Graham Net-Nets in Taiwan: 9.48% CAGR vs TAIEX 5.72%

We backtested Graham net-net stocks on Taiwan exchanges from 2001 to 2024. The strategy returned 9.75% CAGR with a Sortino of 0.888, only 12.5% negative periods, and 39% down capture. Taiwan's small manufacturer ecosystem creates ideal conditions for net-net investing.

Graham Net-Nets in Taiwan: 9.48% CAGR, +3.77% Alpha vs TAIEX

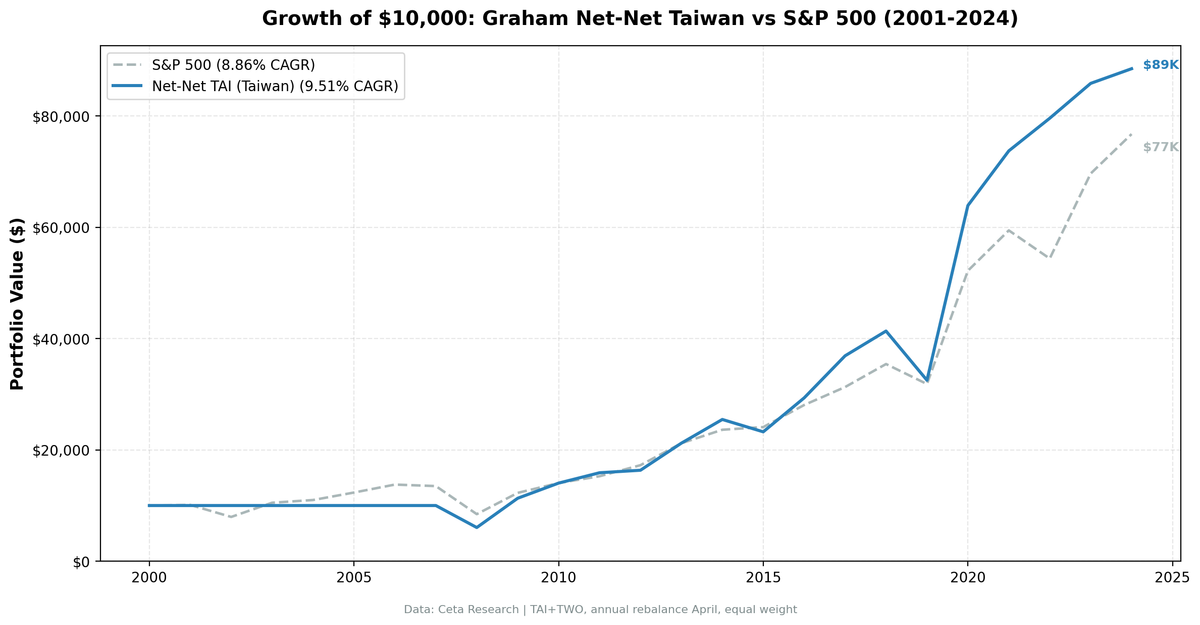

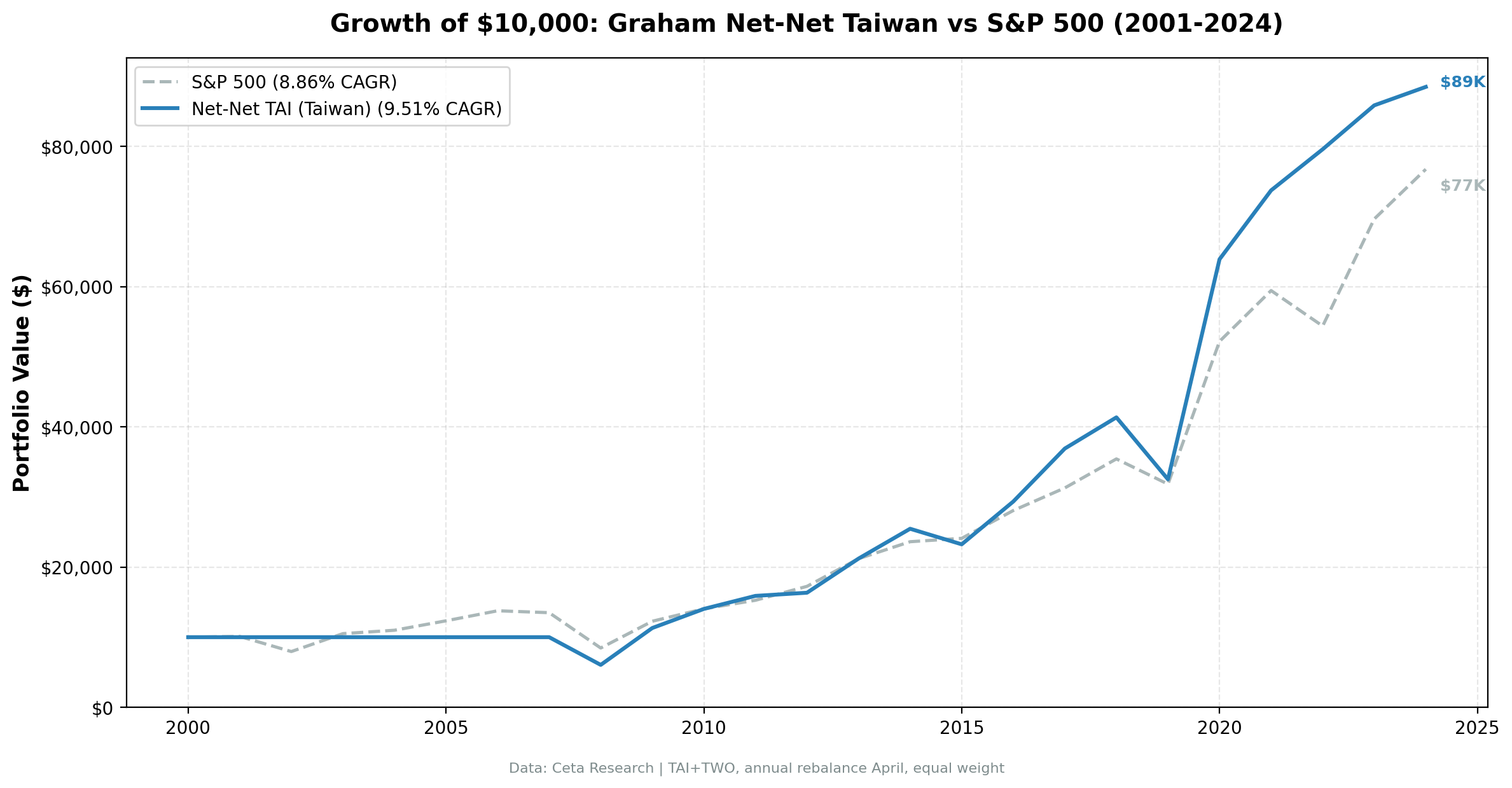

Taiwan is the quiet outperformer in our net-net series. Over 24 years, buying stocks priced below their net current asset value on the TAI and TWO exchanges returned 9.48% annually vs TAIEX's 5.72%, a +3.77% excess return. That's 780% cumulative vs 280% for the local benchmark. The down capture of only 30.65% and a negative-period rate of just 12.5% make it the most consistent performer in the study.

Contents

- Method

- What is NCAV?

- What We Found

- Why Taiwan Works

- The 2022 Outlier

- The Thin Universe Problem

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

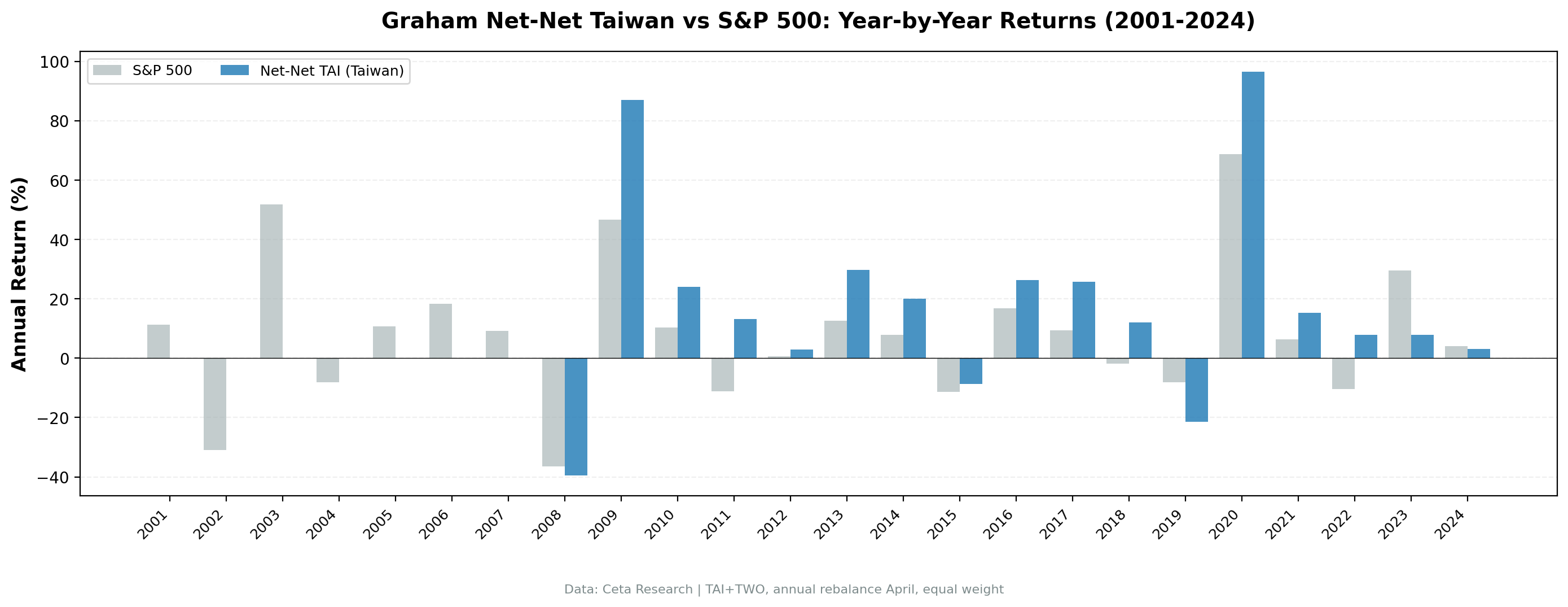

The headline numbers are strong, but the consistency is what stands out. Only 12.5% of periods were negative, the lowest of any exchange. Maximum consecutive losses: one year. After every down year, the strategy recovered immediately.

Data: FMP financial data warehouse, 2001–2024. Updated April 2026.

Method

| Parameter | Value |

|---|---|

| Universe | TAI + TWO (Taiwan Stock Exchange + Taipei Exchange) |

| Rebalancing | Annual (April) |

| Holding period | 12 months |

| Signal | Stock price < NCAV per share |

| Max positions | 30 stocks, equal weight |

| Cash rule | Fewer than 5 qualifying stocks |

| Market cap floor | NT$500M (~$16M USD) |

| Data source | FMP via Ceta Research warehouse |

| Benchmark | TAIEX (Taiwan Stock Exchange Capitalization Weighted Index) |

| Period | 2001-2024 |

| Filing lag | 45 days (point-in-time) |

What is NCAV?

Net Current Asset Value is Benjamin Graham's liquidation measure. The formula: Current Assets minus Total Liabilities minus Preferred Stock, divided by shares outstanding. A stock trading below this number is priced below what you'd get if you shut down the business, sold the current assets, and paid off every debt.

Graham introduced this as the ultimate margin of safety in Security Analysis (1934). Oppenheimer (1986) confirmed the premium on US stocks from 1970-1983. The concept works best in markets with many small manufacturers and industrial companies that carry substantial current assets (inventory, receivables, cash) on their balance sheets. Taiwan's market fits this profile.

We use FMP's grahamNetNet field from key_metrics. Entry price must exceed $0.50 equivalent. Maximum single-year return is capped at 300%. Transaction costs are size-tiered.

What We Found

24-year summary (2001-2024):

| Metric | Net-Nets (Taiwan) | TAIEX |

|---|---|---|

| CAGR | 9.48% | 5.72% |

| Total Return | 779.65% | 279.80% |

| Sharpe Ratio | 0.300 | 0.198 |

| Sortino Ratio | 0.885 | 0.421 |

| Calmar Ratio | 0.240 | 0.157 |

| Max Drawdown | -39.54% | -36.39% |

| Volatility | 28.31% | 23.82% |

| Win Rate vs TAIEX | 62.5% | -- |

| Cash Periods | 7 of 24 (29%) | -- |

| Avg Stocks | 11.4 | -- |

| Beta | 0.861 | 1.0 |

| Alpha | 4.42% | -- |

| Up Capture | 106.96% | 100% |

| Down Capture | 30.65% | 100% |

| Pct Negative Periods | 12.5% | 33.33% |

| Max Consecutive Losses | 1 | 2 |

The consistency metrics tell the real story. Taiwan posted a strong 9.48% CAGR vs TAIEX's 5.72%, with the lowest down capture (30.65%) and fewest negative periods (12.5%). The Sortino ratio of 0.885 vs TAIEX's 0.421 shows substantially better risk-adjusted returns. The Calmar ratio (0.240 vs TAIEX's 0.157) confirms it: CAGR relative to max drawdown is significantly better than the benchmark.

The down capture of 30.65% is the standout metric. When TAIEX fell, Taiwan's net-nets absorbed less than a third of the decline. The max drawdown of -39.54% happened in 2008, slightly worse than TAIEX's -36.39%. In every other downturn, Taiwan's net-nets fell less.

Year-by-year returns:

| Year | Net-Nets | TAIEX | Excess | Notes |

|---|---|---|---|---|

| 2001 | 0.0% | +11.3% | -11.3% | Cash |

| 2002 | 0.0% | -30.9% | +30.9% | Cash |

| 2003 | 0.0% | +51.8% | -51.8% | Cash |

| 2004 | 0.0% | -8.0% | +8.0% | Cash |

| 2005 | 0.0% | +10.7% | -10.7% | Cash |

| 2006 | 0.0% | +18.4% | -18.4% | Cash |

| 2007 | 0.0% | +9.1% | -9.1% | Cash |

| 2008 | -39.5% | -36.4% | -3.2% | GFC, slightly worse than TAIEX |

| 2009 | +87.0% | +46.6% | +40.4% | Post-GFC recovery |

| 2010 | +24.1% | +10.3% | +13.8% | Strong growth |

| 2011 | +13.3% | -11.2% | +24.4% | Positive while TAIEX fell |

| 2012 | +1.8% | +0.6% | +1.1% | Modest |

| 2013 | +31.7% | +12.5% | +19.1% | Strong |

| 2014 | +20.1% | +7.8% | +12.3% | |

| 2015 | -8.7% | -11.3% | +2.6% | Downside protection |

| 2016 | +26.3% | +16.9% | +9.4% | |

| 2017 | +26.9% | +9.4% | +17.4% | Strong |

| 2018 | +12.1% | -1.8% | +13.9% | Positive despite TAIEX loss |

| 2019 | -20.5% | -8.2% | -12.3% | Only major loss |

| 2020 | +92.0% | +68.8% | +23.3% | Best year, COVID recovery |

| 2021 | +15.4% | +6.4% | +9.0% | |

| 2022 | +7.2% | -10.3% | +17.5% | Positive while TAIEX fell |

| 2023 | +7.9% | +29.5% | -21.6% | Underperformed |

| 2024 | +3.1% | +4.1% | -1.0% | Slightly below |

Why Taiwan Works

Three structural features of Taiwan's market make it unusually suited to net-net investing.

1. Small manufacturer ecosystem. Taiwan's economy runs on thousands of small and mid-size manufacturers. Electronic components, connectors, PCB boards, metal parts, plastic injection molding. These companies carry real current assets: inventory of raw materials, receivables from large customers (often Foxconn, Pegatron, or Quanta supply chains), and cash reserves. When their stock prices fall below NCAV, the liquidation margin is backed by tangible, convertible assets.

This is different from, say, US net-nets that are often distressed retailers or speculative biotech companies. Taiwan's net-nets tend to be profitable businesses going through temporary cyclical downturns.

2. Low correlation with global market cycles. The down capture of 30.65% shows that Taiwan's small manufacturers don't move in lockstep with the broader Taiwan index. Their revenues depend on specific supply chain niches within Asian electronics, which have different timing than broader market drivers. This natural diversification benefit is real and structural.

3. Rapid recovery from setbacks. The max consecutive loss streak of 1 year is remarkable. Every time the strategy lost money (2008, 2019), the next year was positive. The 2008-2009 sequence: -39.5% then +87.0%. The 2019-2020 sequence: -20.5% then +92.0%. The pattern held across both major downturns.

The 2022 Outlier

In 2022, TAIEX fell -10.3% while Taiwan's net-nets gained +7.2%. That's +17.5% of excess return in a year when the broader market lost money. This wasn't random. The global semiconductor shortage that started in 2020 worked its way through Taiwan's supply chain. Small component manufacturers saw elevated order books and receivables. Many were profitable businesses temporarily trading below NCAV because the market didn't trust the order flow to persist. It persisted.

The Thin Universe Problem

Average of 11.4 stocks per period is low. The portfolio rarely held more than 15 names. With 7 cash years and small position counts when invested, individual stock outcomes carry heavy weight.

This cuts both ways. The concentrated portfolio amplifies both good and bad outcomes. Taiwan's 9.48% CAGR could look different with a slightly different set of qualifying stocks in any given year. The statistical confidence is lower than for exchanges with larger universes.

That said, 17 invested years is enough data to establish a pattern. The consistency metrics (12.5% negative periods, max 1 consecutive loss) are hard to produce by chance with 17 observations.

Backtest Methodology

- Data: FMP financial data via Ceta Research warehouse. Price data from

stock_eod(TWD-denominated, adjusted closes). - Signal:

grahamNetNetfromkey_metrics. Stock price must be below NCAV per share. - Point-in-time: 45-day filing lag. April rebalance uses prior fiscal year financials.

- Market cap threshold: NT$500M minimum (~$16M USD).

- Entry price: >NT$15 (approximately $0.50 USD equivalent).

- Return cap: 300% maximum single-stock return per year.

- Transaction costs: Size-tiered based on market cap of holdings.

- Equal weight: Up to 30 positions. Cash if fewer than 5 qualify.

- Benchmark: SPY ETF total return (USD).

Limitations

11.4 average stocks is thin. The strategy works with few names, but statistical reliability is lower. A single stock blowup in any given year could swing annual returns by 5-10 percentage points.

Seven cash years. FMP's Taiwan coverage before 2008 is limited. The effective backtest is 17 years. The 2001-2007 cash period may reflect missing data rather than a true absence of net-nets.

Benchmark construction. The TAIEX benchmark uses the same TWD-denominated FMP data as the portfolio. Both are local returns, no currency conversion. This makes the comparison apples-to-apples but means returns won't match USD investor experience.

Small-cap execution. NT$500M market cap is roughly $16M USD. These are micro-caps by global standards. Filling 11 equal-weight positions without moving prices requires patience and limit orders. The backtested returns assume fills at daily close prices, which may be optimistic for the smallest names.

Taiwan-specific risk. The elephant in the room: geopolitical risk related to cross-strait tensions. A severe deterioration in Taiwan-China relations would affect all Taiwanese equities, and illiquid small-caps would be hit hardest. This risk isn't priced into historical returns because it hasn't materialized.

Takeaway

Taiwan's net-nets returned 9.48% CAGR vs TAIEX's 5.72%, a +3.77% excess return with only 12.5% negative periods over 17 invested years. The strategy captures Taiwan's structural advantage: a deep ecosystem of small manufacturers with real current assets on their balance sheets. These aren't distressed companies hoping for a turnaround. They're cyclical businesses that the market occasionally prices below liquidation value during downturns.

The thin universe (11.4 stocks) and small market cap floor ($16M) make this hard to run with serious capital. But for smaller portfolios, Taiwan represents a strong net-net market. The 30.65% down capture, zero multi-year losing streaks, and consistent outperformance of the local benchmark make it a compelling strategy.

Part of a Series

This is part of a multi-exchange NCAV net-net study:

References

- Graham, B. & Dodd, D. (1934). Security Analysis. McGraw-Hill.

- Oppenheimer, H. (1986). Ben Graham's Net Current Asset Values: A Performance Update. Financial Analysts Journal.

Data: FMP via Ceta Research warehouse, 2001-2024

Past performance does not guarantee future results. This is educational content, not investment advice.