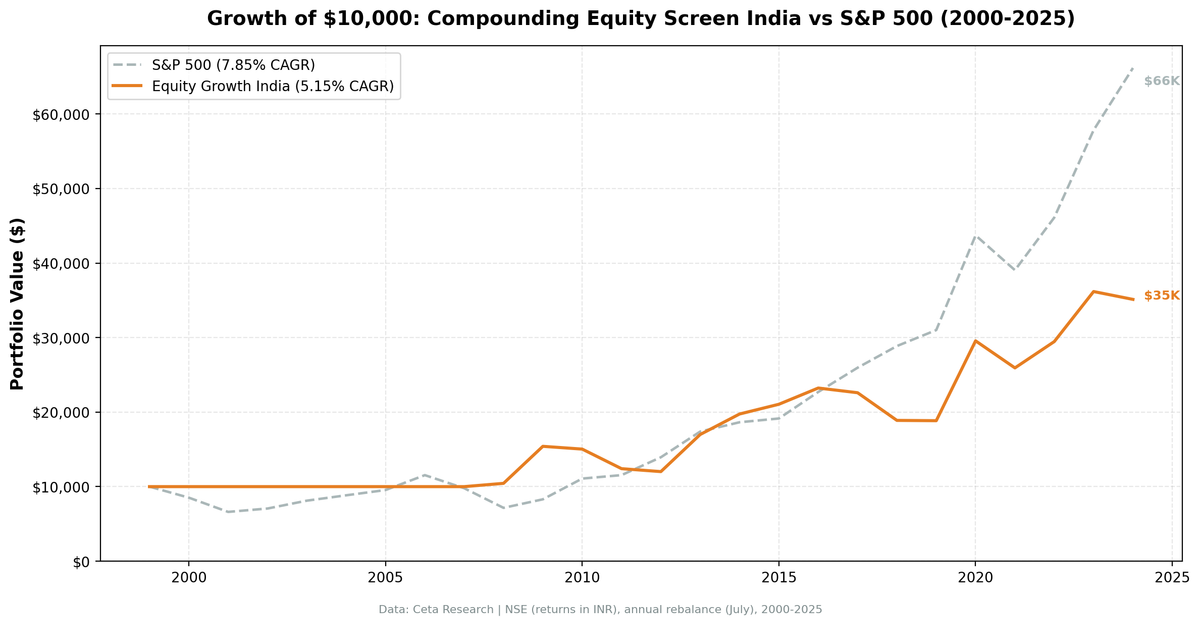

Compounding Equity Screen India: 5.15% CAGR, Underperforms Sensex by 6.90% Annually

We backtested the Compounding Equity Screen on NSE stocks from 2000 to 2025. 5.15% CAGR vs 12.06% for the Sensex. The strategy underperforms the local benchmark by 6.90% annually, with 8 of 25 years in cash missing India''s strongest bull market.

Compounding Equity Screen India: 5.15% CAGR vs Sensex's 12.06%

We backtested the Compounding Equity Screen on NSE stocks from 2000 to 2025. The portfolio returned 5.15% annually vs 12.06% for the Sensex. That's a -6.90% annual shortfall.

Contents

- Method

- Signal and Filters

- Why Cash in 2000-2007

- Results

- Best Periods

- Weak Periods

- Full Annual Returns

- The Screen

- Limitations

- Takeaway

- References

Eight of 25 rebalance periods were cash (2000-2007). The strategy missed India's strongest bull market: the Sensex returned +35%, +49%, +47%, and +39% from 2003 to 2006. When the portfolio finally invested in 2008, it had already fallen far behind.

The result is a portfolio that significantly underperforms the local benchmark. The strategy shows some ability to outperform during recovery years (2009, 2013, 2020), but the 8-year data gap and inconsistent invested returns make it a poor fit for the Indian market.

Data: FMP financial data warehouse, 2000-2025. Updated July 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: NSE (India), market cap > ₹20B (~$230M USD) Period: 2000-2025 (25 annual rebalance periods, 8 cash, 17 invested) Rebalancing: Annual (July), equal weight top 30 by highest equity CAGR Benchmark: Sensex (^BSESN), returns in INR Cash rule: Hold cash if fewer than 10 stocks qualify Transaction costs: Size-tiered model adapted for NSE costs Data quality guards: Entry price > ₹1, single-period return capped at 200%

Financial data uses a 45-day lag from the rebalance date for point-in-time correctness. Full methodology: backtests/METHODOLOGY.md

Signal and Filters

| Criterion | Metric | Threshold | Why |

|---|---|---|---|

| Value creation | Shareholders' equity CAGR (5yr) | > 10% | Core compounding signal |

| Quality overlay | Return on Equity (TTM) | > 8% | Growth from operations |

| Quality overlay | Operating Profit Margin (TTM) | > 8% | Pricing power confirmed |

| Liquidity | Market Cap | > ₹20B | Investable, liquid universe |

The 5-year equity CAGR window accepts 3.5 to 7.0 years to handle data gaps. The CAGR cap at 100% filters inflation artifacts. Both equity endpoints must be positive (negative equity = financial distress excluded).

Why Cash in 2000-2007

India had 8 cash periods: 2000-2007. This isn't a strategy failure, but it's the biggest drag on performance.

The 5-year equity CAGR screen requires 5 years of prior annual filings. For Indian companies in FMP's warehouse, sufficient depth to run the screen at scale became available gradually. The years 2000-2007 produced fewer than 10 qualifying stocks (below the minimum threshold), triggering the cash rule.

The cash periods were devastating for relative performance. The Sensex returned +35.2%, +49.4%, +46.5%, and +38.9% from 2003 to 2006. The portfolio sat in cash through all of it. While holding cash did avoid the dot-com bust (2000-2001, Sensex -29.3% and -4.1%), the missed gains in the 2003-2006 bull market far outweigh any benefit from the early cash years.

Results

| Metric | Portfolio | Sensex |

|---|---|---|

| CAGR | 5.15% | 12.06% |

| Max Drawdown | -22.01% | -- |

| Sharpe Ratio | -0.074 | -- |

| Excess Return | -6.90%/yr | -- |

| Cash Periods | 8/25 | -- |

The -6.90% annual shortfall is large. The Sensex compounded at 12.06% over this period, one of the strongest equity market runs globally. The portfolio's 5.15% CAGR means an investor would have been far better off holding an index fund.

The lower max drawdown (-22.01%) reflects the 8 cash years more than any defensive property. When the portfolio was invested, it experienced significant drawdowns in 2011 (-17.5%), 2018 (-16.4%), and 2021 (-12.3%).

Best Periods

Recovery years where the strategy outperformed:

| Year | Portfolio | Sensex | Excess |

|---|---|---|---|

| 2009 | +47.6% | +19.1% | +28.5% |

| 2013 | +41.5% | +32.8% | +8.7% |

| 2014 | +16.2% | +8.1% | +8.0% |

| 2020 | +56.8% | +46.4% | +10.4% |

The pattern is clear: the strategy outperforms coming out of sharp downturns. After the 2008 crisis, after the 2012 correction, and after the 2020 COVID crash, equity compounders with strong balance sheets led the recovery. 2009 was the best year, beating the Sensex by 28 percentage points.

2008 (first invested year): The portfolio returned +4.4% vs the Sensex's +7.3%, a -2.9% shortfall. The Sensex gained in our July-to-July measurement window, so there's no "crisis protection" story here against the local benchmark.

Weak Periods

2010-2012 (Post-Recovery Correction):

| Year | Portfolio | Sensex | Excess |

|---|---|---|---|

| 2010 | -2.4% | +7.8% | -10.2% |

| 2011 | -17.5% | -7.5% | -9.9% |

| 2012 | -3.2% | +11.9% | -15.0% |

Three consecutive years of underperformance. The Sensex held up reasonably well during this period, but the portfolio's equity compounders suffered from post-commodity supercycle correction and valuation compression. Cumulative underperformance: -35.2% over three years.

2017-2018:

| Year | Portfolio | Sensex | Excess |

|---|---|---|---|

| 2017 | -2.7% | +13.0% | -15.7% |

| 2018 | -16.4% | +12.9% | -29.3% |

The Sensex kept climbing while the portfolio's equity compounders collapsed. Demonetization effects and GST transition pressures weighed on the kinds of mid-cap businesses this screen selects. 2018 was the worst single year of underperformance: -29.3% vs the Sensex.

Full Annual Returns

| Year | Portfolio | Sensex | Excess |

|---|---|---|---|

| 2000 | 0.0% (cash) | -31.6% | +31.6% |

| 2001 | 0.0% (cash) | -0.8% | +0.8% |

| 2002 | 0.0% (cash) | +9.6% | -9.6% |

| 2003 | 0.0% (cash) | +35.2% | -35.2% |

| 2004 | 0.0% (cash) | +49.4% | -49.4% |

| 2005 | 0.0% (cash) | +46.5% | -46.5% |

| 2006 | 0.0% (cash) | +38.9% | -38.9% |

| 2007 | 0.0% (cash) | -7.7% | +7.7% |

| 2008 | +4.4% | +7.3% | -2.9% |

| 2009 | +47.6% | +19.1% | +28.5% |

| 2010 | -2.4% | +7.8% | -10.2% |

| 2011 | -17.5% | -7.5% | -9.9% |

| 2012 | -3.2% | +11.9% | -15.0% |

| 2013 | +41.5% | +32.8% | +8.7% |

| 2014 | +16.2% | +8.1% | +8.0% |

| 2015 | +6.6% | -2.4% | +9.0% |

| 2016 | +10.3% | +14.5% | -4.1% |

| 2017 | -2.7% | +13.0% | -15.7% |

| 2018 | -16.4% | +12.9% | -29.3% |

| 2019 | -0.2% | -10.0% | +9.8% |

| 2020 | +56.8% | +46.4% | +10.4% |

| 2021 | -12.3% | +1.4% | -13.7% |

| 2022 | +13.6% | +22.5% | -8.9% |

| 2023 | +22.8% | +21.8% | +1.0% |

| 2024 | -2.9% | +5.0% | -7.9% |

Note: Returns measured July-to-July. Cash periods earn 0% by design (capital preservation).

The Screen

Run this screen live on Ceta Research →

WITH curr_eq AS (

SELECT symbol, totalStockholdersEquity AS eq_curr, dateEpoch AS epoch_curr,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM balance_sheet

WHERE period = 'FY' AND totalStockholdersEquity > 0

),

prior_5yr AS (

SELECT c.symbol,

b.totalStockholdersEquity AS eq_prior,

(c.epoch_curr - b.dateEpoch) / 31536000.0 AS years_gap,

POWER(

c.eq_curr / b.totalStockholdersEquity,

1.0 / ((c.epoch_curr - b.dateEpoch) / 31536000.0)

) - 1 AS eq_cagr,

ROW_NUMBER() OVER (

PARTITION BY c.symbol

ORDER BY ABS((c.epoch_curr - b.dateEpoch) / 31536000.0 - 5) ASC

) AS best_match

FROM curr_eq c

JOIN balance_sheet b ON c.symbol = b.symbol AND c.rn = 1

AND b.period = 'FY' AND b.totalStockholdersEquity > 0

AND b.dateEpoch < c.epoch_curr - 4 * 31536000

AND b.dateEpoch > c.epoch_curr - 7 * 31536000

)

SELECT pr.symbol, p.companyName, p.sector,

ROUND(pr.eq_cagr * 100, 2) AS eq_cagr_pct,

ROUND(pr.years_gap, 1) AS years_measured,

ROUND(k.returnOnEquityTTM * 100, 2) AS roe_pct,

ROUND(f.operatingProfitMarginTTM * 100, 2) AS opm_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM prior_5yr pr

JOIN profile p ON pr.symbol = p.symbol

JOIN key_metrics_ttm k ON pr.symbol = k.symbol

JOIN financial_ratios_ttm f ON pr.symbol = f.symbol

WHERE pr.best_match = 1 AND pr.years_gap BETWEEN 3.5 AND 7.0

AND pr.eq_cagr > 0.10 AND pr.eq_cagr < 1.00

AND k.returnOnEquityTTM > 0.08

AND f.operatingProfitMarginTTM > 0.08

AND k.marketCap > 20000000000

AND p.exchange IN ('NSE')

AND p.isActivelyTrading = true

ORDER BY pr.eq_cagr DESC

LIMIT 30

Limitations

Massive data gap. Eight of 25 periods were cash. The portfolio missed the Sensex's 2003-2006 run entirely (+35%, +49%, +47%, +39%). This is the single biggest reason for the -6.90% annual shortfall. An investor who started in 2008 would see a different picture, but the data gap is the reality of applying this screen to Indian markets.

Universe change. BSE was removed due to 38% dual-listing overlap with NSE. Running on NSE only gives a cleaner universe, but it reduced the eligible stock count.

Currency effects. Returns are in INR. For USD-based investors, INR/USD fluctuations add another layer. The rupee depreciated significantly in 2011-2013 and 2018-2019, amplifying negative periods for foreign investors.

Policy sensitivity. Indian equity compounders are disproportionately exposed to domestic growth policy. Demonetization (2016), GST implementation (2017), and NBFC credit crises (2018-2019) created multi-year headwinds specific to India's equity structure that a global quality signal can't anticipate.

Takeaway

The Compounding Equity Screen on NSE delivers 5.15% CAGR vs 12.06% for the Sensex. That's a -6.90% annual shortfall. The strategy does not work well in India when measured against the local benchmark.

The main problem is the 8-year data gap. The screen requires 5 years of prior filings, and FMP's Indian data didn't reach sufficient depth until 2008. Missing the Sensex's 2003-2006 bull market (+35% to +49% annually) created a hole the portfolio never recovered from.

When the portfolio was invested (2008-2024), it showed a pattern: strong outperformance in recovery years (2009: +28.5% excess, 2013: +8.7%, 2020: +10.4%) offset by persistent underperformance in mid-cycle years (2010-2012, 2017-2018). The recovery-year strength is real but not enough to close the gap.

For investors considering this screen in India, the honest conclusion is that a Sensex index fund would have delivered more than double the return with less effort. The strategy may have niche value as a recovery-year signal, but as a standalone portfolio it underperforms.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Universe: NSE (India). Returns in INR. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.

References

- Asness, C., Frazzini, A. & Pedersen, L. (2019). "Quality Minus Junk." Review of Accounting Studies, 24(1), 34-112.

- Gordon, M. & Shapiro, E. (1956). "Capital Equipment Analysis." Management Science, 3(1), 102-110.