Dividend Growth on Swiss Stocks: Low Volatility, Positive Alpha (SIX Backtest)

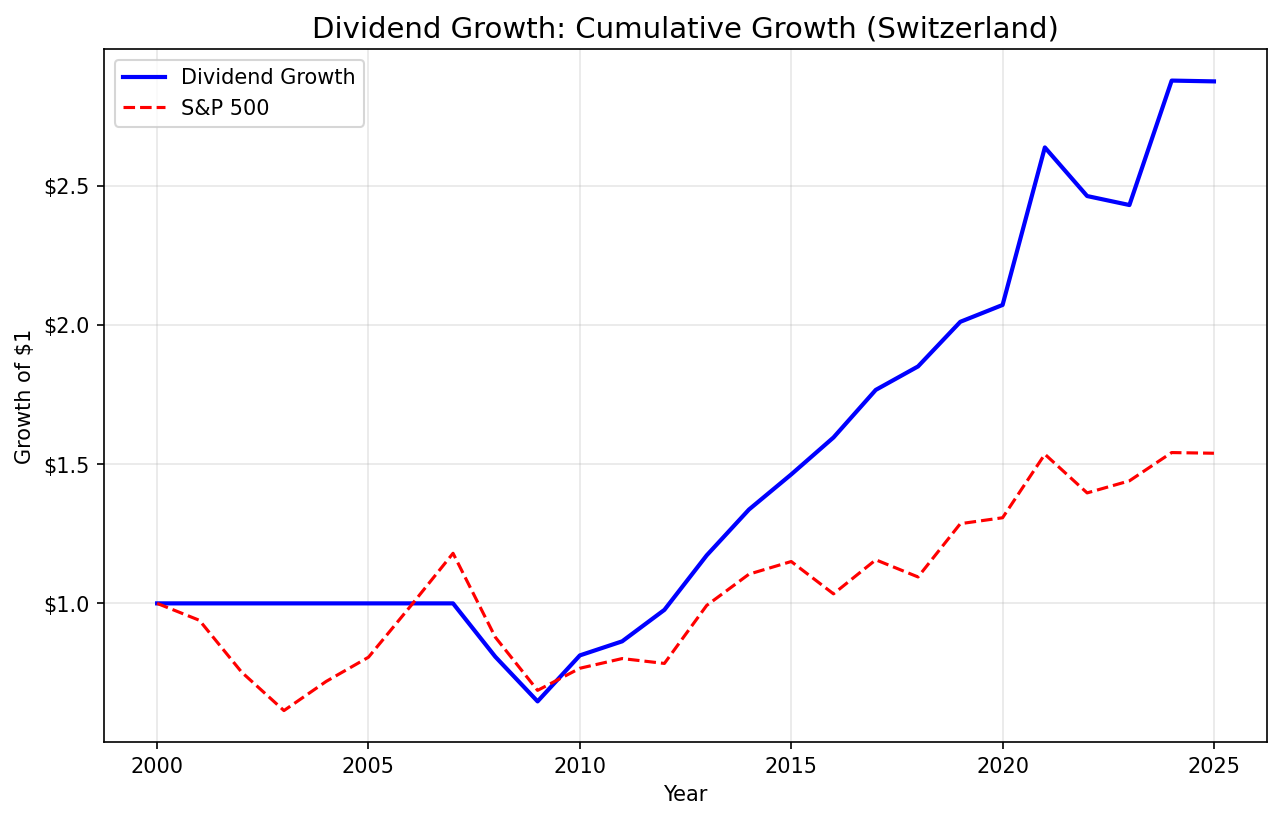

We ran a dividend growth screen on Swiss stocks (SIX). 4.31% CAGR vs 1.74% for the SMI, with the lowest volatility (11.32%) of any exchange tested. +2.57% annual alpha over the local benchmark.

Switzerland is home to some of Europe's most reliable dividend payers. Nestle, Novartis, Roche, ABB. These companies have built multi-decade payout traditions backed by strong free cash flow and conservative capital allocation. We screened SIX-listed stocks for 5+ consecutive years of rising dividends, then held the top 30 by streak length. The result: 4.31% CAGR vs 1.74% for the SMI. Total return of 186%. The strategy beats its local benchmark by +2.57% annually. And the volatility profile makes the case even stronger. At 11.32%, this is the lowest-volatility result of any exchange we tested. Beta of 0.431 means the portfolio moved at less than half the pace of the SMI. You're buying stability and modest local outperformance.

Contents

- Method

- Signal

- Results

- The Cash Period Story

- Annual Returns (Invested Years)

- When It Works

- When It Struggles

- Limitations

- Run This Screen (Switzerland)

- Takeaway

- Part of a Series

- References

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data) Universe: SIX Swiss Exchange stocks with market cap > CHF 500M Period: 2000-2025 (25 years, invested from 2007) Rebalancing: Annual (July)

Signal

| Filter | Threshold |

|---|---|

| Consecutive dividend increases | >= 5 years |

| Payout ratio | 0% to 80% |

| Free cash flow | > 0 |

| Market cap | > CHF 500M |

Portfolio: Top 30 by streak length, equal weight. Cash if fewer than 10 qualify.

For full methodology, see our US analysis.

Results

| Metric | Strategy | SMI |

|---|---|---|

| CAGR | 4.31% | 1.74% |

| Total Return | 186% | 54% |

| Max Drawdown | -35.22% | -41.74% |

| Sharpe Ratio | 0.334 | 0.085 |

| Sortino Ratio | 0.661 | 0.131 |

| Calmar Ratio | 0.122 | -- |

| Win Rate (vs SMI) | 52% | -- |

| Up Capture | 59.13% | -- |

| Down Capture | 30.67% | -- |

| Beta | 0.431 | -- |

| Alpha | 1.53% | -- |

| Volatility | 11.32% | -- |

| Cash Periods | 7/25 (28%) | -- |

| Avg Stocks | 15.9 | -- |

The Sortino of 0.661 is five times the SMI's 0.131, showing far better risk-adjusted downside performance. Up capture of 59.13% vs down capture of 30.67% is the standout number: the portfolio captures most of the upside while blocking nearly 70% of the downside. With a beta of 0.431 and 1.53% annual alpha, you're holding a half-equity position that quietly compounds ahead of its benchmark.

The Cash Period Story

Seven cash periods (2000-2006) all fall at the start of the backtest window. FMP coverage for Swiss dividend data doesn't begin reliably until 2007. This is a data availability issue, not a signal failure. From 2007 onward, the strategy averaged 15.9 qualifying stocks per period. That's well below the 30-stock target, reflecting the smaller Swiss market. Fewer companies meet the five-year streak requirement, so the portfolio runs concentrated.

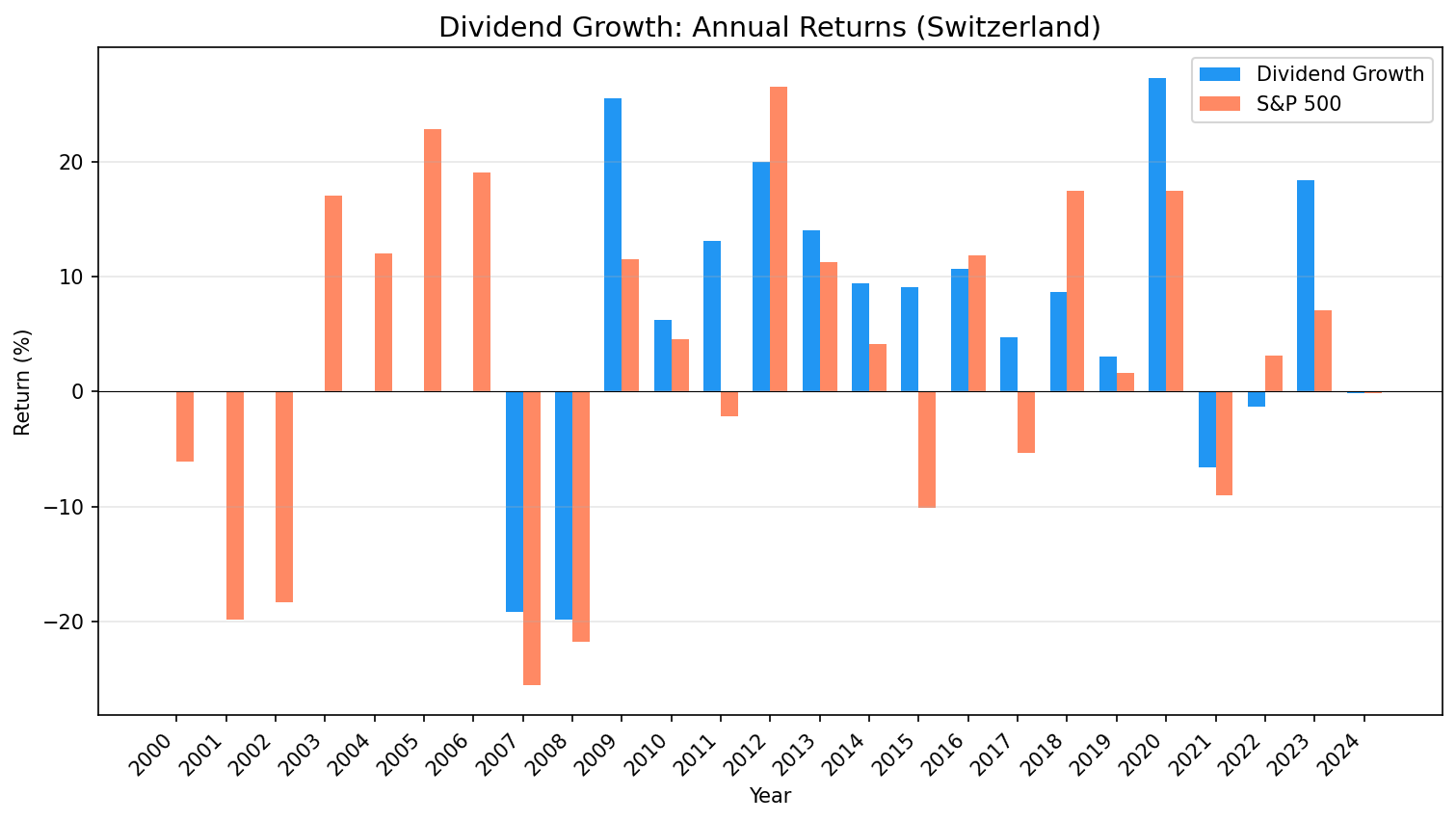

Annual Returns (Invested Years)

| Year | Strategy | SMI | Excess |

|---|---|---|---|

| 2007 | -19.2% | -25.6% | +6.4% |

| 2008 | -19.8% | -21.8% | +1.9% |

| 2009 | +25.5% | +11.6% | +14.0% |

| 2010 | +6.2% | +4.5% | +1.7% |

| 2011 | +13.1% | -2.2% | +15.3% |

| 2012 | +20.0% | +26.6% | -6.5% |

| 2013 | +14.0% | +11.3% | +2.7% |

| 2014 | +9.4% | +4.1% | +5.3% |

| 2015 | +9.1% | -10.1% | +19.2% |

| 2016 | +10.7% | +11.8% | -1.1% |

| 2017 | +4.8% | -5.3% | +10.1% |

| 2018 | +8.7% | +17.5% | -8.8% |

| 2019 | +3.0% | +1.7% | +1.3% |

| 2020 | +27.3% | +17.5% | +9.9% |

| 2021 | -6.6% | -9.1% | +2.4% |

| 2022 | -1.3% | +3.1% | -4.4% |

| 2023 | +18.4% | +7.1% | +11.3% |

| 2024 | -0.1% | -0.2% | +0.1% |

When It Works

2015: +9.1% vs the SMI's -10.1%. That's +19.2% excess, the best single year. The SNB abandoned the EUR/CHF floor in January 2015, crashing the SMI. Dividend growers, backed by global revenue streams, held up while the index cratered.

2011: +13.1% vs the SMI's -2.2%. A +15.3% excess during the European debt crisis. Swiss quality companies with long payout traditions attracted capital as investors fled risk.

2009 (post-crisis recovery): +25.5% vs the SMI's +11.6%. The strategy captured +14.0% excess as companies that maintained dividends through 2008 were rewarded.

2007-2008 (financial crisis): The portfolio lost -19.2% and -19.8%, but the SMI fell -25.6% and -21.8%. Consistent outperformance during the worst two-year stretch. Nestle, Novartis, and Roche kept paying because their revenue streams don't disappear in a recession.

2023: +18.4% vs the SMI's +7.1%. A +11.3% excess. Dividend growers led the Swiss recovery.

Pattern: the strategy works best during stress, recovery, and periods of franc strength. When investors seek safety, Swiss dividend growers attract capital. The 52% win rate means the strategy beats the SMI in more years than not.

When It Struggles

2018: +8.7% vs the SMI's +17.5%. A -8.8% gap. The SMI rallied hard on pharma and luxury goods momentum, and dividend growers couldn't keep pace with the broader index surge.

2012: +20.0% vs the SMI's +26.6%. A -6.5% gap. Both performed well, but the index outran the dividend screen during a broad European recovery.

2022: -1.3% vs the SMI's +3.1%. A -4.4% gap. The only recent year where the strategy lost money while the benchmark gained.

2016: +10.7% vs the SMI's +11.8%. A -1.1% gap. Essentially flat excess, showing that in calm, broad-based rallies the dividend screen can lag slightly.

Pattern: the strategy lags when the SMI rallies broadly, driven by index heavyweights outside the dividend-growth universe. But the losses are moderate. The worst single-year shortfall is -8.8%, nothing like the double-digit gaps you see with US-benchmarked strategies. With a 52% win rate, you beat the SMI in more years than you trail it.

Limitations

Small universe: Only 15.9 stocks on average, well below the 30-stock target. The Swiss market has a limited pool of companies that meet the five-year streak requirement. This concentration adds stock-specific risk.

Data starts 2007: FMP Swiss data is sparse before 2007. The 7 cash periods reflect data gaps, not strategy failure. Effective results cover 2007-2024 (18 invested years).

Modest absolute returns: 4.31% CAGR beats the SMI's 1.74%, but it's still a low absolute number. If you're targeting 8%+ annual returns, Swiss dividend growers won't get you there regardless of benchmark.

Concentrated index: The SMI has only 20 constituents. The dividend growth screen overlaps heavily with SMI components, so alpha partly reflects stock selection within a narrow universe rather than a fundamentally different exposure.

Run This Screen (Switzerland)

WITH annual_div AS (

SELECT symbol,

EXTRACT(YEAR FROM CAST(date AS DATE)) AS yr,

SUM(adjDividend) AS total_div

FROM dividend_calendar

WHERE adjDividend > 0

AND symbol IN (SELECT DISTINCT symbol FROM profile WHERE exchange IN ('SIX'))

GROUP BY symbol, EXTRACT(YEAR FROM CAST(date AS DATE))

),

growth AS (

SELECT symbol, yr, total_div,

LAG(total_div) OVER (PARTITION BY symbol ORDER BY yr) AS prev_div

FROM annual_div

),

last_break AS (

SELECT symbol, MAX(yr) AS break_yr

FROM growth

WHERE prev_div IS NOT NULL AND total_div <= prev_div

GROUP BY symbol

),

streak AS (

SELECT g.symbol, COUNT(*) AS consecutive_years,

MIN(g.yr) AS streak_from, MAX(g.yr) AS streak_to

FROM growth g

LEFT JOIN last_break lb ON g.symbol = lb.symbol

WHERE g.prev_div IS NOT NULL

AND g.total_div > g.prev_div

AND (lb.break_yr IS NULL OR g.yr > lb.break_yr)

GROUP BY g.symbol

HAVING COUNT(*) >= 5

)

SELECT s.symbol, s.consecutive_years, s.streak_from, s.streak_to,

ROUND(r.dividendPayoutRatioTTM * 100, 1) AS payout_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_bn,

ROUND(c.freeCashFlow / 1e6, 0) AS fcf_mm

FROM streak s

JOIN financial_ratios_ttm r ON s.symbol = r.symbol

JOIN key_metrics_ttm k ON s.symbol = k.symbol

JOIN cash_flow_statement_ttm c ON s.symbol = c.symbol

WHERE r.dividendPayoutRatioTTM BETWEEN 0 AND 0.80

AND c.freeCashFlow > 0

AND k.marketCap > 500000000

QUALIFY ROW_NUMBER() OVER (PARTITION BY s.symbol ORDER BY s.consecutive_years DESC) = 1

ORDER BY s.consecutive_years DESC, k.marketCap DESC

LIMIT 30

Data: Ceta Research (FMP financial data warehouse). Universe: SIX, market cap > CHF 500M. Backtest: 2000-2025, annual July rebalance. Past performance does not guarantee future results. This is educational content, not investment advice.

Takeaway

Switzerland's dividend growth screen delivers what you'd want from a local equity strategy: positive alpha with low volatility. The 4.31% CAGR beats the SMI's 1.74% by +2.57% annually. Volatility of 11.32% is the lowest of any exchange we tested. The Sortino of 0.661 is five times the SMI's 0.131.

The asymmetric capture ratio is the headline number. Up capture of 59.13% vs down capture of 30.67% means the portfolio participates in rallies but blocks most of the downside. A 52% win rate confirms this isn't a fluke: you beat the SMI in more years than you trail it. Alpha of 1.53% with a beta of 0.431 is a clean risk-adjusted story.

The limitation is absolute return. 4.31% CAGR won't satisfy investors targeting high growth. But for Swiss equity exposure, the dividend growth screen does what it should: identifies quality companies, reduces drawdowns, and compounds ahead of the index over time.

Part of a Series

This is the Switzerland analysis. See also: - Dividend Growth on US Stocks - full methodology - Dividend Growth on Indian Stocks (NSE) - Dividend Growth on Canadian Stocks (TSX) - Dividend Growth on UK Stocks (LSE) - Dividend Growth on German Stocks (XETRA) - Dividend Growth Across Global Exchanges - full comparison

References

- Lintner, J. (1956). "Distribution of Incomes of Corporations Among Dividends, Retained Earnings, and Taxes." American Economic Review, 46(2), 97-113.

- Arnott, R. & Asness, C. (2003). "Surprise! Higher Dividends = Higher Earnings Growth." Financial Analysts Journal, 59(1), 70-87.