DCF Discount on Taiwanese Stocks: 9.24% CAGR, +6.19% Excess vs TAIEX

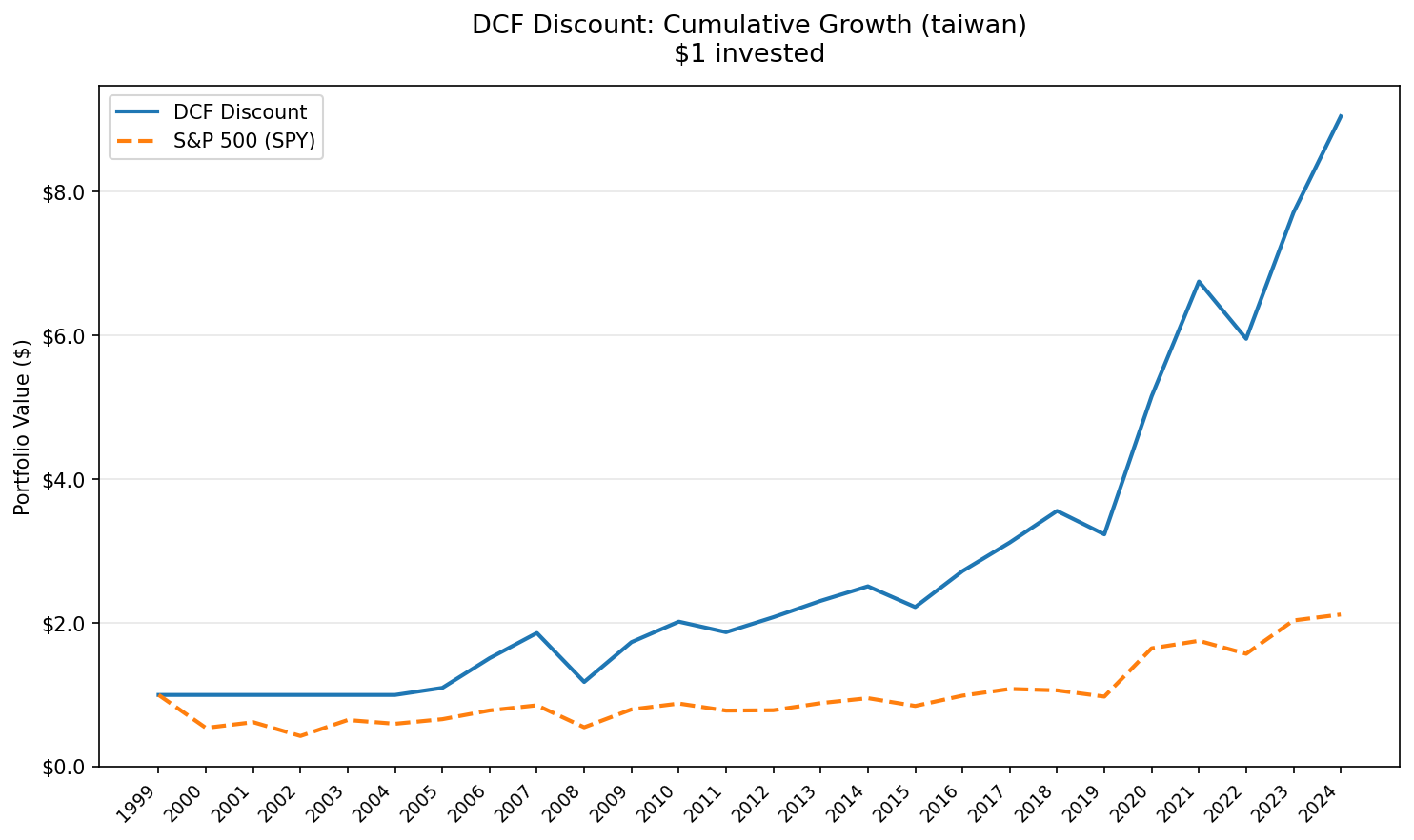

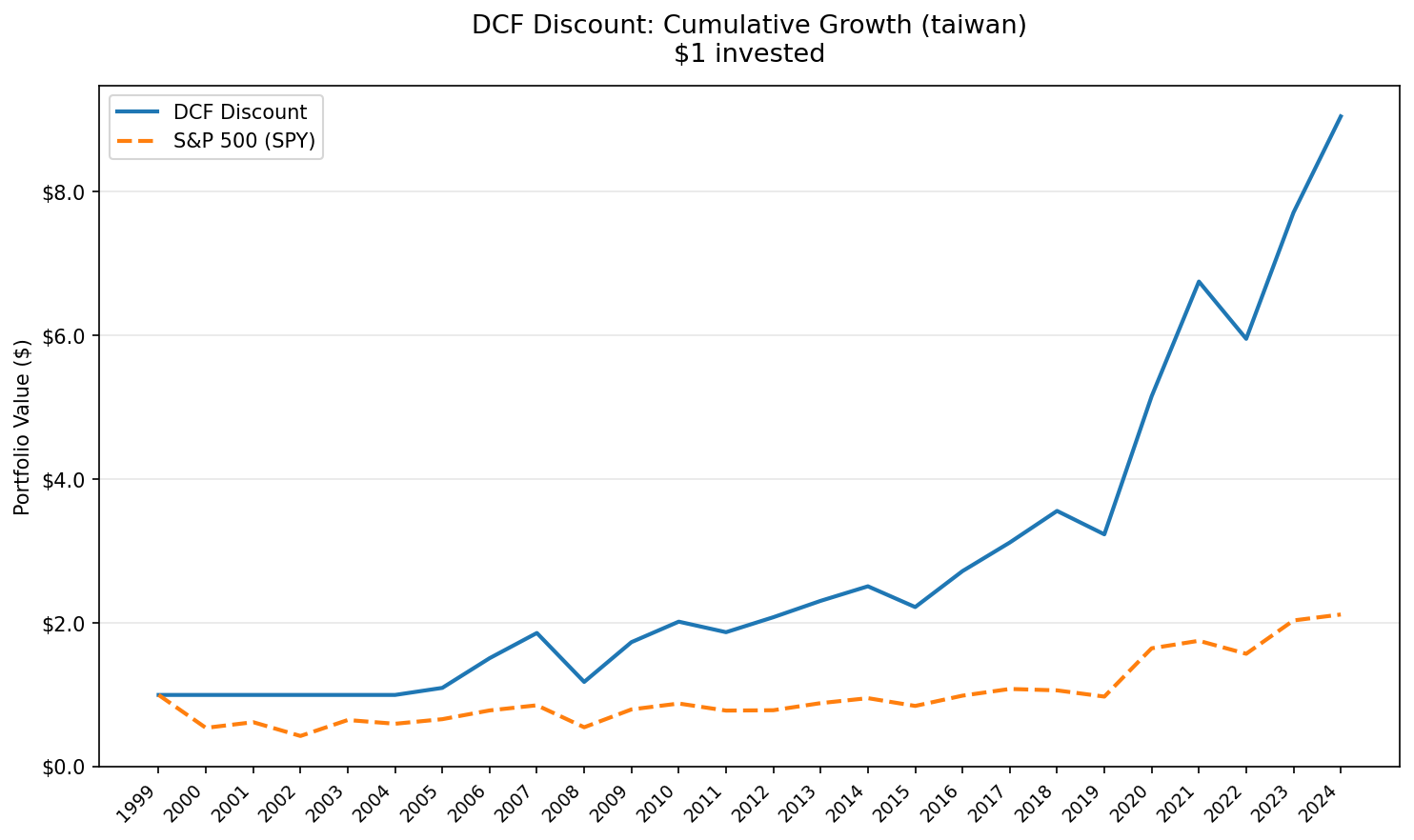

Taiwan's DCF discount portfolio returned 9.24% CAGR over 25 years, beating the TAIEX by +6.19% annually. The 0.399 Sharpe, -35.91% max drawdown (shallowest of any Asian market), and ~2.8:1 up/down capture asymmetry show strong risk-adjusted performance.

Taiwan produced strong risk-adjusted returns in our DCF discount backtest. Across 25 annual periods (2000-2025) with 5 cash years at the start, the strategy returned 9.24% CAGR with a 0.399 Sharpe, beating the TAIEX's 3.05% by +6.19% annually. The max drawdown was -35.91%, the shallowest of any Asian market we tested. A beta of 0.595 against the TAIEX captured 107.64% of upside and only 38.03% of downside.

Contents

- Method

- The Screen

- Results

- Year-by-Year

- Key Observations

- The cash years (2000-2004)

- Contained drawdown

- Downside protection without sacrificing upside

- The tech market paradox

- Strong excess return with outstanding risk efficiency

- Limitations

- Takeaway

- Part of a Series

Taiwan's tech-heavy index (TSMC alone is ~30% of the TAIEX) didn't drag this portfolio into semiconductor volatility. The DCF screen found value elsewhere: industrials, materials, financials. Companies generating real free cash flow at reasonable prices.

Data: FMP financial data warehouse, 2000-2025. Updated May 2026 (post bias fix).

Method

Signal: FCF/MarketCap >= 8.78% (equivalent to a 20% DCF discount). Gordon Growth Model: g=2.5%, r=10%, multiple=13.67x. Top 50 by FCF yield, equal weight. Universe: TAI + TWO (Taiwan Stock Exchange + Taipei Exchange). Market cap > NT$10B (~$312M USD). Period: 2000-2025 (25 years, annual rebalancing in April). Execution: Next-day close (MOC). Signal generated at rebalance date, executed at the following trading day's close. Transaction costs: Size-tiered model applied. Benchmark: TAIEX (^TWII), the local Taiwanese benchmark. Data: Ceta Research (FMP financial data warehouse).

Full methodology: DCF Discount US (flagship post with model details, academic references, and limitations of DCF-based screening).

The Screen

WITH latest_cfs AS (

SELECT * FROM cash_flow_statement

WHERE period = 'FY' AND freeCashFlow > 0 AND reportedCurrency = 'TWD'

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) = 1

),

latest_km AS (

SELECT * FROM key_metrics

WHERE period = 'FY' AND marketCap > 10000000000

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) = 1

)

SELECT

cfs.symbol,

p.companyName,

p.sector,

ROUND(cfs.freeCashFlow / 1e6, 0) AS fcf_mm,

ROUND(km.marketCap / 1e9, 2) AS mktcap_bn,

ROUND(cfs.freeCashFlow / km.marketCap * 100, 2) AS fcf_yield_pct,

ROUND((1 - km.marketCap / (cfs.freeCashFlow * 13.67)) * 100, 1) AS discount_pct

FROM latest_cfs cfs

JOIN latest_km km ON cfs.symbol = km.symbol

JOIN profile p ON cfs.symbol = p.symbol

WHERE p.exchange IN ('TAI', 'TWO')

AND p.isFund = false

AND p.isEtf = false

AND p.isActivelyTrading = true

AND cfs.freeCashFlow / km.marketCap BETWEEN 0.0878 AND 0.50

ORDER BY fcf_yield_pct DESC

LIMIT 30

Run this screen live on Ceta Research

Results

The headline: Taiwan's DCF discount portfolio beat the TAIEX by +6.19% annually. The Sharpe of 0.399 and Sortino of 0.949 strongly favor the portfolio. The TAIEX's Sharpe was just 0.080.

| Metric | DCF Discount Taiwan | TAIEX |

|---|---|---|

| CAGR | 9.24% | 3.05% |

| Total Return | 811.83% | 111.91% |

| Excess CAGR | +6.19% | - |

| Max Drawdown | -35.91% | -57.10% |

| Annualized Volatility | 20.65% | 25.59% |

| Sharpe Ratio | 0.399 | 0.080 |

| Sortino Ratio | 0.949 | 0.143 |

| Calmar Ratio | 0.257 | 0.053 |

| VaR 95% | -12.48% | -35.74% |

| Beta (vs TAIEX) | 0.595 | 1.0 |

| Alpha (Jensen) | 7.02% | - |

| Up Capture | 107.64% | - |

| Down Capture | 38.03% | - |

| Win Rate | 72% | - |

| Information Ratio | 0.288 | - |

| Tracking Error | 17.38% | - |

| Cash Periods | 5/25 | 0 |

| Avg Stocks (invested) | 44.2 | - |

The up/down capture ratio is the clearest way to read Taiwan's character. The portfolio captured 107.64% of the TAIEX's gains and only 38.03% of its losses. That ~2.8:1 asymmetry is strong. Most value strategies on other exchanges run 1:1 or worse.

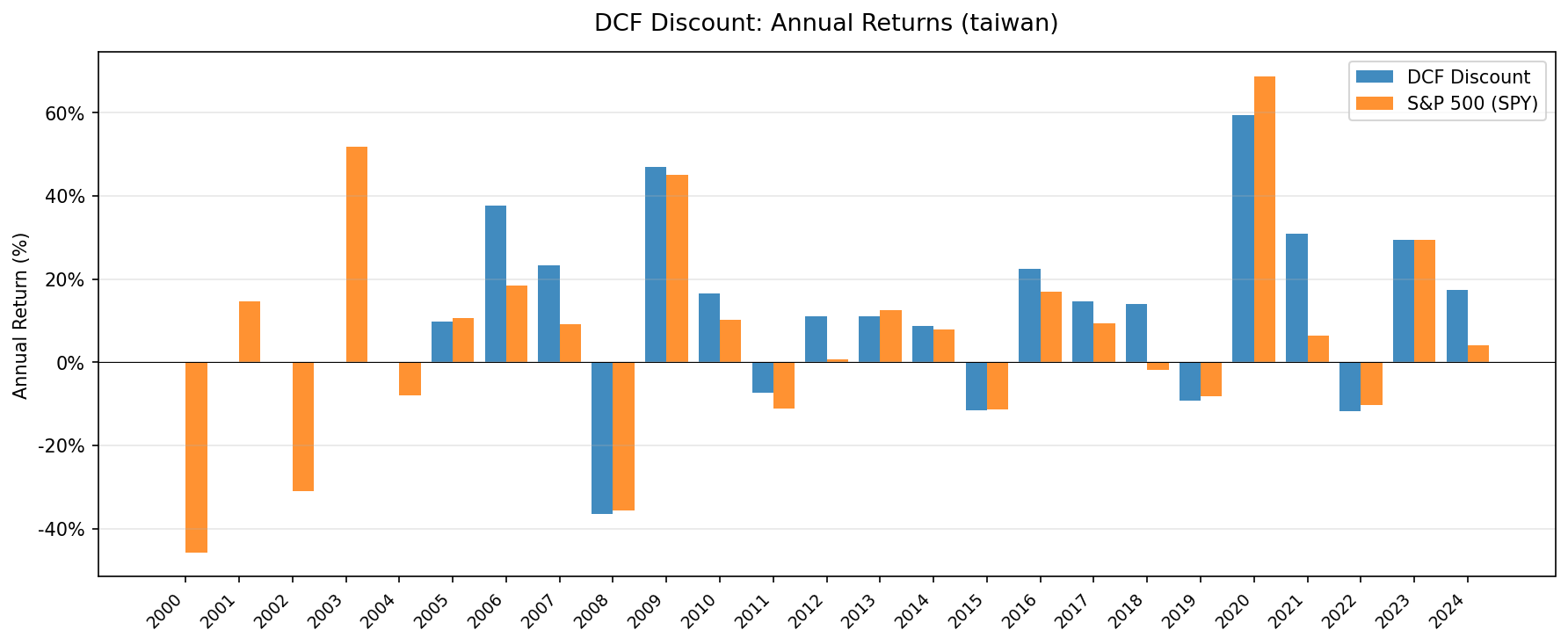

Year-by-Year

| Year | Portfolio | TAIEX | Excess |

|---|---|---|---|

| 2000 | 0.0% (cash) | -45.8% | +45.8% |

| 2001 | 0.0% (cash) | +14.6% | -14.6% |

| 2002 | 0.0% (cash) | -30.9% | +30.9% |

| 2003 | 0.0% (cash) | +51.8% | -51.8% |

| 2004 | 0.0% (cash) | -8.0% | +8.0% |

| 2005 | +10.6% | +10.7% | -0.0% |

| 2006 | +38.7% | +18.4% | +20.4% |

| 2007 | +24.7% | +9.1% | +15.6% |

| 2008 | -35.9% | -35.7% | -0.2% |

| 2009 | +47.6% | +45.1% | +2.4% |

| 2010 | +15.7% | +10.3% | +5.4% |

| 2011 | -9.1% | -11.2% | +2.1% |

| 2012 | +10.1% | +0.6% | +9.5% |

| 2013 | +13.5% | +12.5% | +1.0% |

| 2014 | +8.7% | +7.8% | +0.9% |

| 2015 | -10.7% | -11.3% | +0.6% |

| 2016 | +22.4% | +16.9% | +5.5% |

| 2017 | +12.6% | +9.4% | +3.2% |

| 2018 | +15.0% | -1.8% | +16.8% |

| 2019 | -8.9% | -8.2% | -0.7% |

| 2020 | +60.3% | +68.8% | -8.5% |

| 2021 | +29.1% | +6.4% | +22.7% |

| 2022 | -12.5% | -10.3% | -2.2% |

| 2023 | +29.5% | +29.5% | +0.0% |

| 2024 | +16.7% | +4.1% | +12.6% |

Key Observations

The cash years (2000-2004)

The portfolio sat in cash for the first five years. There weren't enough Taiwanese stocks above NT$10B market cap with sufficient FCF data on TAI+TWO to build a 10-stock portfolio. Taiwan's listed universe was smaller then, and FMP coverage of Taiwanese companies before 2005 is thin.

This creates a data artifact: the strategy missed the 2003 TAIEX rally (+51.8%) and avoided the 2000-2002 drawdowns. From 2005 onward, the portfolio was fully invested every year with an average of 44.2 stocks. All the return and risk numbers reflect this 20-year invested period.

Contained drawdown

The worst year was 2008: -35.9%. The TAIEX fell -35.7%, so the portfolio tracked the market almost exactly during the crisis. Taiwan's -35.9% in a single year drove the -35.91% max drawdown. That's much shallower than the TAIEX's own -57.10% max drawdown, since the portfolio was in cash during earlier TAIEX crashes.

Why did Taiwan hold up relatively well? Taiwanese value stocks tilted toward cash-rich industrials and electronics manufacturers with strong balance sheets. Taiwan's economy contracted but the export machine bounced back fast. The portfolio recovered fully by mid-2009 (+47.6%).

Downside protection without sacrificing upside

The 0.595 beta means the portfolio moved about 60% as much as the TAIEX in either direction. But the capture ratios tell a different story. Up capture of 107.64% means it captured more upside than beta alone would predict. Down capture of 38.03% means it participated in less than 40% of the TAIEX's losses.

That asymmetry is the core finding. Taiwan's DCF discount portfolio didn't just dampen volatility. It did so asymmetrically, giving up far less downside than upside. The Sortino ratio of 0.949 (which penalizes only downside deviation) confirms this, more than 6x the TAIEX's 0.143.

The tech market paradox

Taiwan's TAIEX is dominated by semiconductor and electronics companies. TSMC alone is a massive portion of the index. You'd expect a value screen on a tech-heavy market to either miss the best performers (underweight tech) or get dragged into cyclical semiconductor downturns.

Neither happened. The DCF screen selected companies generating high free cash flow relative to market cap. In Taiwan, those tend to be component manufacturers, industrial conglomerates, financial holding companies, and mid-cap electronics firms. Not the TSMC-tier headline names, but the companies supplying the supply chain. These businesses are less volatile than the flagship semiconductor stocks, and their cash flows are more predictable.

Strong excess return with outstanding risk efficiency

The +6.19% excess CAGR is substantial. Taiwan delivered those returns with lower risk than the benchmark. The Calmar ratio (CAGR/MaxDD) of 0.257 is nearly 5x the TAIEX's 0.053. Volatility of 20.65% is lower than the TAIEX's 25.59%. Taiwan's DCF discount portfolio was less volatile than its benchmark, a rare result.

Sweden's portfolio posts a higher Sharpe (0.579) thanks to its long cash stretches in down markets, and Germany (0.425) edges Taiwan by a hair on Sharpe alone. But Taiwan's max drawdown of -35.91% is the shallowest among Asian markets we tested (vs Hong Kong -52%, Japan -42%, Korea -45%, China -48%, India -58%). For an investor focused on Asian equity exposure, that's the standout characteristic.

Limitations

Cash drag and data coverage. Five years of cash (2000-2004) mean the 25-year CAGR blends invested and uninvested periods. The 20-year invested CAGR (2005-2024) would be higher than the reported 9.24%. The early cash years reflect FMP's coverage gap for Taiwanese stocks, not a signal failure.

Benchmark is price-only. The TAIEX (^TWII) is a price-only index and doesn't include dividends. The strategy returns use total-return data (adjusted close, which incorporates dividends). Taiwanese equities yield roughly 3% on average. The true alpha vs a total-return TAIEX is narrower than the headline by approximately that amount, putting the realistic excess closer to +3% than +6.19%.

Currency exposure. Returns are in TWD (Taiwan Dollar). The TWD has been relatively stable against the USD over this period, trading between roughly 31 and 33 TWD/USD for most of the backtest window. FX impact is smaller here than for India or Korea, but it's still present. A USD-based investor buying Taiwanese equities directly would see slightly different returns depending on entry and exit timing.

Concentration risk. 44.2 stocks on average, but Taiwan's listed universe is smaller than the US or India. Sector concentration toward industrials and electronics component makers is inherent in what the screen selects.

Survivorship and delisted companies. FMP includes delisted Taiwanese stocks (partially addressing survivorship bias), but coverage quality for smaller TAI/TWO listings before 2010 is less comprehensive than for the US.

Takeaway

Taiwan produced one of the most risk-efficient DCF discount portfolios of any market we tested. The 0.399 Sharpe, 0.949 Sortino, and -35.91% max drawdown (shallowest of any Asian market) show strong risk-adjusted performance. The up/down capture asymmetry (107.64% / 38.03%) shows the strategy does what value investing is supposed to do: participate in gains, protect against losses.

The +6.19% annual excess return vs the TAIEX is substantial on the headline. After adjusting for the price-only benchmark's missing ~3% dividend yield, the realistic edge is closer to +3% per year. That's still a meaningful alpha for a steady, risk-aware value portfolio on a market that sits at the center of global semiconductor supply chains.

Part of a Series

This analysis is part of our DCF Discount global exchange comparison:

- DCF Discount on US Stocks (NYSE + NASDAQ + AMEX)

- DCF Discount on Indian Stocks (NSE)

- DCF Discount on Taiwan Stocks (TAI + TWO)

- DCF Discount on Canadian Stocks (TSX)

- DCF Discount on Korean Stocks (KSC)

- DCF Discount on German Stocks (XETRA)

- DCF Discount on Swedish Stocks (STO)

- DCF Discount: Global Exchange Comparison

Data: Ceta Research (FMP financial data warehouse), TAI+TWO, 2000-2025. Returns in TWD. Next-day close (MOC) execution. Benchmark: TAIEX (^TWII), price-only index, no dividends. Full methodology: METHODOLOGY.md. Backtest code: backtests/dcf-discount/. Not investment advice.