R&D Efficiency Backtest (India/NSE): 7.41% CAGR vs Sensex 12.06%, 56% Cash

The R&D efficiency screen on NSE-only sits in cash for 56% of years. When invested (2014-2024), it produced volatile results with two spectacular years (2014 +58% vs Sensex, 2023 +91% vs Sensex). But the 25-year CAGR of 7.41% trails the Sensex''s 12.06%. The screen finds India''s best pharma and...

The R&D efficiency screen on NSE has a thin qualifying universe. The strategy held cash in 14 of 25 years, from 2000 through 2013, fewer than 10 NSE stocks passed all filters simultaneously. When the screen finally found stocks (2014 onward), it delivered some extraordinary years: 2014 (+57.72% vs Sensex +8.14%), 2023 (+91.44% vs Sensex +21.83%). But the full 25-year CAGR is 7.41% vs Sensex 12.06%. The strategy underperforms its own market by 4.65pp annually.

Contents

- Method

- What We Found

- A thin universe, a volatile active period

- Why the sector composition drives the returns

- Why results changed from the previous version

- Full returns (all 25 years)

- Performance summary

- The Screen

- Limitations

- Takeaway

The honest version of this result: the screen works in India when it has enough qualifying companies to hold. But the 56% cash rate means it's only invested about half the time, and the active-period record is volatile. The two spectacular years (2014, 2023) prop up the compounded return, while 2017 (-18.3% excess), 2021 (-15.1% excess), and 2018 (-12.1% excess) are the drags.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: NSE only, market cap above exchange-specific threshold (₹20B, roughly $240M USD) Period: 2000–2024 (25 annual rebalance periods; active 2014–2024) Rebalancing: Annual (July), equal weight top 30 by R&D efficiency Execution: Next-day close (MOC, signal from prior close, entry at following close) Benchmark: Sensex (^BSESN, BSE Sensex 30 index) Cash rule: Hold cash if fewer than 10 stocks qualify

Filters:

| Criterion | Threshold | Rationale |

|---|---|---|

| R&D / Revenue | 2–30% | Real R&D investment, not negligible or excessive |

| Gross Margin | > 40% | Excludes hardware, manufacturing, commodity companies |

| ROE | > 10% | Quality floor |

| Ranking signal | Gross Profit / R&D Expenses | Higher = more output per R&D dollar |

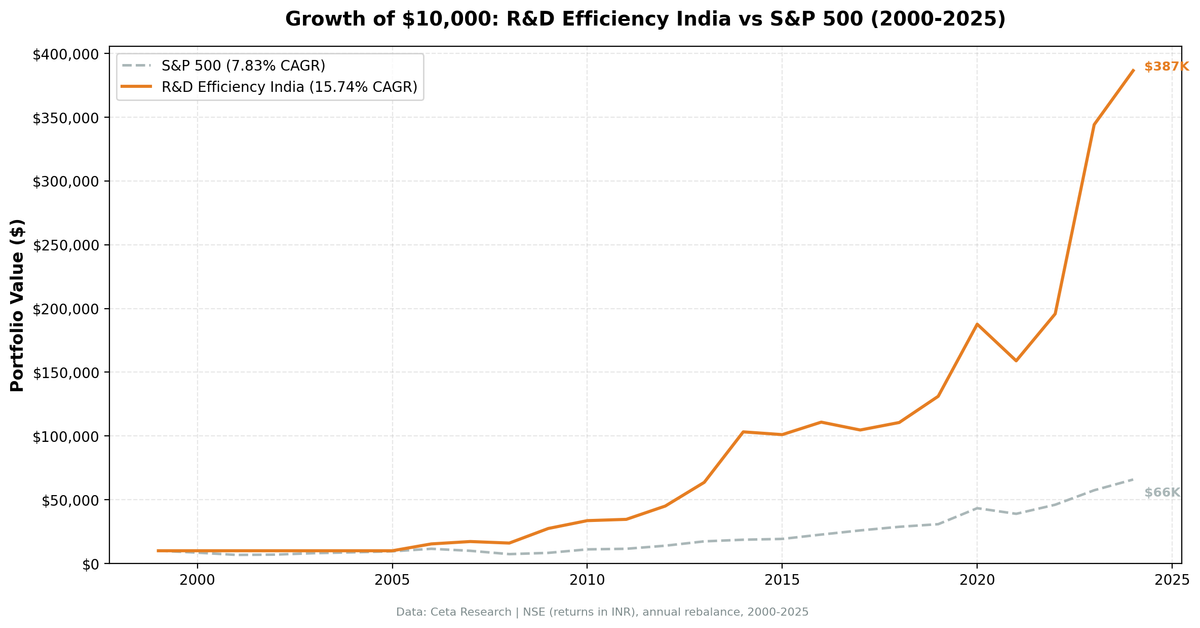

Universe note: NSE-only. BSE was removed due to significant dual-listing overlap with NSE (estimated 38% duplication), which inflated portfolio counts and introduced position duplicates in earlier versions of this backtest. The previous version (BSE+NSE combined) produced 15.74% CAGR vs SPY, but that result used SPY as the benchmark and included the dual-listing duplication. The NSE-only results here are more accurate.

Data availability: FMP's NSE R&D expense data is thin before 2014 for the specific combination of filters used. The strategy held 100% cash from 2000–2013 (14 years). The active period is 2014–2024, eleven years.

Transaction costs: size-tiered (0.1% for market cap > ₹equivalent of $10B, 0.3% for $2–10B, 0.5% below $2B), one-way. Full methodology: backtests/METHODOLOGY.md

What We Found

A thin universe, a volatile active period

The core problem on NSE is that the qualifying universe is small. The R&D efficiency screen requires R&D spending of 2-30% of revenue, gross margins above 40%, and ROE above 10%. On NSE, this combination is met by a small set of pharma and IT companies. Before 2014, fewer than 10 companies met all criteria simultaneously.

When the strategy became active in 2014, it delivered its best single year immediately: +57.72% vs Sensex +8.14%. Then came three rough years (2016-2018) of sustained underperformance, followed by recovery in 2019 and the spectacular 2023 (+91.44% vs Sensex +21.83%).

The active-period record (2014-2024, 11 years):

| Year | Portfolio | Sensex | Excess |

|---|---|---|---|

| 2014 | +57.72% | +8.14% | +49.58% |

| 2015 | -1.83% | -2.39% | +0.56% |

| 2016 | +6.65% | +14.45% | -7.80% |

| 2017 | -5.37% | +12.95% | -18.32% |

| 2018 | +0.86% | +12.91% | -12.05% |

| 2019 | +11.06% | -9.98% | +21.04% |

| 2020 | +49.87% | +46.43% | +3.45% |

| 2021 | -13.70% | +1.43% | -15.13% |

| 2022 | +22.68% | +22.49% | +0.19% |

| 2023 | +91.44% | +21.83% | +69.61% |

| 2024 | +12.22% | +5.00% | +7.22% |

Win rate in active period: 7 out of 11 years, 63%. But the losses in 2017 (-18.3% excess) and 2021 (-15.1% excess) are large, and the strategy trails the Sensex overall.

Why the sector composition drives the returns

India's NSE is dominated by pharma and IT services companies that pass the R&D efficiency screen: Sun Pharma, Dr. Reddy's, Cipla, Lupin, TCS, Infosys, Wipro, HCL Technologies. These companies have gross margins above 40%, R&D spending in the 5-15% range, and consistent ROE.

When these sectors perform well, the strategy does well. When they lag, there's no diversification to compensate. 2017-2018 saw Indian pharma companies dealing with USFDA import alerts and regulatory delays, the companies that dominate the screen were underperforming the broader market. 2021 saw post-COVID mean reversion in pharma names.

The 2023 result (+91.44%) was exceptional. A combination of Sun Pharma, Dr. Reddy's, and HCL Technologies having strong years drove returns well above the Sensex. This kind of concentrated sector performance can be very good or very bad depending on the year.

Why results changed from the previous version

The previous version of this backtest (using BSE+NSE combined, SPY as benchmark) showed 15.74% CAGR vs SPY's 7.83%, and only 24% cash periods. Three things changed:

1. Universe: BSE+NSE → NSE only. Removing BSE eliminated significant dual-listing duplication. This reduced the qualifying count below the minimum threshold in more years, increasing cash periods from 24% to 56%.

2. Benchmark: SPY → Sensex. India's equity market has compounded at 12.06% CAGR (Sensex) over this period. Comparing Indian returns to SPY understated the local market's performance.

3. Execution: Same-day entry → next-day close (MOC). This removed the same-bar entry bias.

All three changes move in the direction of accuracy. The 15.74% vs SPY number was real, but it wasn't the right comparison. The Sensex is the right benchmark for an Indian equity strategy.

Full returns (all 25 years)

| Year | Portfolio | Sensex | Excess |

|---|---|---|---|

| 2000–2013 | 0.00% (cash) | various | — |

| 2014 | +57.72% | +8.14% | +49.58% |

| 2015 | -1.83% | -2.39% | +0.56% |

| 2016 | +6.65% | +14.45% | -7.80% |

| 2017 | -5.37% | +12.95% | -18.32% |

| 2018 | +0.86% | +12.91% | -12.05% |

| 2019 | +11.06% | -9.98% | +21.04% |

| 2020 | +49.87% | +46.43% | +3.45% |

| 2021 | -13.70% | +1.43% | -15.13% |

| 2022 | +22.68% | +22.49% | +0.19% |

| 2023 | +91.44% | +21.83% | +69.61% |

| 2024 | +12.22% | +5.00% | +7.22% |

Performance summary

| Metric | Portfolio | Sensex |

|---|---|---|

| CAGR (full 25 years) | 7.41% | 12.06% |

| Total return | 497% | ~1,700% |

| Max drawdown | -13.70% | — |

| Avg stocks held (when invested) | 22.1 | — |

| Cash periods | 56% (14 of 25 years) | — |

| Sharpe ratio | 0.039 | — |

$10,000 invested in 2000 would have grown to approximately $59,700 in the portfolio vs approximately $180,000 in the Sensex over the same 25 years. Returns in INR.

The Sharpe ratio (0.039) reflects the very low excess return (negative) and the cash drag. The max drawdown of -13.70% is the drawdown measured from peak during active years; the strategy's cash periods are not losses.

The Screen

Run this on the NSE universe to see today's top R&D efficiency stocks:

WITH inc AS (

SELECT symbol, revenue, grossProfit, researchAndDevelopmentExpenses,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM income_statement

WHERE period = 'FY'

AND revenue > 0

AND grossProfit > 0

AND researchAndDevelopmentExpenses > 0

)

SELECT

inc.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(inc.researchAndDevelopmentExpenses / inc.revenue * 100, 1) AS rd_ratio_pct,

ROUND(inc.grossProfit / inc.revenue * 100, 1) AS gross_margin_pct,

ROUND(inc.grossProfit / inc.researchAndDevelopmentExpenses, 2) AS rd_efficiency,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM inc

JOIN profile p ON inc.symbol = p.symbol

JOIN key_metrics_ttm k ON inc.symbol = k.symbol

WHERE inc.rn = 1

AND inc.researchAndDevelopmentExpenses / inc.revenue > 0.02

AND inc.researchAndDevelopmentExpenses / inc.revenue < 0.30

AND inc.grossProfit / inc.revenue > 0.40

AND k.returnOnEquityTTM > 0.10

AND k.marketCap > 1000000000

AND p.exchange = 'NSE'

ORDER BY rd_efficiency DESC

LIMIT 30

Run this query on Ceta Research

Limitations

Currency risk. Returns are in INR. The INR has lost roughly 3-4% annually against USD over long periods. For a USD-based investor, this reduces the effective CAGR.

Thin qualifying universe. The strategy held cash for 14 of 25 years on NSE-only data. This isn't a data artifact, the NSE simply has fewer companies meeting all three criteria simultaneously than BSE+NSE combined. A lower gross margin threshold or lower R&D ratio would expand the universe but change the signal.

Sector concentration. The portfolio is heavily concentrated in pharma and IT services. Both sectors can underperform for multi-year periods (2016-2018 for pharma regulatory issues, 2021 for post-COVID mean reversion). There's no defensive diversification when these sectors lag.

Previous version used wrong benchmark. The prior published version compared Indian returns to SPY. This was misleading, India's market returned 12.06% CAGR (Sensex) over this period. The Sensex is the correct local benchmark. This correction significantly changes the narrative.

Look-ahead bias mitigation. The 45-day point-in-time lag prevents use of financial data before it was publicly reported. Survivorship bias from the current profile table is partially present.

Takeaway

The R&D efficiency screen on NSE finds real companies with real competitive advantages: Indian pharma generics with 60-70% gross margins, IT services companies with consistent R&D in platforms and delivery automation. In years when these sectors lead (2014, 2023), the strategy produces extraordinary returns.

The problem is the qualifying universe is too thin for consistent deployment. 56% cash rate means the strategy is idle for most of the period, and the Sensex compounded at 12.06% during years when the strategy was sitting in cash.

The screen is worth running to identify India's most R&D-efficient pharma and IT companies. But as a full-period systematic strategy against a Sensex benchmark, the current version doesn't generate net alpha.

Full backtest code: github.com/ceta-research/backtests

Data: Ceta Research (FMP financial data warehouse). Returns are in Indian Rupees (INR). Currency risk applies for non-INR investors. Benchmark: BSE Sensex 30 (^BSESN). Past performance does not guarantee future results.