filtered out by the market cap floor.

What Works vs What Doesn't

The clearest pattern in the global results:

Better results correlate with lower down capture. Canada (44%), Germany (58.5%), and India (57.8%) are the three markets with the best defensive characteristics, and they're the three least-negative excess returns. Markets with down capture above 90% (US 109.6%, Switzerland 106.9%, Hong Kong 107.6%) all show severe underperformance.

Cash periods hurt. Sweden (24% cash), India (24%), Japan (20%), and Sweden again — these exchanges had years in the 2000-2005 period where fewer than 10 stocks qualified, meaning the portfolio sat in cash during strong bull markets. This structural problem is worse for emerging markets with thinner data coverage in the early years.

Smaller universes (like Germany at 18.4 avg stocks) aren't necessarily worse. Germany's tighter selection produced better drawdown characteristics than larger, more liquid markets. The quality filter does more work when the universe is naturally smaller.

Limitations

Benchmark is SPY for all exchanges. This comparison treats all 12 exchanges against the same USD benchmark. Currency effects are not neutralized. In periods of significant USD appreciation or depreciation, the comparison changes materially.

25 years per exchange, but start quality varies. Exchanges with thin early-period data (India, Japan, Korea, Taiwan) have more cash periods in 2000-2006. A fair comparison would start each exchange from when data coverage reached consistent levels — which would typically improve Asian market results modestly.

Survivorship bias. All exchanges use current listings. Companies that delisted during the period aren't tracked through failure.

SPY as benchmark for non-US exchanges is imperfect. A local benchmark (NIFTY for India, DAX for Germany, TSX Composite for Canada) would show different excess return calculations. We use SPY for cross-market comparability.

Takeaway

Revenue acceleration underperforms in 11 of 12 markets we tested. Canada is the lone exception at +0.29% annual excess, and that margin isn't large enough to claim statistical significance.

The signal isn't worthless everywhere. In Western markets like Canada and Germany, it produces portfolios with real downside protection characteristics — just not positive alpha. In developed Asian markets, the underperformance is larger and more consistent.

As a standalone strategy, revenue acceleration doesn't work globally. As a secondary filter in a multi-factor model, or as a screen for building defensively positioned portfolios in specific markets, the historical characteristics are worth knowing.

Individual Market Deep Dives

- [US] — 3.76% CAGR, -3.54% excess. The flagship failure: 109.6% down capture, three catastrophic years (2011, 2019, 2021).

- Canada — 7.60% CAGR, +0.29% excess. The lone outperformer with 44% down capture.

- Germany — 6.00% CAGR, -1.30% excess. Best max drawdown in the study (-29.91%).

References

- Chan, L., Karceski, J., & Lakonishok, J. (1996). "Momentum Strategies." Journal of Finance, 51(5), 1681–1713.

- Lakonishok, J., Shleifer, A., & Vishny, R. (1994). "Contrarian Investment, Extrapolation, and Risk." Journal of Finance, 49(5), 1541–1578.

Data: Ceta Research, FMP financial data warehouse. 12 exchanges, annual rebalance (April), equal weight, transaction costs included, 2000–2025.

Past performance does not guarantee future results. This is educational content, not investment advice.