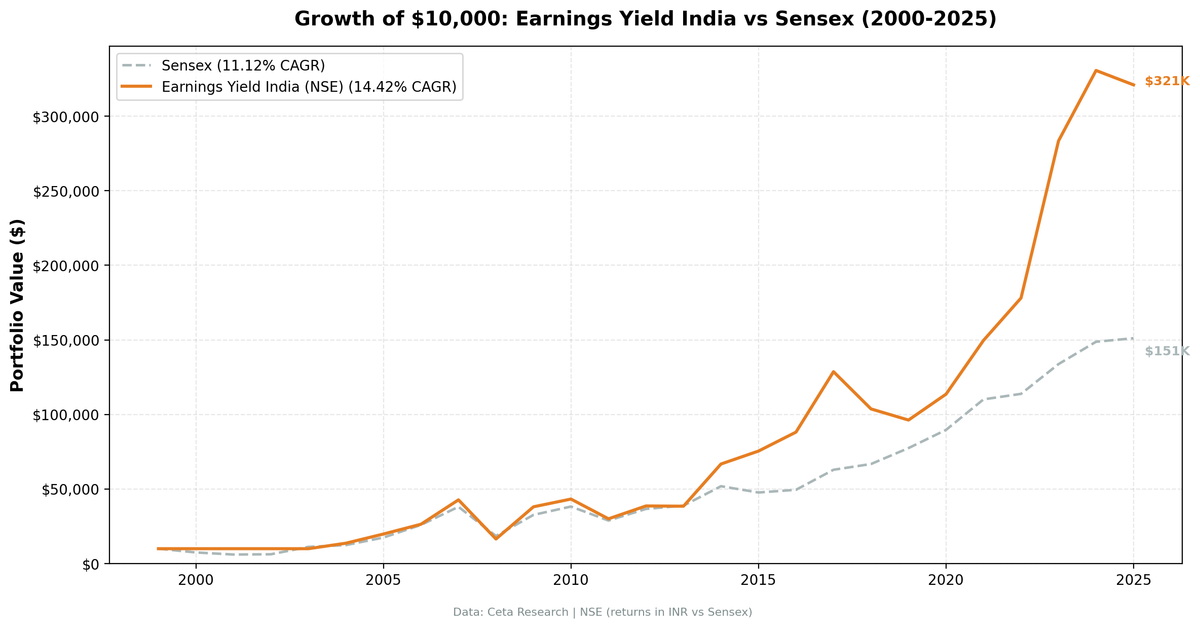

Earnings Yield on Indian Stocks: 14.4% CAGR, +3.3% Annual Excess vs Sensex

Earnings yield screening on NSE returned 14.42% CAGR vs 11.12% for the Sensex. +3.30% annual excess with 57.3% quarterly win rate. Returns in INR, max drawdown -61.4%.

Earnings Yield on Indian Stocks: 14.4% CAGR, +3.3% Excess vs Sensex (NSE)

Earnings yield screening on NSE (National Stock Exchange of India) produced 14.42% CAGR over 21 effective years, compared to 11.12% CAGR for the Sensex over the same period. That's +3.30% annual excess against the local benchmark. For context, the same strategy on US exchanges returned just +0.90% excess vs the S&P 500.

Contents

- Method

- The Screen (SQL)

- Results

- The 2000-2003 Cash Period

- Year-by-Year Returns

- Why India Works

- The Currency Question

- Limitations

The catch: returns are in Indian Rupees, max drawdown hit -61.4%, and the strategy held cash for the first four years while India's qualifying universe was too thin.

Data: FMP financial data warehouse, 2000–2025. Updated June 2026.

Method

Signal: Same as our US earnings yield backtest: - Earnings yield > 0% (positive earnings) - ROE > 12% - Debt/Equity < 1.5 - Interest coverage > 3x - Market cap > ₹20B (~$240M USD)

Portfolio: Top 50 by highest earnings yield, equal weight, quarterly rebalance Transaction costs: Size-tiered model (0.1-0.3% per trade) Period: 2000-2025 (103 quarters, effectively invested from 2004) Benchmark: Sensex (INR), the local index, consistent with the exchange Universe: NSE only (BSE excluded due to dual-listing duplication)

For the full methodology and quality filter rationale, see the US Earnings Yield post.

The Screen (SQL)

WITH km AS (

SELECT k.* FROM key_metrics_ttm k

JOIN (SELECT symbol, MAX(fetchedAtEpoch) AS max_e FROM key_metrics_ttm GROUP BY symbol) lat

ON k.symbol = lat.symbol AND k.fetchedAtEpoch = lat.max_e

),

fr AS (

SELECT f.* FROM financial_ratios_ttm f

JOIN (SELECT symbol, MAX(fetchedAtEpoch) AS max_e FROM financial_ratios_ttm GROUP BY symbol) lat

ON f.symbol = lat.symbol AND f.fetchedAtEpoch = lat.max_e

)

SELECT

k.symbol,

ROUND(k.earningsYieldTTM * 100, 2) AS ey_pct,

ROUND(r.priceToEarningsRatioTTM, 1) AS pe,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(r.debtToEquityRatioTTM, 2) AS de,

ROUND(r.interestCoverageRatioTTM, 1) AS ic,

ROUND(k.marketCap / 1e9, 1) AS mktcap_bn,

p.sector

FROM km k

JOIN fr r ON k.symbol = r.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE k.earningsYieldTTM > 0.08

AND k.earningsYieldTTM < 1.0

AND r.priceToEarningsRatioTTM > 3

AND r.priceToEarningsRatioTTM < 100

AND k.returnOnEquityTTM > 0.12

AND r.debtToEquityRatioTTM >= 0

AND r.debtToEquityRatioTTM < 1.5

AND r.interestCoverageRatioTTM > 3

AND k.marketCap > 20000000000

AND p.exchange IN ('NSE')

QUALIFY ROW_NUMBER() OVER (PARTITION BY p.companyName ORDER BY k.marketCap DESC) = 1

ORDER BY k.earningsYieldTTM DESC

LIMIT 50

Run this screen on Ceta Research →

Results

| Metric | Earnings Yield India | Sensex |

|---|---|---|

| CAGR | 14.42% | 11.12% |

| Total Return | 3,109% | 1,411% |

| Max Drawdown | -61.4% | -51.3% |

| Volatility | 26.9% | 23.8% |

| Sharpe Ratio | 0.295 | 0.194 |

| Sortino Ratio | 0.517 | 0.318 |

| Excess CAGR vs Sensex | +3.30% | - |

| Win Rate (quarterly) | 57.3% | - |

| Avg Stocks per Quarter | 43.2 | - |

| Cash Quarters | 18/103 | - |

$10,000 invested in 2000 became roughly ₹3,21,000 in the earnings yield portfolio vs ₹1,51,000 in the Sensex (same starting amount, returns in INR from 2000 base).

The win rate of 57.3% is the metric that stands out. The strategy beat the Sensex in more than 5 out of every 9 quarters. That's a consistent edge, not a few outlier years inflating the average.

The 2000-2003 Cash Period

The screen held cash during 2000-2003 when India's qualifying universe was too thin. FMP's data coverage for Indian large-caps in this period didn't provide enough stocks meeting all four quality filters at the ₹20B market cap threshold.

Effective backtest history starts 2004. From 2004 through 2025, the strategy was invested in 85 of 85 applicable quarters.

During the cash years (2000-2003), the Sensex fell significantly in 2000-2001 and then surged +79.1% in 2003. The strategy missed that 2003 rally while in cash. This pulls down the relative performance. The honest excess return accounts for all 103 periods including cash.

Year-by-Year Returns

| Year | Portfolio (INR) | Sensex | Excess |

|---|---|---|---|

| 2004 | +36.8% | +10.8% | +26.0% |

| 2005 | +45.0% | +40.6% | +4.4% |

| 2006 | +33.1% | +48.5% | -15.4% |

| 2007 | +61.9% | +46.8% | +15.2% |

| 2008 | -61.4% | -51.3% | -10.1% |

| 2009 | +130.8% | +76.3% | +54.5% |

| 2010 | +13.6% | +17.1% | -3.5% |

| 2011 | -30.6% | -24.5% | -6.1% |

| 2012 | +28.7% | +27.0% | +1.6% |

| 2013 | -0.4% | +6.0% | -6.4% |

| 2014 | +73.5% | +33.5% | +40.0% |

| 2015 | +13.0% | -8.1% | +21.1% |

| 2016 | +16.8% | +3.8% | +13.0% |

| 2017 | +46.0% | +27.1% | +18.8% |

| 2018 | -19.4% | +6.2% | -25.6% |

| 2019 | -7.2% | +16.0% | -23.2% |

| 2020 | +18.0% | +15.7% | +2.3% |

| 2021 | +31.8% | +22.9% | +8.9% |

| 2022 | +19.0% | +3.4% | +15.6% |

| 2023 | +59.2% | +17.5% | +41.6% |

| 2024 | +16.7% | +11.2% | +5.5% |

| 2025 | -2.9% | +1.6% | -4.5% |

The strategy had clear winners: 2009 (+54.5% excess), 2023 (+41.6% excess), 2014 (+40.0% excess). And clear losers: 2018 (-25.6%), 2019 (-23.2%). When India's broader market ran hot in 2019, value companies were left behind.

2022 and 2023 stand out as the strategy's best recent stretch. While the Sensex returned just +3.4% in 2022 and +17.5% in 2023, the earnings yield screen delivered +19.0% and +59.2%. The post-COVID rotation toward cheap, quality companies drove strong alpha in both years.

Why India Works

Three structural advantages explain the outperformance.

Thicker value universe. Indian exchanges have more companies passing the quality and value filters. Average 43.2 stocks per quarter across the invested periods. More qualifying stocks means the top-50 selection is genuinely filtering a deep pool.

Less efficient pricing. Indian mid-caps are less covered by institutional analysts than US large-caps. The earnings yield signal has more room to work before it gets arbitraged away. Quality filters do more work here than in developed markets because overlooked companies stay overlooked longer.

Structural growth. India's economy grew faster than the US over this period. High-quality value companies in a growing economy compound earnings faster. The earnings yield screen captures this by selecting profitable companies at cheap valuations.

Compare to developed markets: UK beats FTSE 100 by +4.86%, but the FTSE 100 itself grew at just 1.36% CAGR. India's advantage is the combination of a strong local market AND excess return above it.

The Currency Question

All returns are in Indian Rupees. The Rupee lost roughly 60% of its value against the Dollar from 2000 to 2025. For a USD-based investor, the returns would be substantially lower after currency conversion. The 14.42% INR CAGR translates to roughly 11-12% in USD terms, still well above the S&P 500's 8.02%.

We use the Sensex as benchmark for this blog because it's the right local comparison: an Indian investor choosing this strategy vs. a Sensex index fund. The currency comparison to SPY is covered in the global comparison post.

Limitations

Currency risk. Returns in INR. For USD-based investors, currency effects reduce the effective return.

Early data gap. Cash 2000-2003 including missing the 2003 +79.1% Sensex rally. Effective history is 21 years.

Max drawdown: -61.4%. Deeper than the Sensex at -51.3%. This strategy amplifies both upside and downside.

Survivorship bias. Universe is based on current NSE membership. Companies that delisted may be underrepresented.

Data: Ceta Research (FMP financial data warehouse). Universe: NSE, market cap > ₹20B. Returns in Indian Rupees. Backtest uses historical financial_ratios, key_metrics, and stock_eod tables with point-in-time methodology and 45-day reporting lag. Transaction costs: size-tiered (0.1-0.3% one-way based on market cap). FMP data has known limitations: coverage varies by company and time period, some historical records may contain errors or gaps, and delisted company data is less complete than active companies. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.

Part of a series: This is the India edition of our earnings yield backtest. See also: Earnings Yield US | Earnings Yield Global Comparison