Beat Earnings, Stock Still Drops 5%: What Happens Next in 12 Markets

18,925 beat-and-dip events across 12 exchanges with local benchmarks. Taiwan: +2.20%** at T+21. UK: +1.33%** (new). China: +2.35%** at T+63 (new). US: -0.85%** (continues falling). India lost its signal when measured vs Sensex instead of a USD ETF.

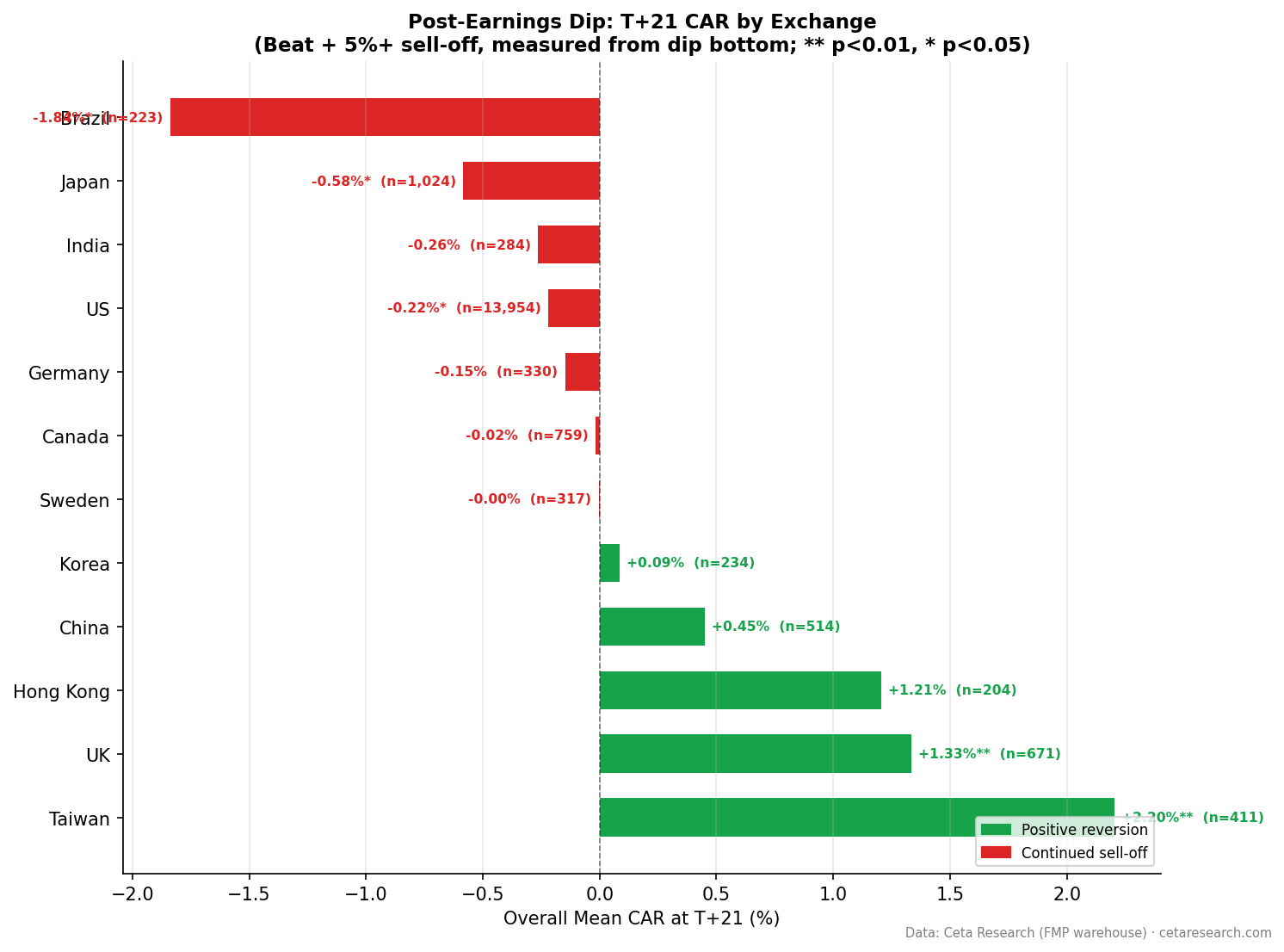

We ran a beat-and-dip event study on 12 exchanges, this time using local currency benchmarks instead of USD-denominated ETFs. The benchmark change matters. Three markets show significant positive reversion, four show significant negative drift, and five are noise.

Contents

- The Setup

- The Global Picture

- What's Statistically Significant

- The Five Noise Markets

- Data Quality Notes

- What the Benchmark Change Revealed

- Takeaway

The Setup

A "beat-and-dip" event is: 1. epsActual > epsEstimated with ABS(epsEstimated) > 0.01 2. Stock drops ≥ 5% from T-1 close to T+1 close (announcement reaction)

For each event, we measure cumulative abnormal return (CAR) at T+21 and T+63 trading days from T+1 close (the dip bottom). CAR = stock return minus local benchmark return over the same window. Each exchange uses its own currency-matched index: Sensex for India, TAIEX for Taiwan, Nikkei for Japan, FTSE for UK, and so on. US uses SPY.

Total events across 12 markets: 18,925

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

The Global Picture

| Exchange | Events | T+21 CAR | t-stat | T+63 CAR | t-stat | Benchmark | Data |

|---|---|---|---|---|---|---|---|

| Taiwan (TAI/TWO) | 411 | +2.20% | +3.75** | +3.88% | +3.40** | TAIEX | 2014–2025 |

| UK (LSE) | 671 | +1.33% | +3.01** | -0.38% | -0.49 | FTSE 100 | 2022–2025† |

| Hong Kong (HKSE) | 204 | +1.21% | +1.41 | -0.22% | -0.15 | Hang Seng | 2014–2025 |

| China (SHZ/SHH) | 514 | +0.45% | +0.87 | +2.35% | +2.78** | SSE Comp. | 2014–2025‡ |

| Korea (KSC) | 234 | +0.09% | +0.13 | -0.44% | -0.35 | KOSPI | 2014–2025 |

| Canada (TSX) | 759 | -0.02% | -0.04 | -0.82% | -1.12 | TSX Comp. | 2000–2025 |

| Sweden (STO) | 317 | ~0% | -0.01 | -2.08% | -2.08* | OMX 30 | 2014–2025 |

| Germany (XETRA) | 330 | -0.15% | -0.28 | -1.71% | -1.65 | DAX | 2015–2025 |

| India (NSE) | 284 | -0.26% | -0.49 | +1.57% | +1.68 | Sensex | 2021–2025† |

| US (NYSE/NASDAQ/AMEX) | 13,954 | -0.22% | -2.11* | -0.85% | -4.56** | S&P 500 | 2000–2025 |

| Japan (JPX) | 1,024 | -0.58% | -2.37* | -0.39% | -0.87 | Nikkei 225 | 2014–2025 |

| Brazil (SAO) | 223 | -1.84% | -2.45* | -1.98% | -1.35 | Bovespa | 2014–2025 |

p<0.05, p<0.01

†Effective coverage primarily post-2022 due to FMP pipeline timing. ‡China beat rate 32–36% vs 41–60% for other markets; interpret with care.

What's Statistically Significant

Seven markets now show significant results at one or both windows. The benchmark change from USD ETFs to local indices revealed patterns that were previously hidden by currency movements.

Significant positive (reversion):

Taiwan: The strongest result. +2.20% at T+21 (t=3.75), +3.88% at T+63 (t=3.40). Both significant at p<0.01. The 10–20% dip category is even stronger: +7.35%** at T+21. Taiwan's result actually improved with local benchmarking vs the earlier SPY comparison. This is the clearest case for mean reversion in the study.

UK: Positive at T+21 only. +1.33%** at T+21 (t=3.01). Disappears by T+63 (-0.38%, not significant). The UK result is new: it wasn't significant when measured against EWU (the iShares UK ETF). 671 events, but concentrated in 2022–2025. Treat this as a recent-period finding.

China: Delayed positive at T+63. +2.35%** at T+63 (t=2.78). Not significant at T+21. This is similar to the pattern India used to show, but with stronger statistical backing (514 events vs India's 284). China data carries its own caveats (low beat rate of 32–36%).

Significant negative (sell-off continues):

US: The benchmark. -0.22% at T+21 (t=-2.11), -0.85%* at T+63 (t=-4.56). Unchanged from the earlier study. 13,954 events over 25 years. The most credible result in the study.

Japan: Negative at T+21. -0.58%* at T+21 (t=-2.37). T+63 is -0.39% (not significant). Japan was previously flat at both windows when measured against EWJ. Measured against the Nikkei, the initial sell-off is informationally efficient: the first month produces significant underperformance.

Brazil: Negative at T+21. -1.84%* at T+21 (t=-2.45). Borderline before (t=-1.71 vs EWZ), now significant. T+63 is -1.98% (t=-1.35, not significant). Small sample (223 events).

Sweden: Negative at T+63. -2.08%* at T+63 (t=-2.08). Still significant, slightly reduced from the earlier -2.58% when measured against pan-European VGK.

The Five Noise Markets

Canada, Germany, Hong Kong, Korea, and India show no statistically significant result at either window.

India lost its signal. The earlier finding of +2.54%** at T+63 was measured against INDA, a USD-denominated ETF. Measured against the Sensex (local INR index) and with NSE-only data (BSE removed for dual-listing overlap), the result drops to +1.57% (t=1.68). Still positive direction, but below the significance threshold. The earlier significance was partly a benchmark artifact involving USD/INR movements. India data is also concentrated in 2022–2025 (93% of events).

Canada (n=759) is the longest-running noise market: 25 years of data, T+63 of -0.82% (t=-1.12). Consistently in the "slight negative" direction without reaching significance.

Germany (n=330) shows -1.71% at T+63 (t=-1.65), close to significance but not crossing the threshold.

Data Quality Notes

UK (LSE): 671 events concentrated in 2022–2025. The +1.33%** at T+21 is a recent-period result. FTSE 100's composition (energy-heavy, bank-heavy) may not match the mid-cap growth stocks generating beat-and-dip events.

India (NSE): 284 events, 93% from 2022 or later. BSE was removed to eliminate 38% dual-listing overlap. Benchmark changed from INDA to Sensex. Both changes reduce the sample and shift the baseline. The earlier +2.54%** result is not comparable to the current +1.57%.

China (SHZ/SHH): Beat rate of 32–36% vs 41–60% elsewhere. This could reflect conservative analyst forecasting norms, reporting practice differences, or data coverage gaps. The +2.35%** result at T+63 is statistically significant but should be interpreted with this context.

Excluded: Australia (adjClose data quality issues), Thailand, Norway, and Switzerland all had fewer than 100 qualifying events.

What the Benchmark Change Revealed

The shift from USD ETFs to local indices changed the picture more than expected.

Markets that got stronger: Taiwan improved from +1.76% to +2.20% at T+21. TAIEX is a harder benchmark than SPY for Taiwan stocks, but the excess return actually increased. This validates the Taiwan result: it's not a currency artifact.

Markets that gained significance: UK (+1.33% vs FTSE, was +0.44% vs EWU), China (+2.35% vs SSE, was +0.67% vs FXI), Japan (-0.58% vs Nikkei, was -0.26% vs EWJ), Brazil (-1.84% vs Bovespa, was -1.32% vs EWZ).

Markets that lost significance: India (+1.57% vs Sensex, was +2.54%** vs INDA). The INDA-based result incorporated USD/INR movements that inflated the apparent alpha.

The lesson: ETF benchmarks can mask or inflate abnormal returns. A Taiwanese investor holding TAIEX, not SPY, as their baseline was beating the market by more than the ETF comparison suggested. An Indian investor comparing to Sensex, not INDA, had less alpha than it appeared.

Takeaway

"Buy the beat-and-dip" works in three markets and fails in four. Taiwan is the clearest positive result. UK shows short-term reversion (T+21 only, recent data). China shows delayed reversion at T+63 (with beat-rate caveats). Five markets show nothing.

The sell-off is informative in the US, Japan, Brazil, and Sweden. The market's negative reaction to a genuine earnings beat in those markets typically contains real information about forward prospects. Buying against it has produced negative abnormal returns on average.

Local benchmarks matter. Currency movements and ETF construction can hide real patterns or create false ones. The India result was a cautionary example: what looked like +2.54%** alpha was partly a benchmark artifact.

Data note: Results use local currency benchmarks (SPY for US, Sensex for India, Nikkei for Japan, TAIEX for Taiwan, etc.). Market cap floors applied per exchange. All CARs winsorized at 1st/99th percentile.

Part of a series: Post-earnings dip mean reversion tested globally. See individual market studies: US, Taiwan, India.

Data: FMP earnings surprises + adjusted prices, 2000–2025 (varies by exchange). 18,925 total beat-and-dip events across 12 exchanges. Local currency benchmarks.